Pension funds - are you making the most of FX?

Professional Pensions recently interviewed our experts about the ways pension funds can harness the returns available from FX and currency management. In the final instalment of the Wire’s three-part currency series, hear from Van Luu and Mirjam Klijnsma.

Should pension funds be holding exposure to safe-haven currencies? If so, what's your outlook?

Luu: Due to the diversification characteristics typical of safe-haven currencies, it does tend to be beneficial - on average - to hold at least some exposure within your portfolios. That's because safe-haven currencies are those that normally increase in value and popularity when equities and other risky asset markets go down. They typically have a positive correlation with mainstream government bonds and see investors pile in when markets are volatile.

The Swiss franc and Japanese yen are two typical safe-haven currencies. Switzerland and Japan are both considered to have stable governments, central banks and financial systems. They both have large current account surpluses as well. As a result, investors hold a lot of confidence in their currencies and take shelter when times are tough.

They are the metaphorical glass of wine and fluffy blanket at home on a cold, stormy night: safe and comforting.

Of course, as the world's reserve currency, the US dollar has also exhibited safe-haven characteristics during the global financial crisis of 2008.

On the other side of the spectrum, we have cyclical currencies such as the Australian dollar, which suffer during periods of turmoil.

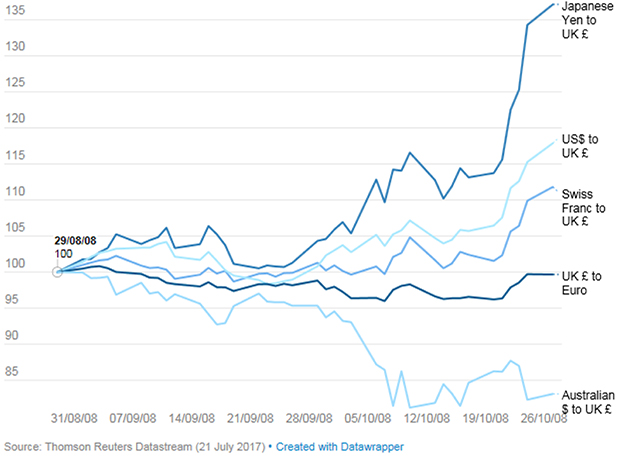

Safe-haven currencies versus GBP during the 2008 Global Financial Crash

The level and combination of exposure does however, really depend on the valuation and cyclical outlook for each currency. Taking these factors into account, we currently prefer the Japanese yen over the Swiss franc or the US dollar. The yen is as cheap as it has been for nearly 40 years while both the Swiss franc and the US dollar are higher than average.

To what extent, if at all, should pension funds be hedging currency risk across their portfolios?

Luu: Broadly, pension schemes invest internationally to gain exposure to the diversification benefits inherent in other assets and participate in global growth. The currency exposure they get from investing in foreign equity and bond markets is usually an unintended by-product of the asset, rather than a conscious investment choice.

Leaving currency risk unmanaged and completely unhedged is almost certainly not the best choice. It leaves investors exposed to ‘unrewarded currency risk' - i.e. uncapped exchange rate risk with no compensation.

Indeed, finding the ‘optimal' hedge ratio is difficult to achieve and can vary for different base currencies. A sensible investment strategy aims to reduce unrewarded currency risk while maintaining select diversification benefits of currency within the portfolio.

All investors should assess the impact unintended currency exposures have on portfolio volatility. In most cases, investors will find that implementing a currency hedging program is almost certainly better than no currency hedging at all.

What's the biggest risk for pension funds that don't hedge currency? Which strategy is the best approach?

Luu: For those that don't hedge currency, the greatest risk is that foreign currencies fall against your home currency - i.e. the one in which liabilities are measured. This reduces the value of your international assets and either means that future returns need to be higher, or contributions have to rise to make up for the shortfall.

It is often argued that currencies go up and down in big cycles and that it washes out in the long run, but why expose yourself to the intermediate swings?

Setting a strategic hedge ratio - and sticking to it - is a reasonable approach to currency hedging. When compared to an unhedged position, static hedging often reduces unrewarded and embedded risk without giving up expected return (when looking at an appropriately long period).

An even better strategy, in our view, is to allow the hedge ratio to be flexible. At Russell Investments, we think it's important to manage risk smartly by continuously responding to the valuations, economic fundamentals and sentiment changes that drive currency returns. This dynamic currency hedging turns the uncompensated and incidental currency risk from international assets into a rewarded source of risk. We use signals from currency factors to help us to help identify trends and provide insight into what the hedge ratio should be next.

To what extent are these factors responsible for currency returns? What are the main factors and how can they be used by pension schemes to enhance returns?

Luu: Pension schemes should consider evaluating currencies on a factor basis because they can become an intentional return source just in the way equities and bonds are. Currency exposures offer strong risk adjusted returns with low correlation to traditional asset classes.

Opportunities available in currencies can often be overlooked within pension schemes. While investors are indeed aware of the role that equity factors play in stock market returns (such as value or momentum), many haven't realised is that something similar applies to the currencies universe, too. Through our own analysis and academic research, we have identified that currencies with certain common characteristics deliver higher returns. This combined with an awareness of the changing market conditions, can in our view, achieve smaller drawdowns and a better balance of return to risk.

For example, currencies with high interest rates tend to have better returns than those with low interest rates. This is the carry factor. There is also the value factor in foreign exchange markets where currencies that are undervalued by purchasing power parity or similar concepts of equilibrium tend to perform better than those that are overvalued. Finally, trend factors look at prices to determine the near-term momentum and sentiment.

What's great is that we can use these insights from currency factors to inform those dynamic currency hedging decisions discussed in the previous question. As demonstrated in the chart earlier, we believe that the pound is cheaply valued at the moment. In particular, it's looking well valued against the US dollar which tells us to have a higher hedge ratio for US dollar assets than we have on average, based on the value factor.

Is there scope for schemes that currently hedge currency risk to reduce the costs of doing so? If so, what are the practical steps they can take to improve currency management?

Klijnsma: Over the last several years, the foreign exchange (FX) market has been plagued with scandals such as allegations of collusion and manipulation, which would have resulted in higher transaction costs for investors. As a result, investors have taken action to manage their costs and maintain appropriate governance over their FX trading program.

Unmanaged FX transaction costs can easily erode any returns generated by a hedging programme. Schemes can better manage their FX trading costs by taking the following steps:

- Ensure their manager has a deep counterparty panel that allows them access to abundant liquidity. Adequate liquidity allows the manager to complete trades and diversify exposure.

- Insist on time-stamps for all transactions. Time-stamps allow an independent transaction costs analysis provider to assess the execution quality.

- Utilise an independent FX transaction cost analysis (TCA) provider. An FX TCA is an excellent tool that allows investors better understand any execution slippage. At the end of the day, what gets measured, gets managed!