Private markets: Diversifying for the future

What is the role of private markets in the midst of the coronavirus? As the investment environment continues to evolve while investors adapt to the effects of the COVID-19 pandemic, we believe that private assets will play an increasingly important strategic role in fortifying portfolios over the long term, and that the current landscape provides compelling opportunities.

Obtaining private markets exposure through a multi-manager, multi-asset approach can provide investors with effective access and risk controls, in addition to operational and reporting efficiencies.

Why private markets?

An increasing number of investors are broadening their asset allocation across private markets – with the objective of obtaining exposures that can complement listed assets and have the potential to generate attractive risk-adjusted returns.

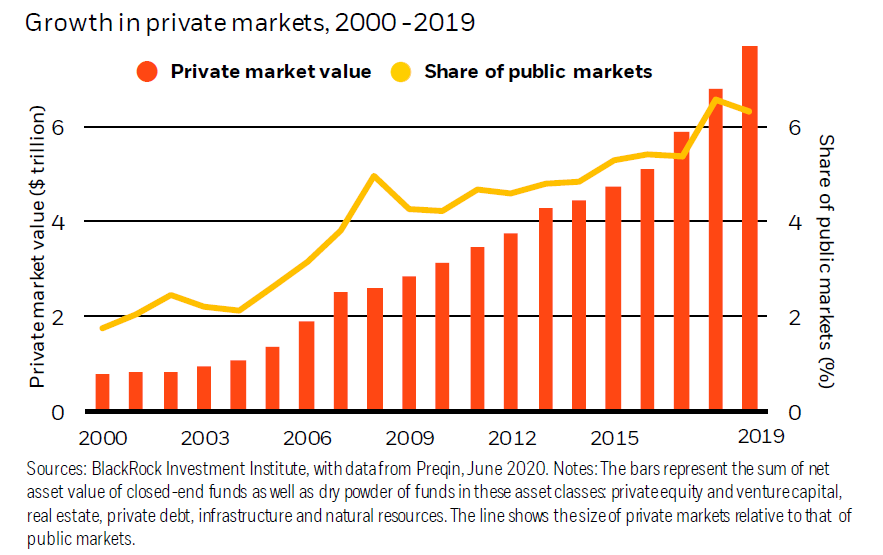

Capital allocated to private markets has tripled since the Global Financial Crisis (GFC), from $2.5 trillion to $7.7 trillion today. Private markets are a bigger and deeper component of institutional portfolios than ever before, making up 6.3% of public market size, from 3.8% before the GFC, as highlighted in the graph below.

Click image to enlarge

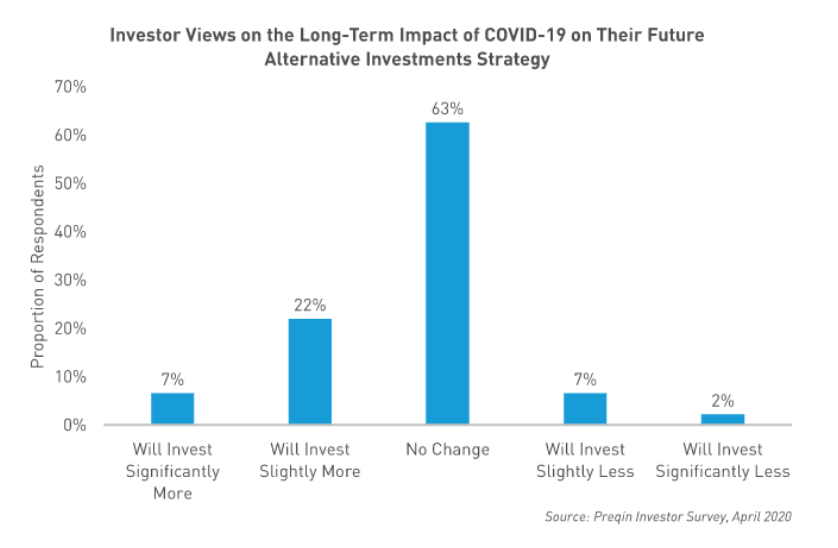

Data reflects that this trend is expected to accelerate. According to a recent Preqin industry survey of how investors are responding to COVID-19,1 almost a third of the respondents indicated that they plan to increase their allocation to more illiquid strategies, with less than 10% suggesting they will invest less.

