ESG considerations in fixed income

Since 2014, we have been formally incorporating environmental, social and governance (ESG) factors into our investment process, including fixed income research. As a component of our manager research process, manager research analysts assign an ESG rank to individual strategies. Our observations of market trends assist us in identifying leading market practitioners around ESG considerations and implementations in their investment processes.

While ESG was initially a hot topic for equity investors, fixed income market investors are taking notice and practitioners are quickly catching up. At Russell Investments, we have observed the rapid expansion in ESG integration practice among fixed income asset managers in recent years.

In this blog, we aim to share some key ESG integration trends we see among the fixed income market practitioners. Our observations are derived from the findings from our 2019 Annual ESG Manager Survey and discussions with a number of fixed income market practitioners.

ESG for fixed income investing

Before diving into our observations, we believe it’s helpful to compare the history of ESG considerations in fixed income investing to equity investing. The primary difference is the fiduciary duty associated with proxy voting and shareholder engagement (proxy and engagement) for equity investment managers.

The role of proxy and engagement has emerged as a major part of responsible investment practices. The idea that investors can influence the activity of their holdings had a slower uptake among many bond investors, where “voting” isn’t an option. Fixed income investment managers distanced themselves from the notion of engagement at first, while focusing more on integration. However, we have seen some indications that fixed income managers are finding their way into an engagement practice that leverages some of the unique features of fixed income investing in a more implicit manner. We review this recent development further down in this blog post.

The below table highlights some key differences between ESG integration for equities and fixed income instruments. Fixed income investing is primarily about diversifying from and moderating the risks associated with equity investing, which is true even for the riskier securities such as high yield bonds and emerging markets bonds. It is not surprising, then, that ESG considerations are mainly considered a risk mitigation exercise in fixed income investing. ESG factors tend to have a long-term outcome that corresponds well for fixed income investing where the investment horizon also tends to be long-term.

Exhibit 1: Key differences between ESG integration for equities and fixed income instruments

| ESG INTEGRATION | EQUITIES | FIXED INCOME |

|---|---|---|

| Entities | Public corporation | Public or private corporation, Sovereign |

| Investment analysis | Fundamental (i.e., one stock price) | Multi-layered (i.e., fundamental, maturity, yield, capital structure) |

| Status | Owner with voting rights | Lender with credit terms |

| Trading | Upside return potential & downside risk mitigation | Downside risk mitigation |

| Performance | Upside return potential & downside risk mitigation | Downside risk mitigation |

| Engagement | Explicit | Implicit |

ESG data coverage availability

Within the fixed income market, we’ve observed that ESG integration has been more broadly adapted in the corporate credit market at first. This is understandable, given corporate bonds are the closest to equities, which allow equity coverage in ESG considerations to be transported into the corporate credit market. Many credit market practitioners try to incorporate ESG considerations into their companies’ credit analyses.

Third-party ESG data providers, such as MSCI and Sustainalytics, also had greater ESG coverage for corporate bonds than for the rest of the fixed income markets. Within the corporate bond world, investment grade rated corporate bonds have wider ESG data coverage than high yield bonds. This is mainly due to the fact that there are more privately held companies that are rated below investment grades, where the disclosure requirements are less than those that are publicly traded.

We have observed increased efforts to analyse ESG aspects in sovereign debts, followed by municipal and securitised markets over the past year. ESG considerations in corporate credit differ from sovereign bonds because the first is associated with companies while the second is associated with governments that become even more complex.

Furthermore, change is slower at the country level than at the company level, so investors need to be mindful of the timeline associated with ESG considerations in sovereign levels compared to corporate levels. While there are not set standards in how market practitioners apply ESG considerations in corporate credit analyses, the Sustainability Accounting Standard Board’s (SASB) standards to assess materiality of ESG considerations are assisting the market practitioners in establishing the ESG integration framework. On the other hand, sovereign debt analyses lack such well-established guidelines.

Engagement in fixed income

We have seen a trend where many fixed income market practitioners have started to utilise the engagement terminology as a part of their ESG integration efforts. So, we’d like to take a moment to discuss the engagement implications in fixed income investing.

While bondholders do not have voting rights per se, as capital providers to corporations, they do have a direct line of access and communication to management. For instance, the global bond market consists of over $60 trillion1 in market capitalisation. In our 2019 Annual ESG Manager Survey, we asked market practitioners to state how often they engage with underlying companies related to ESG issues.2 We saw 89% of market practitioners with both equity and bond offerings and 71% of market practitioners with bond-only offerings claim they often or always discuss ESG topics when they interface with companies they are invested in3.

The heightened market interest in ESG considerations has led many underlying companies to be more amenable to proactively discussing ESG related topics. That said, the explicit limitation exists for bondholders who are without proxy voting. We have observed that fixed income market practitioners with equity offerings leverage their equity counterparts to increase influence when engaging with the underlying companies. And some bond managers who have limited or no equity offering try to partner with other bond managers to increase influence. Climate Action 100+, an investor-led climate engagement coalition launched in 2017, helps facilitate such bond managers to coordinate the engagement activities with other investors4.

The growing reporting criteria

Demand for metrics-driven reporting is generally two-fold: one for ESG criteria broadly and the other for climate-change related metrics such as carbon footprint. Asset owners are increasingly demanding greater transparency around ESG considerations in their portfolios through reporting. As such, market practitioners are faced with a scaling challenge, because reporting formats often vary according to each asset owner’s content preferences. There is no standard in ESG reporting.

