Supply chain melody: Will supply chains continue to heal in 2023?

- Once disrupted by pandemic restrictions and lockdowns, supply chains have now demonstrated significant signs of recovery

- As we continue into 2023, supply chains should heal further, though there is always an element of uncertainty in the outlook

The bottom line: Supply chains have played a critical role in explaining some of the inflationary pressures we have seen recently. We believe working with a trusted advisor like Russell Investments can help you better understand this complex song.

Introduction

Market observers often quip “copper has a PhD in economics.” But the graduating class of 2022 has another member – supply chains. After the emergence of the coronavirus, lockdowns and other restrictive measures hampered the normal functioning of supply chains. As we round out 2022, it may be prudent to examine the current state of supply chains, and the implications for 2023.

Transportation costs appear to be normalising

Transportation costs are one way of gauging the state of supply chains. The more that transportation costs rise above their long-term trend, the more likely it is that supply chains are under pressure. Within transportation costs, ocean freight shipping costs are perhaps the most important bellwether. After all, much of international transportation depends on transoceanic freight. For heavy durable goods such as refrigerators, trucks and dishwashers, transporting the goods via ocean freight vessels might be the only practical means of getting the products from the manufacturer to the customer.

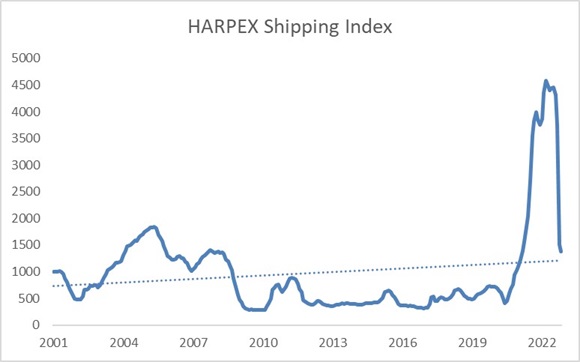

Up first: the HARPEX Shipping Index. Produced by a ship brokerage firm, this index tracks the prices of chartering a container ship. The higher the index value, the more expensive the shipping costs are. Looking at the graph below, we can see that the HARPEX Shipping Index has fallen noticeably from its peaks and is now only slightly above its longer-term trendline. This suggests that container shipping prices have largely normalised.

Source: Refinitiv Datastream, Nov 2022

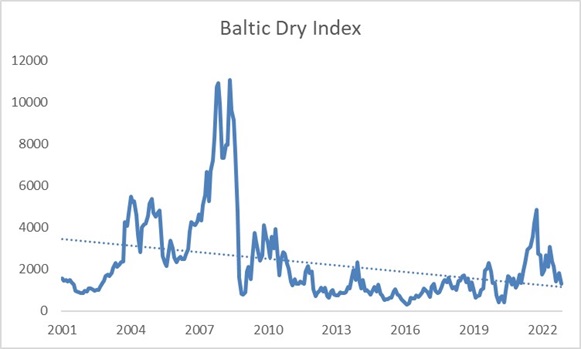

Raw materials also often get transported via transoceanic freight vessels. As such, the Baltic Dry Index, which measures the cost of shipping raw materials, can also be a useful measure of how strained supply chains are. Like the HARPEX Index, the Baltic Dry Index has given back much of its pandemic-induced gains and is now closing in on its longer-term trendline.

Source: Refinitiv Datastream, Nov 2022.

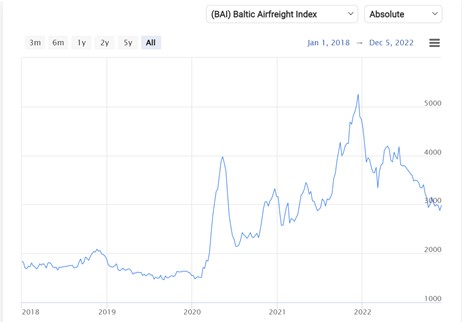

While transoceanic freight vessels play a key role in transporting goods, air freight is often used for perishable products or those that need to be delivered expeditiously. The Baltic Airfreight Index (BAI) tracks prices for transporting cargo by air. Although the Baltic Airfreight Index is still noticeably above pre-pandemic levels, it still is down approximately 40% from its peak, providing yet another sign that supply chains may be healing.

