Multi-Asset Growth Strategy Review & Update

David Vickers, Head of Multi-Asset, EMEA and Thomas McDonald, Portfolio Manager, provide an update on how the Russell Investments Multi-Asset Growth Strategy (MAGS) has performed in recent months, outline how the portfolio was positioned in the period leading up to February 2020, and whether there are any forward looking opportunities amidst the heightened level of volatility.

Diversification and defensive mechanisms

2019 saw excellent returns across the majority of asset classes, with 2020 starting in a similar way.

In 2019, as equity markets rallied to overvalued levels, global economic growth slowed down and manufacturing ground to a halt, we sought to reduce overall portfolio risk. Firstly, we progressively removed the exposure to equities, offsetting the drift that had occurred as equities rallied. This gradual reduction in equities ensured that the MAGS portfolio was not over extended when the market turn came. We also added government bonds throughout the year, with a focus on the U.S. and Australia, due to yields being higher in these countries and greater potential for future interest rate falls. The result of this was that going into 2020 we had the highest interest rate duration that the MAGS portfolio has ever held since inception.

The other step we took was to increase the exposure to the Japanese yen. The yen has historically been added as a good stabiliser in portfolios during ‘risk off’ events. In addition, we added equity protection to the portfolio, which was originally intended to cover the trade war risks.

Click image to enlarge

Source: Russell Investments Multi-Asset Growth Strategy, asset class breakdown as at 31 December 2019.

Downside Protection, Dynamically Traded

News of the coronavirus came to public attention in January, but apart from a selloff in emerging market equities and commodities, developed markets responded with a collective shrug and continued to rally through to February, assuming the virus was contained within China.

During the brief window of calm before there was a breakout in the West, we took further action to insulate and protect the portfolio. Specifically, we purchased a put option in late January on the S&P500 (U.S. equity market), with a strike price of 3250 and a maturity of December 2020. When volatility is low like it was in January, this insurance is very cheap.

As the extent of global virus situation became better known and volatility spiked, we took the opportunity of selling a put option, again on the S&P500 but at a much lower strike price (2350). This locks in protection between 3250 and 2350 (roughly a 30% zone of protection), and importantly we were able to do this at zero overall cost. This put option spread is illustrated in the diagram below.

Click image to enlarge

S&P500 put spread option

Source: Russell Investments as of March 2020.

Looking to the future, opportunities and positioning

We are now approaching a bear market, as defined by a 20% drawdown. Valuations have significantly improved, and we are now inclined to start modestly increasing the risk in the portfolio at more attractive levels. It is important to note that whilst we don’t know how bad the short-term virus impact will be, we recognise that a lot of bad news is already priced in, limiting downside potential from here and providing a platform if the situation does start to improve.

We can also observe other regional markets as a model for European and North American experience with the coronavirus. As an example, South Korea which currently has 7531 cases, has seen a significant reduction in the rate of growth over the last 7 days. The same pattern has been seen in China, outside of Hubei. If Europe and the other affected countries follow this pattern, the rate of growth is likely to significantly slow down over the coming weeks.

In addition to the slowdown of the virus spread, there are numerous stimulus packages being put into place. Prime Minster of Italy, Giuseppe Conte, was discussing stimulus leeway of up to €16 billion, which would be approximately 0.9% of GDP. In the UK, the Bank of England made an emergency interest-rate cut of 50 basis points to 0.25%. This was shortly followed by the Budget announcement; finance minister Rishi Sunak pledged a £30 billion stimulus package as he seeks to prepare the British economy to fight the potentially devastating impact of coronavirus.

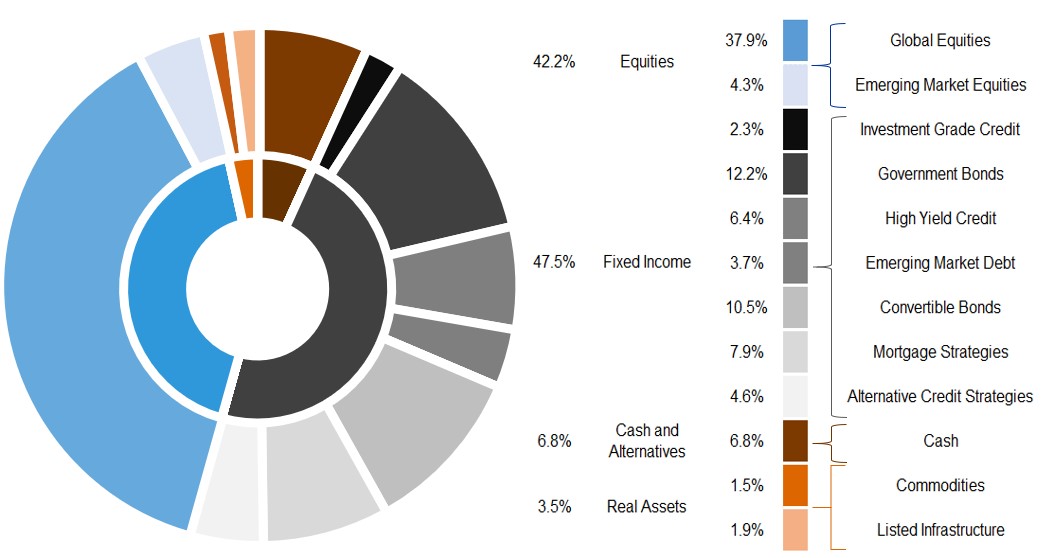

The below chart shows our current asset class breakdown in the MAGS portfolio as of March 2020.

Click image to enlarge

Source: Russell Investments / Bloomberg as at 9 March 2020.

For Professional Clients Only.

This material does not constitute an offer or invitation to anyone in any jurisdiction to invest in any Russell Investments Investment product or use any Russell Investments Investment services where such offer or invitation is not lawful, or in which the person making such offer or invitation is not qualified to do so, nor has it been prepared in connection with any such offer or invitation.

Unless otherwise specified, Russell Investments is the source of all data. All information contained in this material is current at the time of issue and, to the best of our knowledge, accurate. Any opinion expressed is that of Russell Investment, is not a statement of fact, is subject to change and does not constitute investment advice.

The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested. Any past performance figures are not necessarily a guide to future performance.