In addition, market and economic stresses cause borrower default rates to increase, which would result in the need for additional capital for distressed and other special situations, such as restructurings. A poll commissioned by fund service firm Intertrust Group found that 92% of private equity professionals across North America, Europe and Asia believe that distressed fund activity will increase in the next 12 months2. The survey highlighted that the greatest themes for the next two years are expected to be distressed funds, specialist, sector-specific strategies such as funds targeting healthcare or technology, and debt funds.

Another factor signalling that additional allocations will be made is the record high level of unallocated cash awaiting investment. Commitments made to private markets, but that have not yet been called, are expected to be a catalyst for additional market transactions. Data from Preqin, Dealogic and other sources indicates that across funds dedicated to buyouts of established companies, venture capital, infrastructure, real estate, special opportunities and distressed funds, private equity managers have more than $2 trillion of dry powder to put to work. Those cash piles, if allocated to skilled managers and deployed to a diverse range of potential opportunities, can deliver attractive future performance.

Why now?

Amidst the current global market uncertainties, there has been an increased desire amongst many investors to strengthen diversification levels within their portfolios beyond traditional assets, which, by their nature, are affected by daily market price swings. Volatility is a risk many clients try to mitigate. In addition, with global interest rates low, and expectations that they will stay so for longer, some investors are also seeking income. The COVID-19 pandemic has created an opportunity for private markets managers to invest in areas that have been affected by the pandemic and market disruptions. With capital to invest, and a liquidity budget that can accommodate exposure to assets that are less liquid than traditional markets, increasing the weight of non-listed assets can be an appropriate action – to take advantage of the potential growth and income enhancement over the medium and long term.

Capturing economic recovery

In March, the COVID-19 crisis triggered a sharp selloff in financial markets, as economic activity slowed substantially following the social distancing and lockdown measures that were enacted globally to control the spread of the virus. Central banks and governments reacted quickly, taking unprecedented measures to support the economies. This has provided a necessary boost to the public markets. However, additional waves of infections and policy implementation remain as key risks for the remainder of the year, and likely beyond.

Unlike public markets, which have already priced in economic recovery and may look expensive, slower-moving private markets seem uniquely positioned to offer exposure to accelerating economic activity for the next couple of years. Relatively slower moving, less liquid private markets generally take longer to reflect changes in the broader environment, which offers additional opportunity in times of uneven economic recovery. Given the nature of the shock of the COVID-19 pandemic, we expect a wide variation in activity normalisation by region, sector and company. Private markets have the potential to capture this variation.

Biggest themes in tomorrow’s private markets investments

- Distressed debt: The pandemic has had an impact on quality companies hard hit by social distancing. Those companies might require short-term liquidity support, which is not being provided by banks. The distressed debt market, currently estimated at $600 billion, is expected to grow and become the most prominent theme in the short-term, according to a study by Intertrust Group.3

- Structural trends: Another set of opportunities lies in taking advantage of structural trends that usually accelerate after a big shock. We see such trends in sustainability, digitalisation and public health sectors. As estimated by Preqin and IJGlobal, renewable power already was the most active infrastructure sector in 2019, with technology and healthcare accounting for 19% and 13% of private equity deals, respectively, and the trends are only expected to accelerate in the world post COVID-19 outbreak4.