Source: TAC Index, Nov 2022

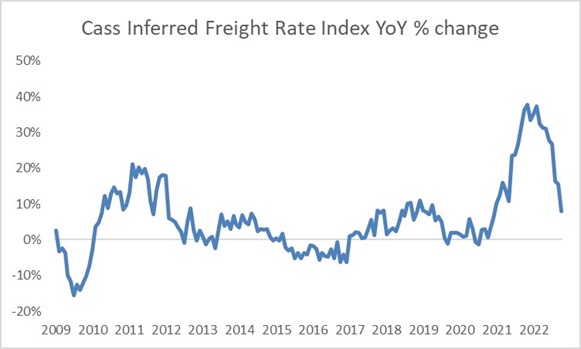

Finally, let’s consider those goods that are shipped purely within North America. The Cass Inferred Freight Rates Index serves as a composite unit price for shipping goods within North America using a variety of methods. Although the year-over-year percentage increase in this index is still positive, we can see that the rate of growth is clearly decelerating – suggesting once again that supply chains are likely healing.

Source: Cass Information Systems, Inc., Oct 2022

Delays and backlogs seem to be clearing

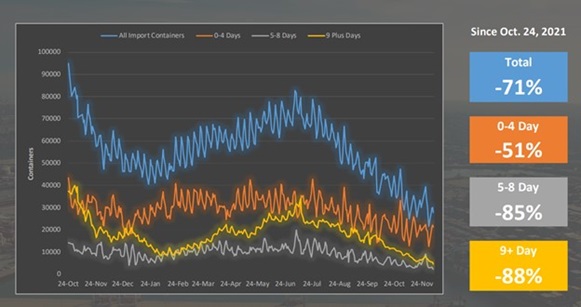

Yet costs are not the only method of examining supply chains. Another critical gauge is how quickly freight shipments can be processed. In 2021, headlines about congestion at the Port of Los Angeles –one of the world’s busiest ports – were common. With the passage of time though, conditions appear to have improved noticeably. The chart below shows trends in dwell times – times in which containers sit idle.

Source: Port of Los Angeles

The volume of containers with the longest dwell times of nine days or more has fallen more than 88% since late October 2021. And news outlets are reporting that the backlog of ships at the Port of Los Angeles has fallen by roughly 90% since the 2021 peak.

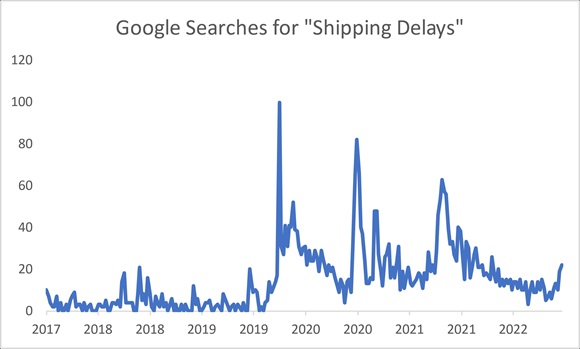

Beyond looking at cargo backlogs, the number of google searches for shipping delays can also be insightful. While it’s not a direct measure of actual shipping times, it’s likely that when supply chains are stressed, shipping delays will be high and lead to more people searching about shipping delays. But from the chart below, you can see that searches for shipping delays are sharply lower than the peaks that we had seen earlier. While it’s true that the searches ticked upwards again in recent weeks, we believe that this may merely be seasonal effects associated with the holiday season. On balance, the google search results once again lends credence to the idea that supply chains may be healing.

Source: Google Trends, 7 Dec 2022

The link between supply chains and inflation

While supply chains might be fascinating for economists to examine, consumers ultimately care about the impact on their lives. 2022 was a painful year for many consumers, as high inflation rates outstripped consumer wage growth, and ate into consumers’ purchasing power. Although there are many factors that influence inflation rates, supply-chain impacts played an important role.

