Turning lemons into lemonade: How to convert the recent market volatility into a tax-managed opportunity

Editor's note: The chart in this post was updated to include market data through May 18, 2020.

There is no denying that market volatility, especially volatility of the negative kind, can and does make clients as well as investment professionals nervous. Add to that a near constant 24-hour news flow that follows us almost everywhere (just consider that fact that we are attached to our little devices all day long) and many are left wondering, what do I do?

These numbers and stats I am about to share may be of little consolation, but it is important to put things into historical perspective:

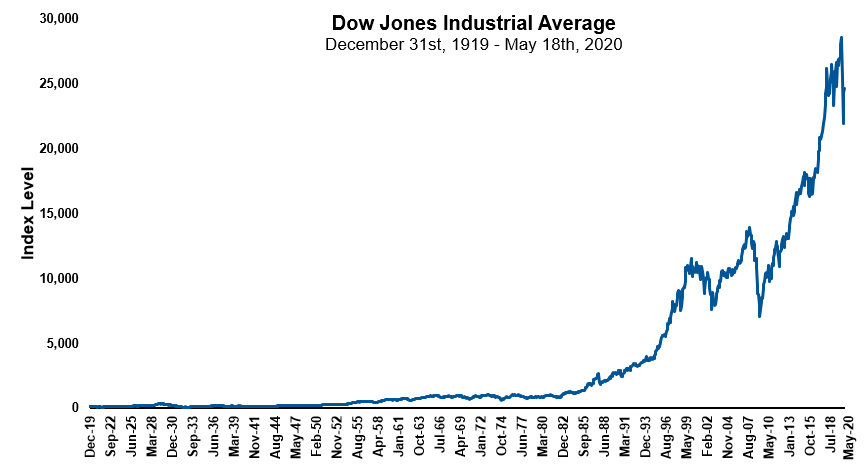

- The Dow Jones Industrial Average (DJIA) finished the year 1919 at a level of 107. Today we are at north of 20,000 (21,201 at the time of my writing this). That is around a 200 times increase in the value of the Dow Index!1

- Put another way: An investment of $10,000 at the start of 1920 in the DJIA would have resulted in a portfolio today worth $2.2 million—without counting dividends! Not shabby.

- U.S. equity markets, on average, are positive three out of four years.

Click image to enlarge

Source: Factset.com

Source: Factset.com

Think through the many things we have seen or experienced as a nation and globe over the last 100 years. There have been many wars, natural disasters including earthquakes, volcanic eruptions and hurricanes, past pandemics, oil and nuclear crises, and financial crises and recessions.Yet here we are today, with long-term value creation, despite periods of volatility.As a point of disclosure: investing in stocks and bonds is not for everyone, and it is important for investors to consult with a financial advisor about what is best for their personal situation.

The tax-management opportunity for investors today

Here are three practical tax-management suggestions and potential actions that can be taken when investors ask, What can I do about this volatility we are experiencing right now?

These are specific to clients that have had tax bills they would rather have not been paying or have investments with embedded gains they would like to transition out of but taking action would result in a tax bill if sold:

- Mutual fund or ETF portfolios

- Separately managed accounts (SMA)

- Concentrated stock positions

Transitioning out of some of these investments and into a tax-managed portfolio that is more suitable for non-qualified accounts makes sense to most, but the trick and challenge is how to do it without getting saddled with a larger-than-expected tax bill in the process.

1. Mutual fund and ETF portfolios

There are two things I think are important to consider with transitioning this type of portfolio: a) the breakdown of embedded gains by tax lots; and b) the actual embedded gain today in total.

What many fund investors often don’t realize is that their actual embedded gain is smaller than they think.The reason for this is the fact that in the vast majority of cases there have been sizable capital gain distributions paid out annually. The end result of these so-called distributions is that investors pay a significant amount of their taxes along the way.This makes the cost of transitioning lower.

Think about this in terms of total tax cost, and tax cost by tax lot.The cost of transitioning could be further reduced by using market volatility and market downturns to lower the tax bill. Think about a 10% drop in the market in a short period of time. With the reality of an already reduced tax bill due to taxes having been paid, the loss harvesting opportunity during a market downturn could reduce or even eliminate an investment portfolio’s tax bill.

We feel this is a great time to take a good look at accounts of clients that have expressed unhappiness at past tax bills (or said differently, screamed bloody murder when they saw how large the check to the IRS was).Consider what can be done to transition them out of those investments and into a tax-managed portfolio that is more suitable for their taxable situation.Instead of a conversation of unease about the markets, a more productive conversation about after-tax wealth growth and tax management can help demonstrate greater valuein front of clients.

2. Separately managed accounts

While SMA portfolios often run into the same challenges as funds when it comes to how do you move without triggering big tax bills?, they do often have a more unique problem.That problem is an actual large embedded gain with little flexibility to make changes when you hit a point referred to as lock-up.Lock-up happens when most losses have been harvested and the portfolio is loaded with positions that have large embedded gains.This situation happens surprisingly often, and after a significant bull market run, clients are now holding onto a portfolio that could be getting stale—and with a large embedded gain and tax bill, that makes moving very difficult.

What can be done about this?Once again, we believe using the market volatility and down movements could be advantageous and open up flexibility with these portfolios. While the markets as a whole have come down, some sectors/industries/stocks have moved down even more.This is a great time to do some analysis on SMA portfolios that may be in your book of business.In some cases, the embedded tax situation may be down to a tolerable point for a client to transition out of the portfolio.Or, there might be loss harvesting opportunities that could help eliminate at least part of the client’s gain position, allowing a partial transition to occur.

3. Concentrated stock positions

The opportunity here is similar in nature to that of what can be done with a SMA portfolio, but in a more focused or possibly more limited manner. That being said, it is worthwhile to see how much of an embedded gain in concentrated positions has decreased with the recent down-market movements. At a minimum, you can discuss with the client and see if a move makes sense. At best, a concentrated position can be moved out of and proceeds transitioned into something that makes longer term tax-sense for the client.

Take action – limited time opportunity

Any which way you look at it, there is an opportunity to help clients improve the after-tax wealth results in their portfolio right now. This is one of those limited-time opportunities to better align taxable investment portfolios by using the market volatility to lower—and even possibly eliminate—a client’s tax bill. Even more importantly, we believe it's also a great time to help clients move toward a tax-managed solution for long term alignment and after-tax growth.

1Source: Factset.com