Furthermore, many market practitioners measure ESG criteria in their portfolios differently. Some practitioners incorporate third-party ESG data providers to help form their ESG insights. As vendors and market practitioners express ESG outputs differently, it is understandable that investors request their own criteria in order to facilitate comparison. Some market practitioners even appear to support this effort themselves: providing ESG scores from an external vendor, such as MSCI, even though they have their own interpretation of ESG.

As for reporting the linkage between portfolios and climate change specifically, a clear standard format is lacking. Many market practitioners report relative carbon footprint, such as a large amount of CO2-equivalent emission per revenue dollar. Some practitioners report projected annual CO2 emissions savings. Third-party data providers continue to expand their reporting capabilities around measuring greenhouse gas (GHG) emissions, particularly connecting to the global transition pathway required to limit global warming to below 2 degrees Celsius.

According to our ESG survey, climate reporting efforts have expanded in the last year. The Financial Stability Board (FSB) introduced the industry-led Task Force on Climate-related Financial Disclosures (TCFD)5 to encourage climate-related financial disclosures. As of December 2019, there were over 930 organisations around the globe supporting the TCFD, which represents over $11 trillion in market capitalisation.6 For PRI signatories, a continuously expanding portion of investment practitioners, TCFD-based reporting becomes mandatory in 2020. We expect climate-related reporting to receive a fair degree of attention this year.

Responsible investing product offerings

Responsible investing product offerings continue to expand around the globe. The scale of sustainable investments notably increased from 2016 to 2018. In 2016, European investments accounted for more than half of the total. Subsequently, however, sustainable investments in the U.S. and Japan grew. Active sustainable investments have turned into a global trend.

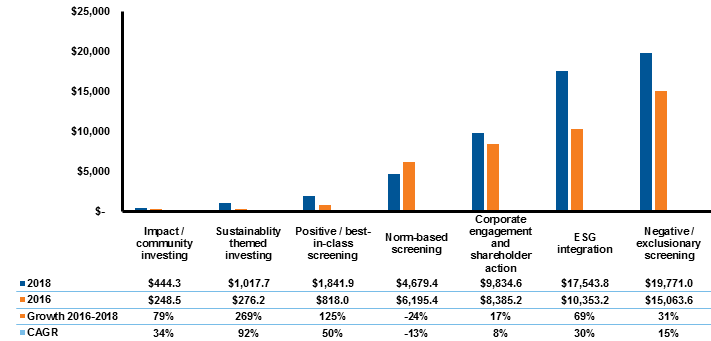

In order to dig deeper into the sustainable investing strategy offerings, the below chart shows the types of sustainable investing strategies offered. The largest category for the sustainable investing strategies is Negative/Exclusionary Screening. At the same time, the ESG Integration category has seen a much greater growth rate than screen-based offerings in recent years.

Global growth of sustainable investing strategies (2016-2018)

Source: Global Sustainable Investment Alliance, “Global Sustainable Investment Review” (2016 and 2018). All assets are converted to U.S. dollars at the exchange rates at each previous year-end.

Furthermore, Themed Investing has seen the highest growth, exceeding both screen-based and ESG Integration categories. This is in-line with our observation that market practitioners are launching responsible investing strategies that have targeted sustainable goals, such as following Sustainable Developments Goals (SDGs). We expect to see this growth trend for products with sustainable goals continue.

Impact investing in fixed income

Impact investing in the fixed income market has been relatively small but is growing across three primary categories: green bonds, social bonds and sustainability bonds.

- Green bonds aim to focus on transition toward a low carbon economy and are a leading impact solution within the fixed income market. Green bonds are bonds issued by countries or companies with the proceeds targeting environmental projects and opportunities.

- Social bonds focus on non-environmental impacts, including affordable housing, access to finance, and/or supporting small businesses.

- Sustainability bonds are quickly evolving and target a combination of green and social goals. We have observed that such sustainability bond offerings tend to link their investment opportunities with the United Nations’ SDGs.

The key features in impact investing are to understand how the proceeds are used and to monitor the actual versus stated objectives. In the case of green bonds, the International Capital Market Association’s Green Bond Principles aim to provide guidelines for the use of proceeds. However, there is much subjectivity in the definition of what qualifies as “green bonds” in the marketplace.

Summary and conclusions

The integration of ESG into investment practice is rapidly evolving for fixed income investors, and many market practitioners are embracing the agenda as a key initiative. While the starting point varies for each market practitioner, the whole market is adjusting. Key areas of advancement we’ve noted are through additional resources, data availability and establishing, or further enhancing, investment frameworks around ESG considerations.

ESG-specific information is increasingly available in the marketplace. Getting access to ESG-related data and digesting such information into one’s investment process are an evolving investment practice. Along with increased scrutiny, asset owners are demanding greater transparency around ESG considerations in their portfolios through reporting. Ultimately, asset owners want greater transparency regarding the linkage between the portfolios and climate change - yet how to respond to this aspirational goal is not yet clear, and a standard format does not currently exist. Reporting ESG criteria is a major topic in ESG investing and will certainly continue to evolve.

As we move forward, standout approaches will be able to demonstrate leading implementation methodologies, articulate a best practice and define useful and informative metrics that are broadly recognised by investors as effective implementations of ESG considerations.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 Bloomberg Multiverse as of 31 December 2019,

2 Phillips, Y. (2019). “2019 Annual ESG Manager Survey”, Russell Investments Research. Available at: https://russellinvestments.com/uk/insights/articles/2019-annual-esg-manager-survey

3 See endnote 2.

4 Russell Investments is a Climate Action 100+ signatory since 2020. https://www.climateaction100.org

5 Russell Investments is a PRI signatory since 2009 and a supporter of TCFD since 2019.

6 Financial Stability Board.