Tax-loss harvesting: When life gives you lemons, does it matter WHEN you need to make lemonade?

As I approach the big 40 later this year, I’m starting to prioritize things differently. I’m thinking about doing more of what I like (i.e. golf, travel, etc.) and less of what I don’t like (i.e. yard work, mulching, etc.). I also value my time differently. Instead of trying to do things myself as I would have in the past, I’m hiring someone who can focus on the activities I‘m not well-versed in (and that I frankly don’t enjoy) and who is simply better at it than I am. For me, getting to 40 is finally feeling good about letting someone else make the lemonade for you.

In the conversations I’ve had with advisors and clients, tax-management and tax-loss harvesting tend to be the activity equivalent to my yard work—necessary, but not enjoyable.

To paraphrase Elbert Hubbard, “When life gives you lemons (negative markets), make lemonade (tax assets in the form of tax-loss harvesting).”

I want to reiterate the value that tax-management may add. For those of you who have seen me present the 2020 Value of the Advisor study, tax-management is the second largest component of the value you can add as an advisor. This component has also had the largest increase in value since our initial study from 2013. But tax-management is multi-faceted and complicated, whether you’re an individual or an advisor.

Let’s make the complex simple by exploring two questions, one for individuals and one for advisors:

- Individuals – Why isn’t tax-loss harvesting done more often?

- Advisors – Does timing and scale matter for tax-loss harvesting?

Question #1 – Why isn’t tax-loss harvesting done more often?

- They only do it at end of the year because people are busy.

- Most investors don’t wake up every morning and say, I can’t wait to tax-loss harvest my portfolio today. People are busy and we tend to procrastinate.

- When do they tax-loss harvest? Typically, right before year-end.

- How has year-end tax-loss harvesting worked for individuals?

- Since 1926, the U.S. stock market, based on the S&P 500, has been positive 70%+ of the time, looking at calendar years

- Over the past 70 years, based on FactSet data, in terms of monthly returns:

- November has been the best stock market month

- December has been the third-best stock market month

As we all know, markets don’t conveniently go down at the end of the year, which means investors need to be ready to make lemonade any time the market gives you lemons.

- It’s an admission that you’re wrong. Psychologically, it is hard to tax-loss harvest.

- When you tax-loss harvest, you sell your positions that have gone down (obviously, right?). But for many investors, the act of selling means locking in losses and admitting you’ve lost money.

- We don’t like to admit that we’re wrong (just ask my wife), so instead of selling we hold onto our losing positions. We do this in the hope that they'll recover and we’ll be right again.

- This isn’t just a feeling, it’s an established theory known as the disposition effect, which states investors tend to sell assets that have increased in value, while keeping assets that have dropped in value.1

Question #2 – Does timing and scale matter for tax-loss harvesting?

I’m going to start by stating the obvious: advisors don’t only work with one taxable account. The multitudes of accounts an advisor manages translates to every investor having a specific starting point. Each investor’s cost basis is unique to them and the advisor needs to be sensitive to each situation.

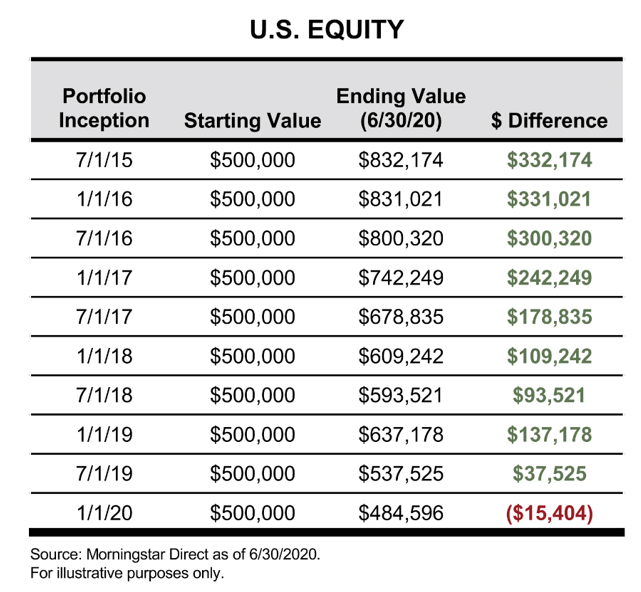

Let’s look at a sample client base by a seasoned advisor in the last five years. For simplicity, let’s assume that this advisor added one taxable account every six months and invested all of the accounts in a hypothetical investment that tracks U.S. equities (S&P 500® Index).

Click image to enlarge

You start to see how complicated and careful one needs to be. Some clients could be tax-loss harvested and others shouldn’t be. This assumes ONLY the last five years, ONLY adding one taxable account every six months, and ONLY invested in U.S. stocks. The larger the client base, the more products, the more complicated this gets.

Does it matter WHEN you make lemonade?

Maybe it’s the approaching 40th birthday, but I feel like today’s market corrections seem to be quicker than they used to be. The most recent bear market started and finished within 30 calendar days, the fastest ever. You need to be ready to act—and to act quickly. As an advisor, you also need to consider which clients get tax-loss harvested first, second, third, etc.

