Worried about inflation? Let’s take a trip back to the future.

Everything in perspective.

It’s a phrase we’ve all heard, and we generally believe to be true. Just think about how your perspective has changed on dining out, home offices, or baking, knitting and other home-bound activities since the pandemic began. As with most things in life, your perspective depends on your experience.

That got me to thinking about some of the recent headlines on inflation. For those of us who came of age in the past two or three decades, inflation has been generally benign and rarely an issue. But for investors who have been in the markets a lot longer, the latest inflation numbers may revive memories of the early 1980s. So I thought it might be worthwhile to do some historical comparisons.

One of the most eye-opening headlines I’ve seen was the startling news that the Social Security Administration is raising its benefit next year by 5.9%. Inflation is the highest that we’ve seen in a long time, and there are a few comments going around the internet on how to address it. One that keeps cropping up is that the current inflation rate is transitory. That’s been said for more than a few quarters now, which has led to another comment going around the internet: All inflation is transitory, until it’s permanent. It’s a tongue-in-cheek response, but historically true.

When I saw that the Social Security benefit increase was the largest in decades, I wanted to know when was the last time the benefit was bumped by such a significant amount. It’s been nearly 40 years! In 1982 the benefit was raised by a whopping 7.4%.

I wondered what the interest rate environment was like at that time to prompt such a huge increase. The direction of interest rates seems to be the topic du jour for the advisers I work with and understandably so. Fixed income is a headwind for portfolios with its current lacklustre performance and low rates on new issuance. A cursory Google search into bond yields in 1982 returned some downright shocking information. Bonds were yielding an average 14% at that time. Mind-blowing. So even though inflation was a concern, you were able to easily overcome its impact for your most conservative clients. Even certificates of deposit (CDs) were returning mid double-digit rates.

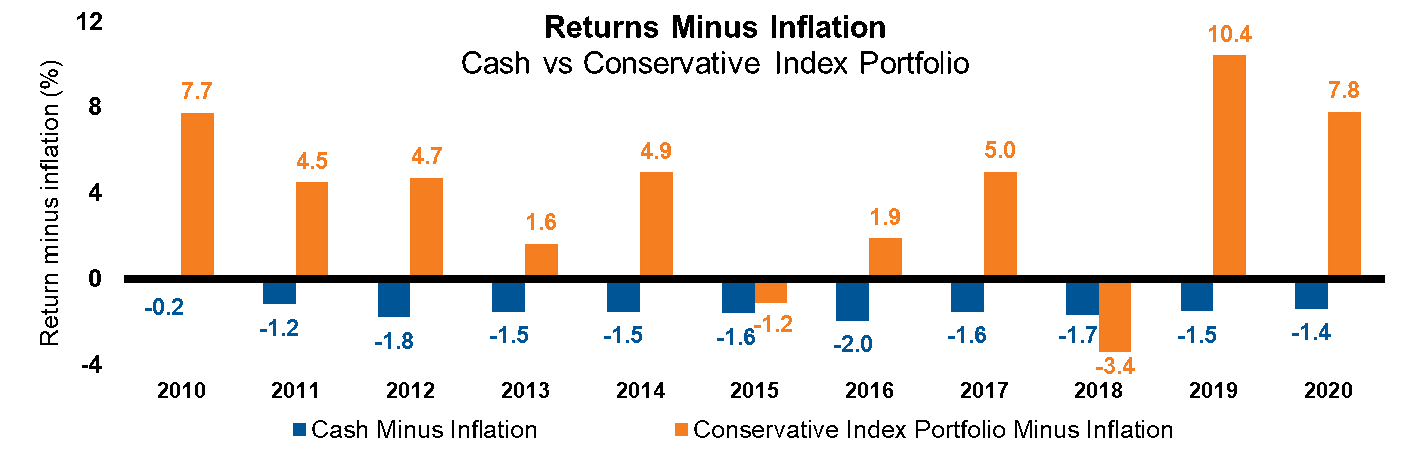

We haven’t had sizable, sustained inflation for some time, so it’s easy to forget its effect: Inflation is one of the biggest detractors of wealth creation (taxes is the other largest one). Take a look at the chart below to see the difference in performance between a conservative 20% equity/80% fixed income portfolio and a cash position over the past decade on an inflation-adjusted basis. Today is different.

Inflation: The hidden cost of cash

| Example | Cash | Conservative Index Portfolio |

| 2020 return | 0.3% | 9.5% |

| 2020 inflation | 1.7% | 1.7% |

| 2020 return minus inflation | -1.4% | 7.8% |

Sources: St. Louis Federal Reserve and Morningstar. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly. Cash returns represent national rate on 12-month jumbo Certificate of Deposit (CD). Conservative Index Portfolio represents 80% Bloomberg US Aggregate Bond Index, 13% Russell 3000 Index, 5% MSCI EAFE Index and 2% FTSE NAREIT All Equity REITs. Inflation represents Core CPI.

