U.S.-China ceasefire: Reasonable outcome for markets, brief respite for economies

How might the ceasefire on new tariffs between the U.S. and China impact markets and economies?

No new tariffs for three months

At the 2018 G-20 Buenos Aires summit that concluded last weekend in Argentina, U.S. President Donald Trump and Chinese President Xi Jinping agreed not to impose any new tariffs for three months to allow negotiations to continue at the technocrat level. This ceasefire delays the ramp up in the U.S. tariff rate from 10% to 25% that was scheduled for the 1st of January (impacting $200 billion of Chinese imports). The agreement stalls Trump's threat of new tariffs against the final $267 billion of imports from China, at least temporarily. In response, China "will agree to purchase a not yet agreed upon, but very substantial" amount of U.S. exports.1

A positive turn in the trade war

This is a positive turn in the trade war, but it falls close to the consensus expectations from economists. A more positive outcome would have contained substantive details and/or a longer pause (e.g., six months). The three-month ceasefire by no means guarantees that a final trade deal will be struck, but it improves the risk distribution for markets.

Impact on global equities

We view the G-20 meeting as a small tailwind for global equities, with the order of impact being most positive for China and emerging markets (EM) and least positive for the U.S. This ceasefire is probably not long enough to meaningfully reduce uncertainty for the CEOs (chief executive officers) of multinational businesses. Therefore, we expect U.S. (and global) capital expenditure to remain subdued until a lasting agreement is reached.

U.S. perspective

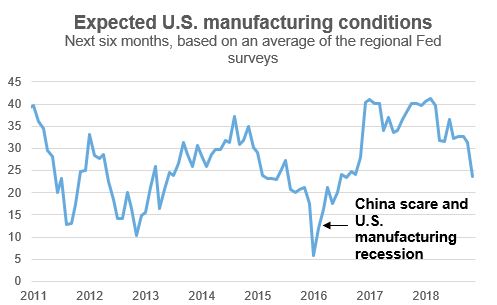

Until very recently, there has been little discernible impact from the trade war onto our high frequency business confidence tracker. In the November regional U.S. Federal Reserve (Fed) surveys, however, we saw a marked step down in the optimism of U.S. manufacturing executives. It's difficult to disentangle how much of this was from lingering trade concerns versus the moderation in global growth rates and the collapse in crude oil prices — but we suspect the latter forces are playing a more significant role.

Where next for stabilisation?

The next Beige Book report from the Fed, scheduled for release on the 5th of December, will give us a cleaner read on the underlying narrative. At present, we expect there to be a stabilisation/rally in oil, a stabilisation/reacceleration in Europe and Japan as well as a stabilisation in China. Given this, we look for our confidence tracker (and other broader indices like the Institute for Supply Management Index — i.e., the ISM Index) to stabilise firmly in the zone consistent with positive above-trend economic growth. The sharpness of the recent dynamic bears a watchful eye, though.

Source: U.S. Federal Reserve System and Russell Investments calculations, as at 30, November 2018.

Implications for U.S. tariffs

The implications of U.S. tariffs are more material to the inflation outlook. The tariffs that have already been implemented ($50 billion at a 25% rate, and $200 billion at a 10% rate) are currently adding roughly 0.1% to core personal consumption expenditures (PCE) inflation. With the 90-day pause for further negotiations, we've pushed back our timeline on the expected inflationary impacts from the higher tariff rate by three months. The bottom line is that the near-term inflationary consequences of protectionism are still potentially very significant, but the pause means they are more likely to show up in mid/late 2019 now (if at all).

Implications for the Fed

The implications for the Fed are mixed. The first order effect is that the ceasefire removes a near-term event risk for the December and March Federal Open Market Committee (FOMC) meetings, making hikes marginally more likely on each of these dates (where we already had high conviction levels). Easier financial conditions, should they emerge, would also be a tailwind for the Fed's ability to deliver on its intended rate hike path. The recent weakness in core PCE inflation, however, coupled with the delay in potential tariff-related inflation boosts, does suggest some potential for a Fed pause scenario in June.

To be clear, this is not our baseline view. As we can see in the chart, the inflationary consequences of tariffs are transitory — meaning the Fed is likely to look through them. Our expectation of continued above-trend U.S. economic and employment growth should continue putting pressure on a very tight U.S. labour market. Furthermore, our team expects an abatement of the downside risks emanating from non-U.S. growth.

China perspective

Impact on Chinese GDP

From a Chinese economy perspective, the Xi/Trump meeting in early December was a touch better than our expectations. In terms of economic implications, there's nothing here to change our expectation of a moderate-risk slowdown in the Chinese economy in 2019, from 6.5% gross domestic product (GDP) growth to 6.0% GDP growth.2 While the uncertainty around such estimates is always high, we believe it's convenient to calibrate and track the China impact of the trade war in terms of GDP impact. The best outcome we see would be a one-off permanent reduction of Chinese real GDP by 0.5%. The worst outcome, from our vantage point, would be a negative GDP hit of 1.5%, which we would associate with a high to very high-risk slowdown. As at today, we anticipate that there will be a 0.75% real GDP hit.

Implications for the trade war

We'd rate the outcome of the weekend's talks as one-part trade war, one-part grandstanding and one-part obfuscation. And maybe even some progress. That's a whole lot better than three parts trade war. Even getting a communique was not necessarily expected. At present, we are overweight China A-shares and will be staying this way for now.

Given that within the U.S., Trump's main objective appears to be seen as reprimanding China, while within China, Xi’s main objective (incompatibly) appears to be seen as standing up to the U.S. and giving no ground — then an unclear meeting outcome that kicks the can down the road and that nobody can understand, is a win for global investors.

All of that said, we'd adhere to a view that the U.S. and China will be oscillating between fake deals and fake unilateral initiatives, through much of 2019. That, in and of itself, makes so called muddle-through scenarios the most likely. These trade negotiations likely still have a long way to go. We'll be watching the Chinese high-frequency economic indicators, and data from exports and the purchasing managers indices (PMIs), for an ongoing read on the impact.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 White House, “Statement from the Press Secretary Regarding the President’s Working Dinner with China” 1 December 2018. Accessed via

2 Russell Investments, 3 December 2018.