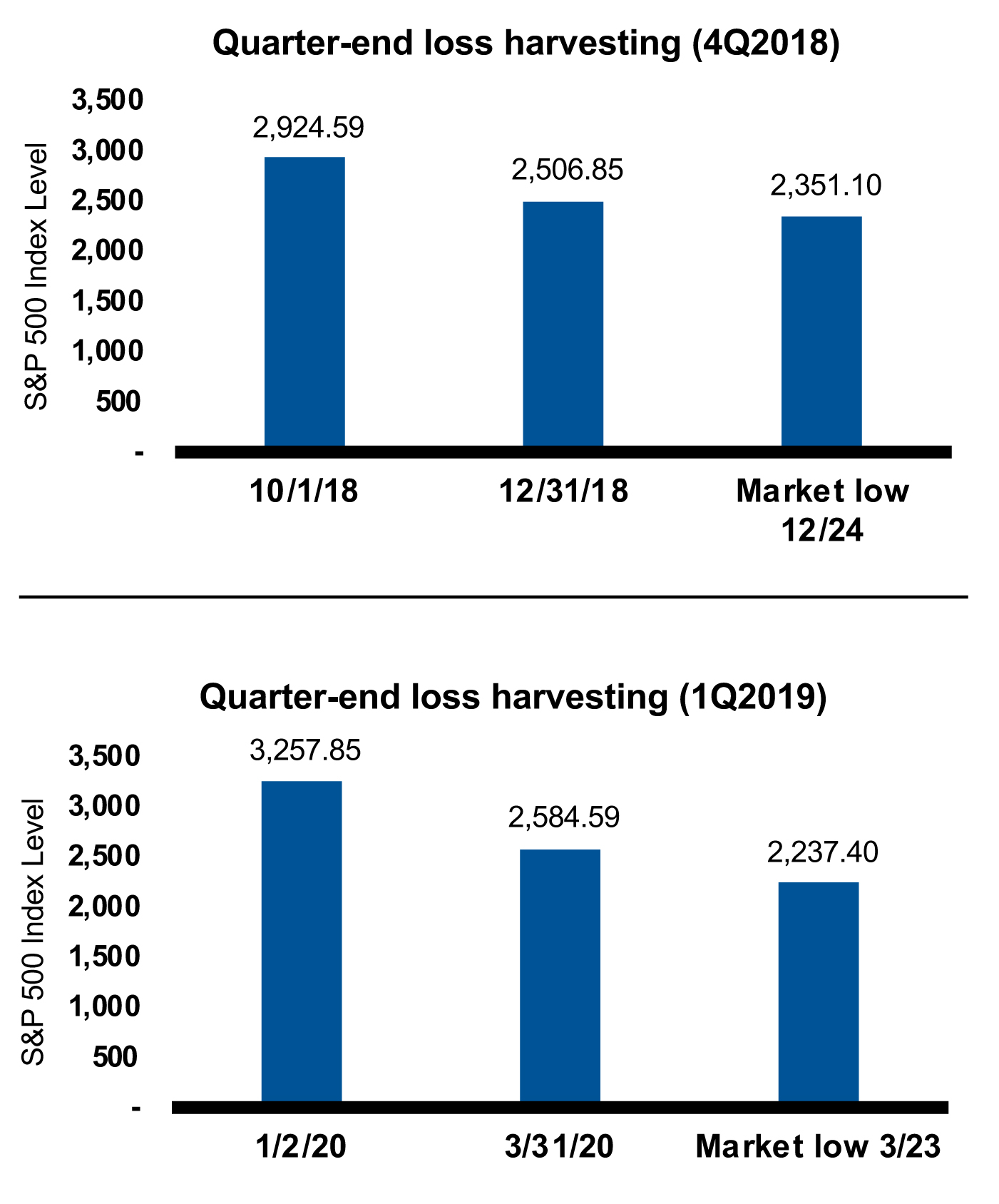

Let’s look at the last two 15%+ market corrections: in the fourth quarter of 2018 and the first quarter of 2020.

Did the timing of when you tax-loss harvested matter? What if you automated tax-loss harvesting with an overlay manager? If you go that route, you’re likely on a monthly or quarterly rotational schedule. Let’s look at two different scenarios:

- Loss harvesting at quarter-end

- Loss harvesting at month-end

1. Quarter-end loss harvesting:

Click image to enlarge

For illustrative purposes only.

Note that in both quarters, the best time to harvest losses (market low) did not coincide with quarter-end dates.

