The impact of today’s low-interest rate environment on investors

In response to the global COVID-19 recession, central banks across the world unleashed synchronised monetary stimulus to backstop the economy, driving short-term and long-term rates downward. How long will interest rates stay low? And how does this low-interest rate environment impact borrowers and investors?

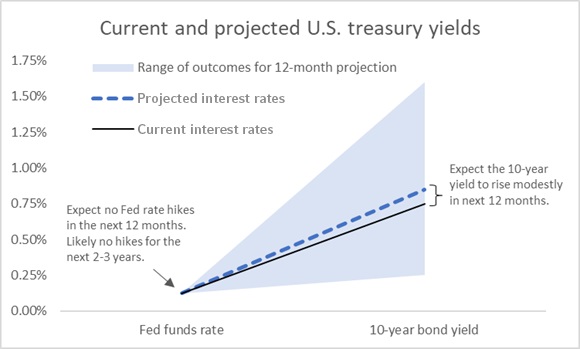

Low interest rates are here to stay

Global interest rates will likely stay near current low levels for at least the next couple of years because central banks globally will feel little pressure to raise interest rates any time soon.

Short-term interest rates are determined by central banks. Longer-term interest rates, like the U.S. 10-year Treasury yield, are determined by the average expected short-term rate over the next 10 years, plus some term premium (to compensate investors for the risk that actual short-rates may differ from expectations). Thus, central bank actions, and guidance for future actions, will directly impact short-term and long-term yields.

- Average inflation targeting will delay rate hikes:

The U.S. Federal Reserve (the Fed)'s dual mandate is to foster maximum employment and stable prices by controlling short-term interest rates - lower to stimulate economic activity, higher to cool economic activity. In the past, the Fed may have raised rates if inflation had crept toward their 2% inflation target. The recent shift to an average inflation targeting policy raises the bar for a rate hike - essentially keeping rates low for longer. Because U.S. inflation has been so muted over the last expansion and recent recession, the Fed will tolerate an inflation overshoot to make up for past inflation undershoots, such that the average inflation over a cycle is around 2%.

- No inflation pressure during early cycle recovery:

The three usual drivers of inflation are market expectations (a self-fulfilling prophecy), demand-pull (increased aggregate demand for goods) and cost-push (higher production costs). There is little inflation pressure coming from these sources today, especially given we are in the early recovery phase of the global business cycle.

After a recession, economic activity recovers, but remains far away from levels that generate any inflation pressure. The high unemployment rate puts a cap on any frenzied consumer spending, even with the government’s previous fiscal stimulus. The high unemployment rate also creates downward pressure on employee wages, which drives down production costs. Production costs may also remain low because governments are less likely to raise taxes while the economy is still in recovery. Furthermore, market expectations for future inflation are low.

With the lack of inflation pressure, and higher tolerance for inflation overshoots, central banks are likely to keep interest rates low for a long time.

Click image to enlarge

Source: DataStream, Russell Investments.

Impact of low interest rates on borrowers

It’s great to be a borrower in a low-interest rate environment. Issuing debt is cheap, especially if you are a government, consumer, or business with a strong credit rating.

For governments, lower interest rates make high government debt more sustainable. For the consumer, lower interest rates may mean you can afford a better house with the same mortgage payments. For businesses, the access to cheap debt may fund innovative projects, upgraded capital, or other productive business investments. Business growth may increase future cash flows and increase its stock price. Depending on an individual organisation’s situation, issuing debt may be another lever they can pull to improve their overall financials, if the cost of doing so is manageable.

Impact of low interest rates on investors

The early recovery phase of the business cycle is usually favourable to equities over bonds. Low discount rates and low borrowing costs can fuel an equity market rally. For bond portfolios, returns come from yield and price changes. Low returns are expected because 1) yields are depressed from low interest rates and 2) price increases are limited by how high bond prices are already. Generally, low-interest rate environments are beneficial to longer-term portfolios (which take more risk and have higher allocations to stocks) and disadvantageous to shorter-term portfolios (which take less risk and have higher allocations to bonds). For consumers to meet their near-term retirement goals or for businesses to meet their near-term liabilities, they may need to increase their portfolio’s risk profile and search for yield in credit markets.

A low-interest rate environment also dampens the diversification power of bonds. In risk-off environments, investors usually rush to safe-haven assets like U.S. Treasuries. Because the 10-year Treasury yield is already low at 75 basis points, and yields have a natural lower bound around 0 basis points (as long as the Fed remains averse to the idea of negative interest rates), there is a limit to how much further bond yields can fall (and bond prices can rise). Under a low-interest rate environment, U.S. Treasuries may still help diversify a portfolio, but the upside benefit to bonds is limited after a risk-off event. Consider supplementing bonds with safe-haven currencies.

The bottom line

Global rates are likely to remain low for a while. Today’s low-interest rate environment creates some challenges for investors looking for adequate returns through bonds, but great opportunities for borrowers and equity investors.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.