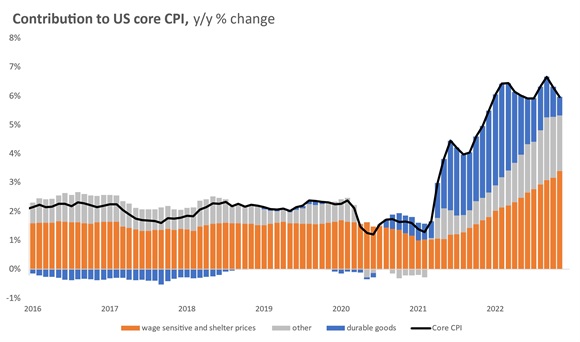

The chart below examines the contribution (in percentage points) to year-over-year core inflation rates. Pre-pandemic advances in technology led to a secular decline in the prices of durable goods. In the chart below, the blue bars show that durable goods prices typically fell-year-over-year and helped keep overall core inflation rates at bay. However, during the course of the pandemic, many countries imposed lockdowns and other mobility restrictions that greatly hampered production and transportation of goods. Those supply-chain disruptions caused the prices of durable goods to actually increase. The blue bars began turning positive, and continued growing until late 2021/early 2022.

The good news for consumers is that this trend seems to be turning again. The blue bars have compressed from their widest points, suggesting that the healing supply chains are causing durable goods price inflation rates to moderate.

Source: Russell Investments’ decomposition using data obtained through Refinitiv Datastream

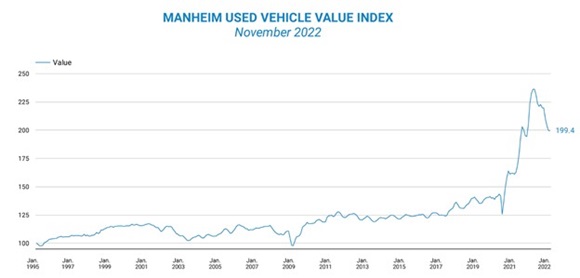

Within durable goods, one of the big drivers of high inflation has been used cars. The chart below shows how dramatically used car prices had spiked in late 2021/early 2022. But in recent months, the prices of used cars have been falling. Although prices are still markedly above pre-pandemic levels, it’s at least comforting to see that price pressures have eased up somewhat.

Source: Manheim Solutions/Cox Automotive

Outlook and risk factors for 2023

With 2022 drawing to a close, it can be tempting to think about what 2023 may look like. While macroeconomic uncertainty can be expected, there are promising signs that supply chains will likely improve further rather than deteriorate. China, one of the biggest industrial hubs globally, has signaled a relaxation of some of the strict COVID control policies that have hampered industrial production. Although there’s a risk that some of these policies may return should COVID cases rise more than expected, we believe that the Chinese government’s renewed focus on economic growth should help make any controls more targeted, rather than repeating some of the city-wide lockdowns that were seen earlier in 2022. If China can produce goods at close to a regular cadence, that should help alleviate some of the supply side pressures.

Economic growth is also expected to moderate in many developed countries in 2023, with the potential for some regions to even experience a mild recession. While recessions are of course painful for consumers, a mild recession can also be the bitter herbal medicine that helps further heal supply chains. In a recessionary environment, consumers are likely to delay big discretionary purchases of things like televisions and cars. The easing of demand will create more balance in the system and help mend the remaining supply chain fragilities.

Energy prices can be a bit of a wildcard that can either help or hurt supply chains. While the reduced demand from a recession might help to dampen energy prices, any escalation in geopolitical conflicts could potentially cause spikes in energy prices, at least in the short-term. A spike in the prices of oil and diesel would likely make it more expensive to ship goods, once again creating supply chain woes.

The supply chain melody can be hard to master, with a significant amount of nuance. But when you work with a trusted advisor like Russell Investments, we believe you will be better prepared to navigate the challenges. That is perhaps the best holiday symphony you can ask for.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.