Short term volatility and long term planning

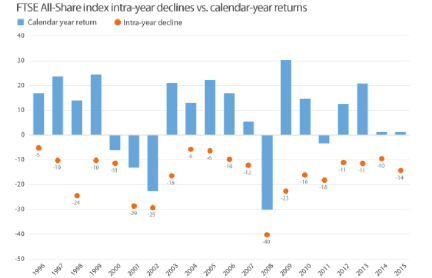

Intra-year declines and Calendar Year returns

Everyone feels rattled when stock-markets drop suddenly and unexpectedly. When the markets get messy like this, generally it’s because investors (institutional as well as retail) lose confidence. No matter how well portfolios are positioned, we must acknowledge that stock-markets can sometimes go down via the elevator and come back up via the staircase.

Intra-year declines refer to the largest market fall from peak to trough within a calendar year. The chart below helps demonstrate that these happen frequently, but more often than not the markets still reported a positive gain for the full calendar year. Whilst these can be periods of panic amongst both retail and institutional investors, staying calm (and staying invested) is crucial. Even in 1987, despite ‘Black Monday’, investors in the FTSE All-share index realised a calendar year return of + 4%.

Source: FactSet, FTSE, Russell Investments. Returns are based on Total Returns in GBP, including dividends. Intra-year decline refers to the largest market fall from peak to trough within the calendar year. Returns shown are calendar years from 1996 to 2015. Data as of 31 December 2015.

Is diversification still relevant?

When markets ‘go south’, investors (and the media) tend to focus purely on the returns of the equity markets. Whilst US investors will be closely monitoring the S&P500, UK investors will be watching the movements of the FTSE100 like a hawk. The FTSE All-share chart above is therefore useful in helping investors understand that volatility in stock-markets is in fact normal. ‘In the moment’ it may feel exceptional, but it is in fact fairly ordinary.

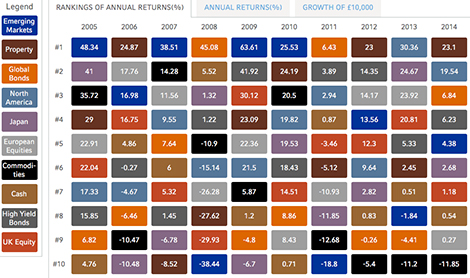

However, it is likely that in reality investors who are receiving professional advice will have portfolios that are not invested 100% in equities (and we would hope certainly not be invested in only one equity asset class). At Russell, irrespective of a client’s appetite for risk, the portfolio will include a range of fixed income asset classes (such as government bonds, investment grade, high yield) and real assets (global real estate, infrastructure, and perhaps commodities). These asset classes diversify risk and help you achieve your investment goals with lower volatility, minimising the ups and downs of the market. However, when looking at each these asset classes individually it is impossible to forecast which one will perform best over shorter time periods such as a year. This is illustrated by the following chart.

Source: IMA. Figures show the median percentage rise or fall of each asset grouping per calendar year. Figures do not include fees or other charges. The effect of these would reduce the figures quoted.

Building a well-constructed portfolio

Diversification is more than just spreading risk. In building portfolios we start by looking at our risk and return assumptions for each asset class, using a 5 to 10 year timeframe which matches the investment horizon of a typical investor. We then look at the interaction between different asset classes, to make sure we combine asset classes in a portfolio which perform in different market environments to provide our clients with effective diversification and the greatest chance of success. Finally we also take into account our shorter term views on how asset classes are most likely to behave over the next 1 to 3 years. Whilst it could mean staying away from a specific asset class, it will generally likely involve overweighting asset classes we like and underweighting asset classes we don’t like.

Russell’s success has been built on a clear investment process that is repeatable. This isn’t about making ‘hero’ calls on the direction of the markets. We belief that every basis point (0.01%) counts and employ strategies designed to improve performance and efficiency, which even if minor individually, make a real difference when aggregated. The British cycling team, headed by Sir David Brailsford, have had great success from an approach based on marginal gains, using the motto “will it make us faster?” for every detail. At Russell, we ask “Will it make our funds perform better?”