Market concentration and the Magnificent Seven: Where next?

Executive summary:

- The Magnificent Seven stocks (Microsoft, Apple, Alphabet, Amazon, Nvidia, Meta, and Tesla) have been the largest driver of equity returns in recent years and were again the dominant contributors in 2023, accounting for more than half of the market increase.

- Market concentration is nearing its highest level in more than 50 years, with technology and related sectors now comprising more than 40% of market cap, and the 10 largest companies accounting for more than 30% of the market.

- While the large technology companies undoubtedly possess formidable competitive advantages, prior rotations in membership among the largest companies by market cap suggest that on a relative basis, investors would do well to diversify their exposures.

The Magnificent Seven save the day

Younger investors could be forgiven for not knowing the current Magnificent Seven moniker has its origins in the classic 1960 western film “The Magnificent Seven” starring Steve McQueen and Yul Brynner, which is itself a remake of Akira Kurosawa’s “Seven Samurai”. In the movie, the farmers in a poor village hire rogue gunfighters to protect them from marauding outlaws who raid their village and take their hard-earned food and provisions.

In much the same vein, investors have flocked en masse to the Magnificent Seven stocks in recent years not only for their attractive expected long-term growth profiles, but also for their potential protection from the erosion of purchasing power due to inflation. This broad appeal has driven significant outperformance for those stocks over time; that was again the case in 2023 and continues so far in 2024.

For calendar year 2023, the Russell 1000 Index returned 26.5%, led higher by stocks within the technology (+56%) and communication services (+54%) sectors. The Magnificent Seven as a group did even better, with an average total return of 105% leading the group to contribute more than 62% of the overall gain in the index over the course of the year. That degree of outperformance has resulted in the Magnificent Seven now constituting 27% of the Russell 1000, with the top ten holdings representing 31%, a degree of market concentration unprecedented in decades.

The market environment today

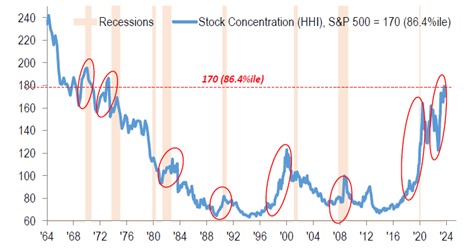

Market share and market concentration can be measured in a number of ways. The Herfindahl-Hirschman index (HHI) is one of the most popular methodologies and is widely used to measure market concentration and competitiveness by assessing the size of individual companies relative to the overall size of their industry. The same methodology can be applied to market shares within the equity market, comparing individual company market caps to the overall capitalisation of the market to arrive at a measure of market concentration.

The below chart from JPMorgan uses the HHI to calculate the relative concentration of the S&P 500 over the last 60 years. The significant increase in market concentration can be seen in the steeply rising blue line since 2016. After a pause in 2022, market concentration is now at its highest level since the early 1970s when the Nifty Fifty stocks dominated the U.S. stock market and is well in excess of the prior tech bubble ending in 2000.

Concentration within the S&P 500

Source: JP Morgan. Data through Jan. 31, 2024.

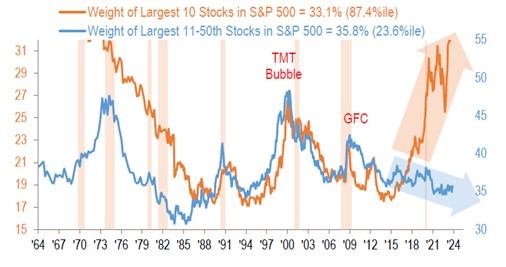

While illustrative of the overall trend in market concentration, the HHI arguably understates the true degree of market concentration within the U.S. equity market. The below chart shows the weight of the 10 largest stocks in the S&P 500 compared with the weight of the 11-50th largest stocks. The two lines historically have moved together as broad themes play out in the market. As can be seen below, however, the divergence between the two groups is significant since 2016, with the weight of the 10 largest stocks nearing its highest level since the 1970s, while the weight of the 11-50th largest stocks is no higher than average.

Relative weights of the largest stocks within the S&P 500

Source: JP Morgan. Data through Jan. 31, 2024

What does the future hold?

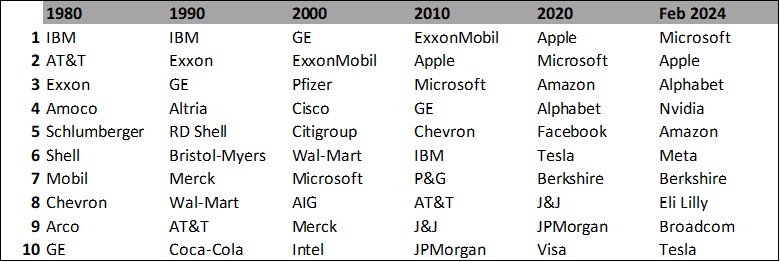

It is beyond the scope of this post to assess what the road ahead may look like; the market outlook is best left for our investment strategy team. That said, looking at prior episodes of market concentration and the tally of the largest companies in those markets can be illustrative of long-term relative performance. The below table lists the largest companies in the S&P 500 by decade, starting with 1980 and continuing through the present. While there are some stalwarts with multiple appearances over the decades (Microsoft, ExxonMobil), change in the composition of the top 10 companies is the norm.

Largest U.S. companies by market cap by year

Source: S&P, Russell Investments

While the large technology companies comprising the majority of the current top 10 list undoubtedly possess considerable competitive advantages and have been diligent in erecting formidable barriers to entry for would-be competitors, it is the nature of competitive markets, particularly within newer, rapidly evolving industries, to adapt and change over time.

Active managers have long differentiated between the diverse business models, incremental returns on capital, and relative valuations of the Magnificent Seven. Prior capital-light advertising-driven models are giving way to higher capital intensity AI-driven models. Consumer goods-focused companies are facing increased competition, driving down incremental returns. Potential competitors within AI are being made partners with an eye toward keeping regulatory authorities at bay.

Performance of the Magnificent Seven since the end of Q3 2023

Source: Bloomberg, Russell Investments

The bottom line

After trading together for much of 2023, the market is beginning to take note of the changes underway, with a sharp divergence in the fortunes of the Magnificent Seven over the past four months. Ultimately, the returns of the Magnificent Seven stocks in the long run will be driven by the underlying performance of their individual operating models. While making no prediction about the specific companies here, we believe active managers will be able to differentiate the relative prospective returns of each and position their portfolios accordingly. It is often said that diversification is the only free lunch in markets. Investors would be well served to remember that in “The Magnificent Seven”, only three of the seven gunslingers make it out of the final battle alive.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.