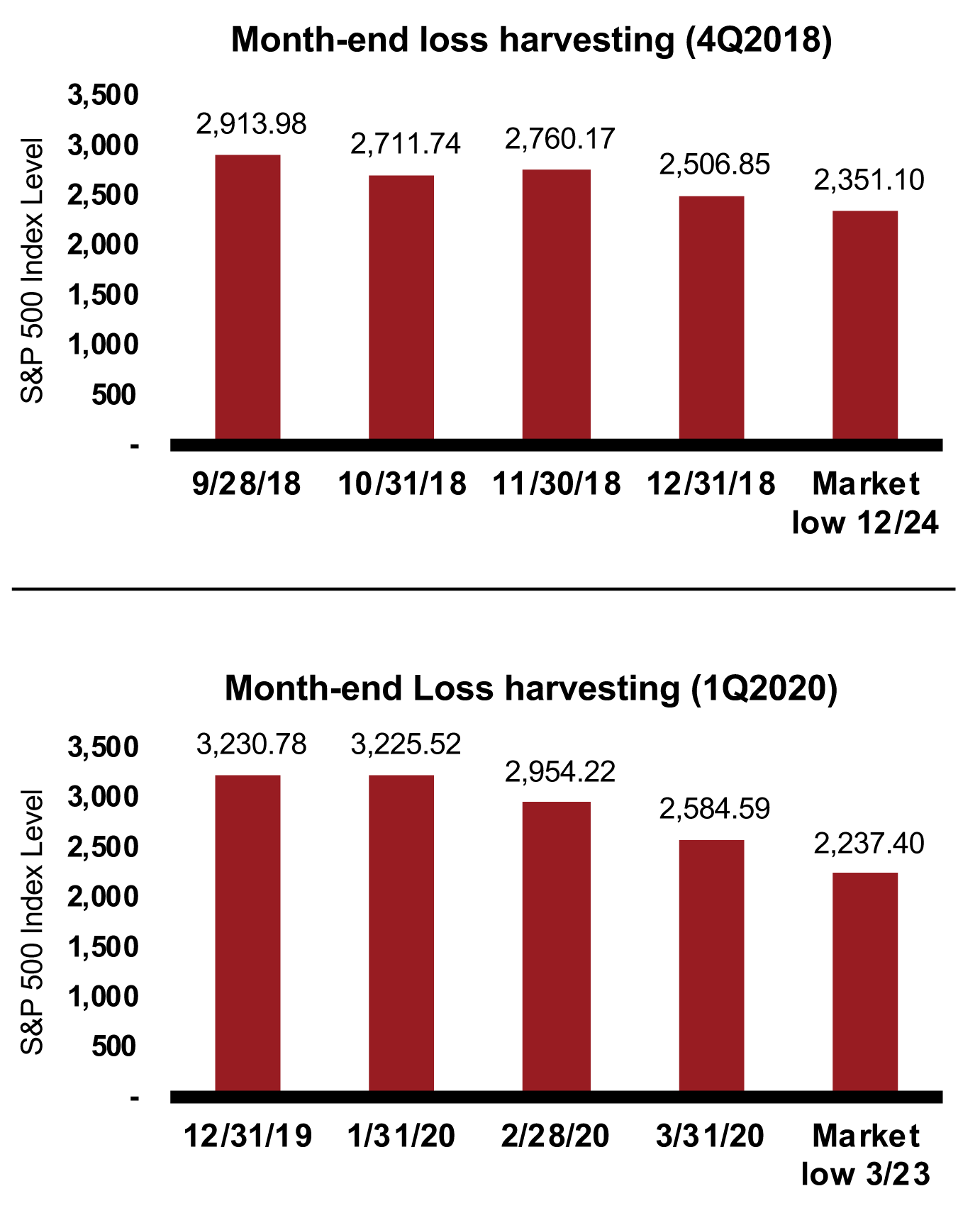

2. Month-end loss harvesting:

Click image to enlarge

For illustrative purposes only.

Note that for month-end dates, again, the best time to harvest losses (market low) was not at the month-end.

These are major differences in what you could have had vs. month-end, quarter-end, or if you’re an individual investor, doing it only once, at year-end. This is the importance of having a systematic tax-loss harvesting program. No one can perfectly time market low points, but given we manage four tax-managed equity funds and two tax-exempt bond funds, we can be laser-focused on seeking the optimal after-tax returns for investors all over the United States. And in the example above, it goes without saying that few were prepared to harvest losses on Christmas Eve. At Russell Investments, we’re ready to tax-loss harvest at any point in the market year—regardless of schedules and we do. Timing does matter and having the scale to implement this across all of our tax-managed strategies is very important.

The bottom line

As we all get older, whether you’re an advisor or an individual investor, we are all experiencing the same things in business and in life. Here are some key takeaways:

- Focus on what you like, and outsource the dislikes to someone that can focus on solving your problem

- No one likes to admit they're wrong

- When tax-loss harvesting, timing truly does matter

- Partner with someone that can help you scale tax-management across your business

If you already partner with Russell Investments for our tax-managed solutions, thank you for your partnership. If you haven’t yet considered us, think of this as your lemon. Now let’s go out and make some lemonade.

Related articles

Grasp the opportunity: Tax-loss harvest your legacy mutual fund portfolio

Be opportunistic: Tips on transitioning to tax-managed investing from a legacy mutual fund portfolio

Your words matter! Especially when it comes to TAXES.

1 Shefrin, Hersh; Statman, Meir (July 1985). "The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence". The Journal of Finance. 40 (3): 777–790. https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1540-6261.1985.tb05002.x