Five key questions organisations should ask when choosing a Fiduciary Management provider.

An early Christmas present – should you have opened it?

It is Christmas 2019. The last few weeks of the year are always unique, but this year they have been more of an assault on the senses than normal. Coupled with crying over Christmas ads, the stress of last-minute shopping and worrying about over-eating during the holidays, we’ve also had the post-election hangover. The only thing that remains is the pre-payment of a full year of gym membership and the rush to wrap up meetings at work to go!

You would be excused for not noticing an early present under your tree, and it is from someone you might not know so well. A little bit like secret Santa.

If you are a pension trustee, on 10 December, you received a gift from the Competitions and Markets Authority (CMA). It is a clear set of instructions on what to do if you are looking to adopt Fiduciary Management (FM), or already have one such arrangement in place.

For some, it’ll be a gift you didn’t really want, but one that you still have to wear so as to not offend your family member staring at you with a beaming smile on their face. For others, it is as welcome as a glass of mulled wine on Christmas Eve.

But, either way, there is no option to exchange the gift. Let’s see how you can make the most of it.

What's inside the wrapping paper?

If you are looking to adopt FM for the first time, you will now need to consider at least three firms as part of a competitive tender. Although additional work for some, this is definitely good governance – you do want to get the best deal and find a long-term partner.

And partner is the right word. While you may well already have a trusted investment consultant, working with your FM provider can become an even closer affair. It does become a true partnership, with your provider’s phone number most likely listed on speed dial alongside your family and friends.

If you already have an FM arrangement in place, there are a few alternatives. If you’d originally appointed that provider through a competitive tender, you are in the clear. You might review them at some point, but at your discretion.

If you have not run a competitive tender to start with, you have either five years since appointment, or until 10 June 2021 to complete a re-tender, whichever is later.

How to go about it?

You will need to invest a reasonable amount of time in this process, regardless if it’s a new search or a re-tender process. But this should be seen as a good investment, rather than an unwelcome burden.

If you have sufficient resources and/or knowledge in-house, you may well feel able to do this yourself. The work required will typically involve drafting a questionnaire, evaluating responses, and then most likely narrowing down the choice of FM providers to present to the trustees

The alternative is to appoint a specialist firm to help you select the FM provider that will best fit your scheme. They are called selection consultants – many have been undertaking these searches for some years and have a very good understanding of different FM offerings in the market.

Hiring a selection consultant will attract a fee, but for many pension schemes, this will be a worthwhile investment. These independent consultants can guide you through the process, design the right questions, scrutinise providers’ answers, and use their experience to best match you with an ideal FM partner.

This may be a significant expense for smaller schemes, however, there are lower-cost options available, or alternatively, trustees can seek help from their actuary, independent trustee or run it themselves.

How do you choose?

FM providers come in different shapes and sizes, like gingerbread cookies.

To choose the cookie that both looks and tastes the best, we have listed below five key questions that trustees should ask during the process, and maybe include as part of their questionnaire:

Q1: Can the FM provider give clear and proactive advice?

At the heart of an FM, proposition remains the provision of high-quality advice. It needs to be timely, clear and presented in a way that enables trustees to make decisions. Reams of material are probably too much. A black box just trust us approach is worse.

Look for an FM provider that can tailor their communication approach to fit the style of your trustee group.

One way to get a taster for what it would be like working with a particular FM provider is to ask them to deliver a short trustee training session as part of a final stage presentation. We saw this organised by one of the selection consultants and it worked extremely well - the trustees got a first-hand experience of working with the FM providers and it made the session highly interactive. It provided them with much more insight than a generic presentation or a simple written proposal would.

Q2: Does the provider have FM at the core of their business?

When we hire investment managers on behalf of our pension clients, we look for focus and dedication to the strategy they specialise in. Specialisation leads to better results, usually through the dedication of accumulated expertise and resources.

