Stock market volatility in 2016: reality or rumour?

There was much talk of stock market volatility in 2016 – so where do you think 2016 would rank among the past twenty years, when we compare the daily volatility of market returns?

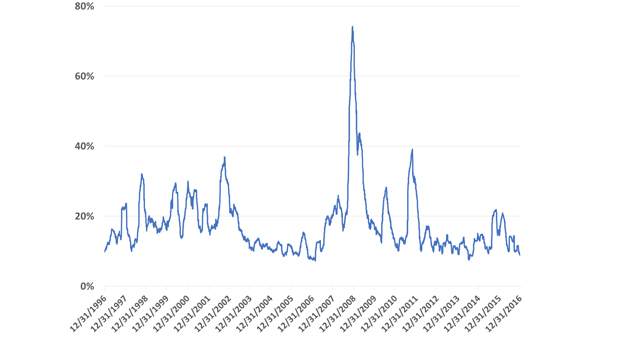

Smoother than the average year

2016 was the 14th most volatile of the past twenty years, as measured by the Russell 3000 equity market index. The annualised volatility of 13.6% was higher than that of 2004-2006 and of 2012-2014, but below that of every other year since 1997. So as roller coasters go, this was a remarkably gentle one.

That result may well come as a surprise to many readers. But it is confirmed by the chart below, which shows the 60-day rolling volatility of the Russell 3000™ index for the past twenty years. Following a period of unusual calm post-2011, there was indeed a jump in volatility that started in the second half of 2015, but that died down over the course of 2016. Compared to the longer term norm, 2016 wasn’t particularly bumpy at all.

Annualised 60-day volatility of stock market returns, 1997-2016

Source: Russell Investments, FTSE-Russell

Can it last?

There are plenty of reasons that the stock market could have turned out more volatile than it did in 2016. The market’s response to the year’s major political surprises was much more muted than most would have anticipated: Brexit provoked a very brief bout of market wobbles, but so far the only lasting impact seems to have been on the value of sterling; Donald Trump’s U.S. election victory stirred up many things, but not the stock market.

Maybe this will continue in 2017, maybe not. It would be brave to assume that there will be no more political turmoil: it’s not only the British who are disgruntled with the European Union, and the cracks in the single currency project are never far from the surface; U.S. relations with key economies, notably China, under a Trump administration are unpredictable, as is the geopolitical outlook in the Middle East. The new administration also likely represents a change of direction in domestic policy. Stock market valuations are stretched by many measures, and interest rates have been making commentators look like fools for what seems like forever. So potential catalysts for renewed volatility are easy to find.

Perhaps it’s little wonder, then, that it feels like the market was more volatile in 2016 than it really was. Our MD of US Fiduciary Solutions wrote in 2014 that “some day in the future, we will look back at these markets as particularly low, not high, volatility. And when we do experience higher volatility, it will feel nothing like it does today”. That “some day” has not arrived yet. But it’s two-and-a-half years closer than it was when those words were written.

1 All of the volatilities quoted in this post are the standard deviation of daily returns over the period in question, multiplied by SQRT (252) to give the annualised equivalent.

2 This conclusion is not simply a side-effect of the choice of volatility measure – it ranks similarly on other measures such as the volatility of monthly returns, or the number of days where the market movement exceeded a threshold such as ±1%.

Bob Collie, Chief Research Strategist, Americas Institutional