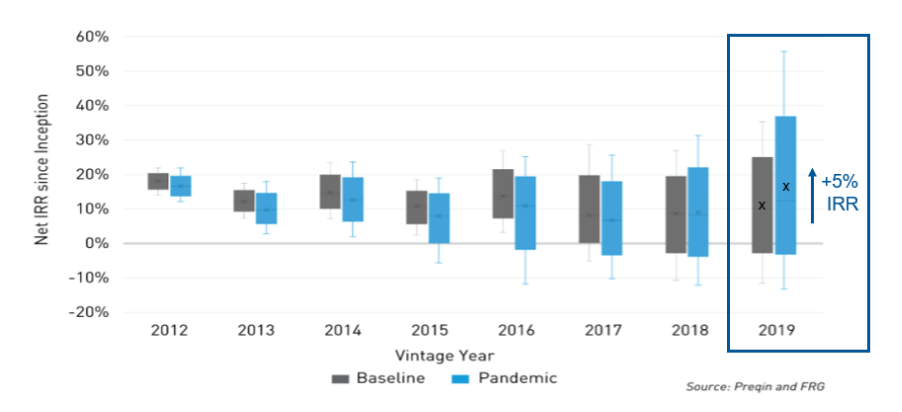

- Market disruption: Periods of market disruption can create attractive opportunities, and some funds launched after a market crisis have generated particularly attractive returns. However, the dispersion of returns within various private market strategies can be very wide, so selecting the best managers is critical to the outcome. As shown in the chart below, Preqin and FRG data reflects that internal rate of return (IRR) expectations have increased by 5% for funds launched in 2019, as they will be investing after the period of recent market disruption. Interestingly, the expectations of the dispersion of returns among managers have widened also, so selecting the best managers remains of utmost importance.

Date: As at 31 March 2020. The “X” represents median return.