Today is a lot different. CDs, affectionately called by one adviser I work with as certificates of depreciation, haven’t been helping investors meet their financial goals. And there is more money than ever sitting in cash and equivalents: roughly $21 trillion dollars as of 30 September 2021.1 This low-return environment brings a lot of risks to the forefront for your more conservative clients, such as inflation risk/purchasing power risk, longevity risk and risk to their overall financial plan. Your clients are likely to continue to have the same objectives they’ve always had - such as a secure retirement, home ownership, or funding education - but, how they are going to get there might need a halftime adjustment.

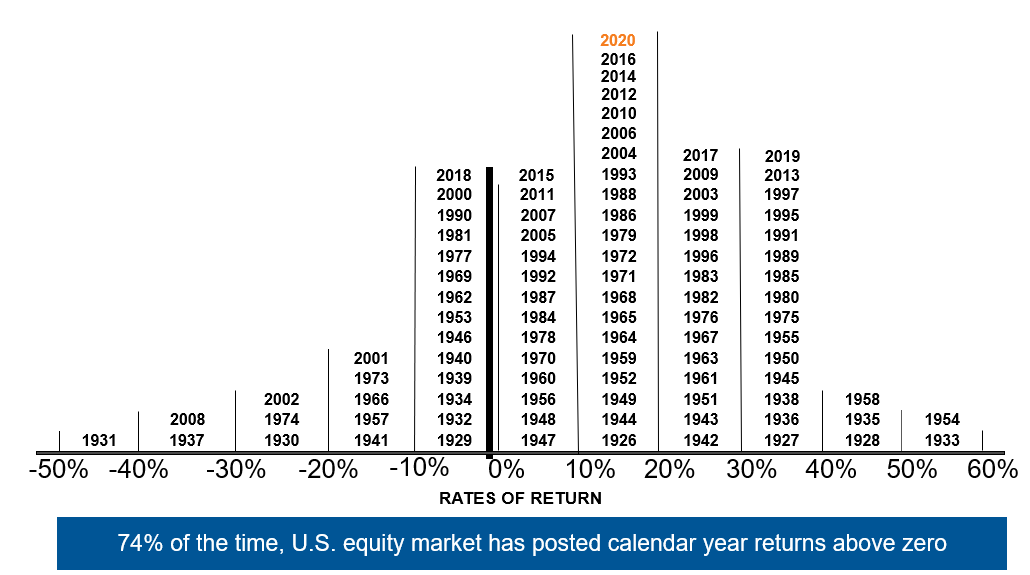

While some more conservative investors might be reluctant to own equities because of even the slightest bit of risk, they’re likely needed in most portfolios. Historically, equities have been a consistent contributor to portfolio performance, as they go up far more frequently than they go down. A little exposure can keep you ahead… and usually does.

Historically it has paid to own stocks

Calendar year S&P 500® Index returns 1926-2020

Represented by the S&P 500® Index from 1926-2020. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

This is where a thoughtful and educational conversation with your most conservatively invested, or not invested, clients will reap rewards. Stocks and bonds generally balance each other out. To get the return desired to stay above inflation shouldn’t be an adrenaline-pumping and fear-inducing prospect. Often we think of a three- to five-year time horizon as appropriate for a likely positive return on a 60% equity/40% fixed income portfolio. And it generally is. But for those on the conservative end of the risk spectrum, it doesn’t take long for a likely positive return. As the chart below shows, at the one-year mark on a 25% equity/75% fixed income portfolio, there was a 94% likelihood of a positive return as of 31 March 2021. At three years it was 100%.

Cash on the sidelines?

Historically it has paid to be invested

Three Index Portfolios comprised of S&P 500 Index (S&P500), MSCI EAFE Index (EAFE), and Bloomberg U.S. Aggregate Bond Index (AGG). 25% Equity: 17% S&P500/8% EAFE/75% AGG; 50% Equity: 34% S&P500/16% EAFE/50% AGG; 75% Equity: 50% S&P500/25% EAFE/25% AGG. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

One of the primary objectives as a financial adviser is to put individuals and families in a position to meet their investment objectives while mitigating risk. We can’t eliminate risk completely, but advisers can work to minimise it and offer greater security to the financial plan. The U.S. Federal Reserve has openly acknowledged that it wants inflation at 2-2.5%, and is likely to pull the levers at its disposal to achieve that. Since bonds and fixed rate instruments aren’t keeping pace (and might lock you in for a sizable term) what do you do?

- Have a conversation

- Talk about the past, present and future. Are their goals and time horizons the same?

- Educate your clients on the current environment

- Do they understand the lasting effect inflation and low rates might be having on their account?

- Revisit different options to maintain their current trajectory for their investment goals (I think about my son’s university fund and the long-term benefit of a bit more risk now).

- Keep perspective

- While their mortgage rate might be the lowest they’ve ever had, their money might be growing at a slower pace than it ever has.

- The investment options they’ve used before might not be doing the job in the current situation.

Like I said, their objectives have likely gone unchanged, but how they get there might need an adjustment.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 Based on M2 money supply. a measure of the money supply that includes cash, checking deposits and deposits that are easily converted to cash, such as bank accounts. Source for M2 data: St. Louis Fed. https://fred.stlouisfed.org/series/M2SL