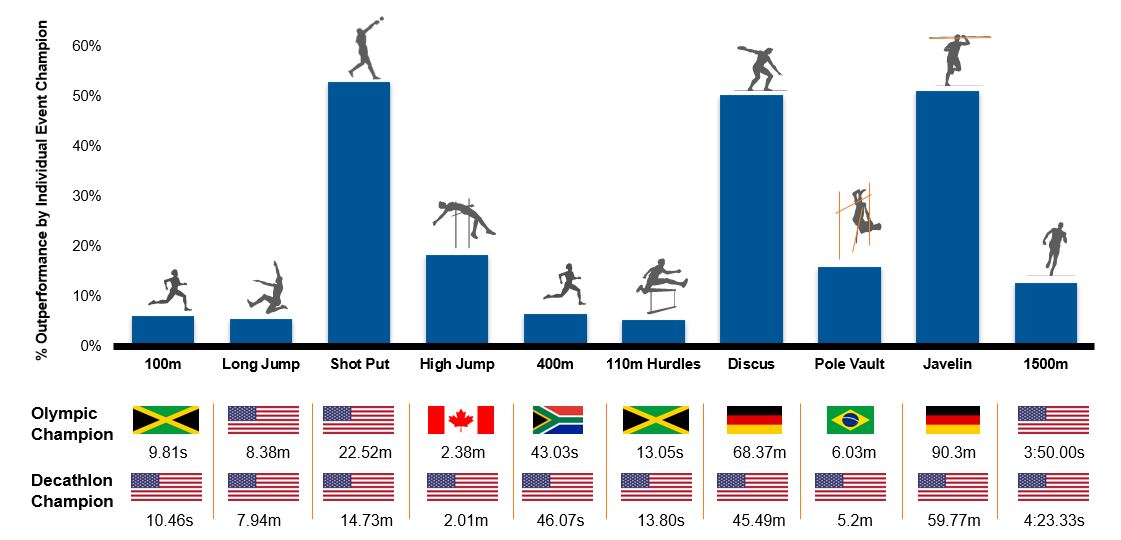

There are a number of examples of this. As we head towards another Olympic year, one that clearly illustrates the benefits of specialisation is the decathlon versus the individual, constituent events. The event specialists achieve greater results in each individual discipline.

Source: Rio Olympic Games results 2016. For illustrative purposes only.

Furthermore, experience is crucial. Those that have been in the FM market for many years, if not decades, have encountered the hurdles, and created solutions.

Would you look to hire someone who is only entering the FM race now, or someone who has been working with pension schemes for decades and will continue to invest in FM at the core of the business?

Q3: Can the provider really find the best managers in the world?

Your current investment consultant is probably already helping you select and appoint investment managers.

However, there should be an improvement under an FM approach.

Your access should improve. The FM provider should use their scale and research platform to identify investment managers that are critical to your success as a pension scheme. In addition, your pace of implementation should also be accelerated.

In some areas, such as passive equities, manager selection is arguably less important, since a number of providers can probably track the benchmark relatively well.

However, there are many asset classes that can provide a valuable and diversified source of return, but can’t be accessed through a passive approach. This is where you should test your FM candidates and ask them to demonstrate both their process and value-add in manager selection.

However, beware, some providers can use their in-house solutions to fill in the gaps in their research coverage. You should stay alert to this potential conflict of interest.

Q4: Is it the entire solution cost-effective, or just 'cheap'?

There is a difference. You can’t have the best-tasting gingerbread cookie if the ingredients are not of high quality, and this will undoubtedly come at a cost. Anyone promising to create such a cookie at bargain-basement prices is most likely an alchemist.

As Trustees, you should focus on value for money. Whether you are aiming for buy-out, self-sufficiency or just getting to full funding on your Technical Provisions basis, all elements of the FM solution should work in harmony together – alignment of advice with actuarial input, allocation to the right asset classes, good returns from managers, robust risk management, cost-effective implementation, good quality reporting, frequent meetings to review progress, effective communication…the list goes on.

Better ingredients for your cookie might cost more, but they are likely to deliver increased satisfaction for your members.

Q5: Are the fees fully transparent?

Fee transparency is now mandated by the CMA. When FM providers submit their proposal, they will separate their fiduciary fee from those of underlying managers, amongst other requirements.

However, the key will be to for you as trustees to have ongoing visibility into what costs you are incurring. You should ask your FM candidates to show you samples of their invoices – ideally, they will be prepared on a quarterly basis

Apart from being on top of total costs, this reporting will also help you track the FM provider’s ability to pass on manager costs savings. For example, FM providers should use their scale to negotiate fees charged by specialist investment managers in your portfolio. These savings should be fully passed on to you and reported back regularly.

Can I please go back to planning for Christmas?

Yes, and thank you for reading this far.

You will no doubt be extremely busy over December and into January, but after a deserved break, you should probably come back to this article and check out some of the steps we recommend you take before appointing a fiduciary manager or reviewing your current one.

Wishing you all the best for 2020 and beyond!

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.