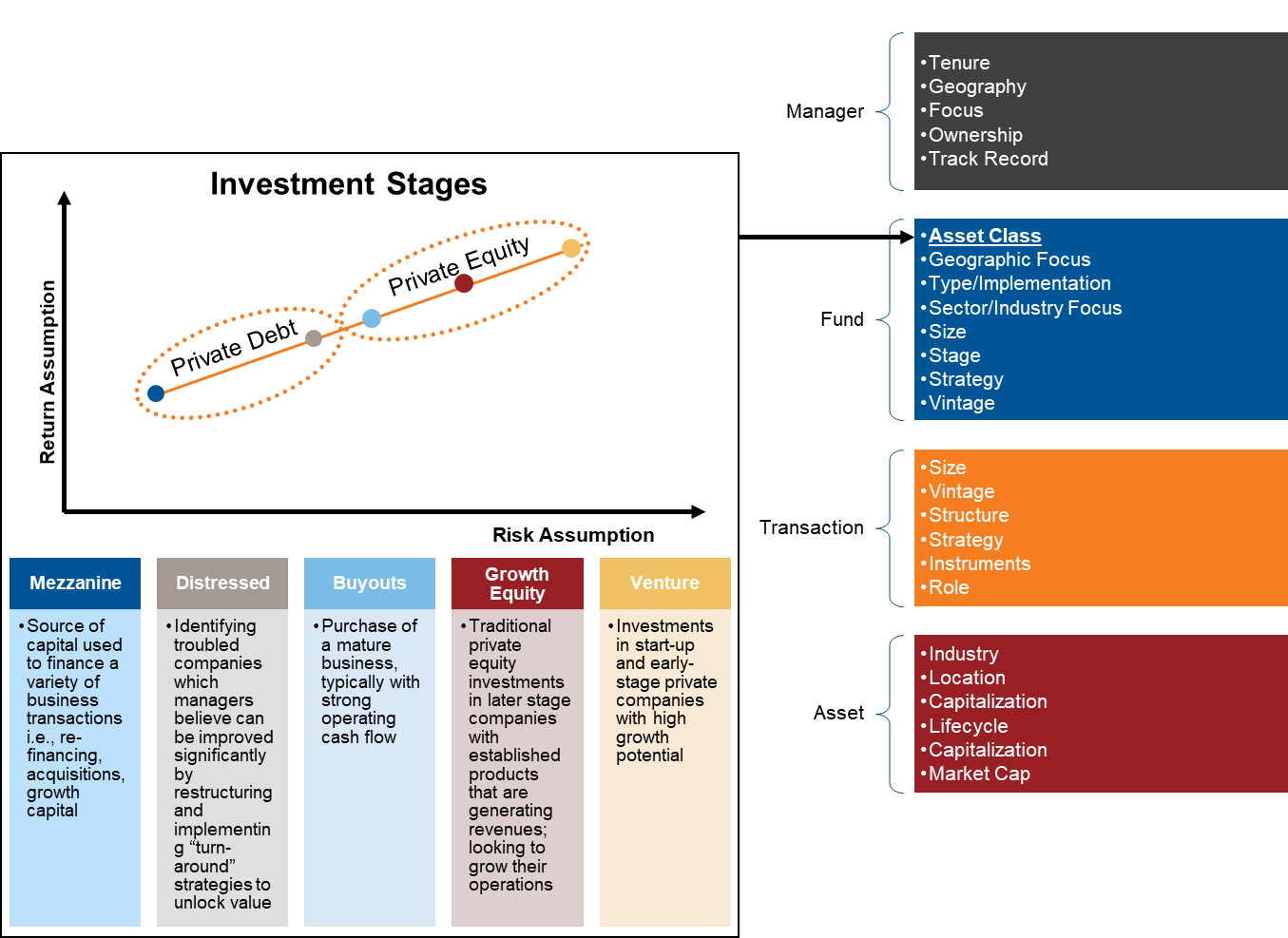

We believe that diversification beyond asset classes plays a crucial role in the private markets portfolio construction. A multi-asset and multi-manager approach to private markets provides access to the widest opportunity set while enhancing portfolio diversification properties. The graphic below gives an overview of the main areas of the private equity and debt markets.

The many uncertainties around the timing and shape of the broad economic recovery mean it is still too early to establish a complete picture of the impact of COVID-19. However, we do have some views and expectations regarding opportunities ahead across private equity, private debt and private real estate, among others. For example:

- Private equity: We anticipate favourable entry valuations for both primary and secondary private equity investments. Though the current valuations may not yet reflect the full impact of the pandemic, we believe the market will stabilise on lower valuations relative to pre-COVID-19 levels. Deal volume should rebound, and we believe there will be opportunities to participate in both primary and secondary transactions.

- Private debt: This category is increasingly viewed as an important source of liquidity and long-term finance for many companies. We see clear signs of opportunities for private lenders, particularly for those with expertise to evaluate and manage default risk.

- Real estate: Investments in real estate remain an important tool of portfolio diversification. While there is still uncertainty around certain sectors such as office and retail, there are other sectors such as industrial and multifamily that have not been challenged by COVID.

Why a multi-manager approach?

A multi-manager approach can offer unique diversification of opportunity set across a spectrum of private market managers and underlying investments, without being restricted by a narrower range of opportunities from a single manager.

We believe a best-practices approach utilises a wide range of instruments and research, exploiting market inefficiencies and providing greater portfolio risk-return characteristics than standalone allocations. This approach is further enhanced by robust governance. A robust investment process does not conclude upon investment. Continual oversight and interaction with fund managers ensure that managers are consistently aware of the expectations from both a financial and impact perspective – and that both objectives are continually aligned.

Finally, a multi-manager approach can be an efficient way to overcome the diseconomies of scale. Many of the most attractive opportunities within this space come in smaller deal sizes, which are accessible by boutique managers with specialist skills, but which often are below the investable universe for larger mainstream managers. Conducting robust due diligence on these types of managers requires specialised investment and operational due diligence skills and can be challenging for investors.

The bottom line

Private markets provide a broad spectrum of opportunities across a variety of market cycles. Slower moving, not immediately repriced private assets offer natural diversification benefits to portfolios containing only listed assets, while also having a potential to generate attractive returns. The impact of COVID-19 on financial markets has created both opportunities and risks, which can be navigated and capitalised on if working with a trusted investment partner. As an increased number of investors now turn to private assets in pursuit of returns amid the global low rates environment, we believe it is more crucial than ever to conduct a thorough research and selection process of the best managers in order to build resilient and well-diversified portfolios.

3 Intertrust Group. Distressed Funds Set to Flourish in Post-COVID World, June 2020.

4 2019 Preqin Global Alternatives Reports.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.