Your words matter! Especially when it comes to TAXES.

This is a milestone kind of year for me, so forgive me if I’m starting to get a little nostalgic. My triplets are going into middle school next year, my wife and I have been married for 15+ years, and I’m just finishing up my 15th year at Russell Investments, which converts to 50 years in wholesaler years. Whether it’s communicating with my kids, my wife or advisors and their clients, a few things ring true to me—our words matter, and expectations are everything.

Let’s play this out. Russell Investments has also crossed an important milestone with our Tax-Managed Model Strategies. We now have a 15+ year track record to talk about. One thing is very apparent: taxes are hard and the differences between approaches vary wildly.

Common approaches observed for non-qualified (taxable) accounts

Below are the most common approaches I see day after day in non-qualified accounts:

- Individual Retirement Account (IRA) is managed the exact same way as the non-IRA.

- Everything is the exact same. I’m not sure what adjective we’d even use to describe that, but it happens way more than people think.

- IRA is managed one way, and the non-IRA uses municipal bonds for fixed income.

- All of the equity exposure is managed the exact same way from IRA to non-IRA

- A balanced investor may be thereby ignoring 60% of the tax problem by going with the exact same funds in IRA and non- IRA

- IRA is managed one way, and the non-IRA uses a total passive approach using ETFs or index funds.

- The asset allocation and the weights to the different products are the exact same from IRA to non-IRA

- IRA is managed one way, and the non-IRA is totally different.

- This approach uses a different asset allocation, different funds, different managers and different techniques all geared towards pursuing a better after-tax outcome (more on this—and my favorite—approach later).

So, what’s the difference?

During my travels throughout the year, I see three different adjectives that describe the different approaches to non-qualified accounts that I outlined above: tax-aware, tax-efficient, and tax-managed.

Remember when I said that words matter? Here’s a great example of how widely these approaches differ by definition:

- AWARE – Having knowledge or perception of a situation or fact

- EFFICIENT – Working in a well-organized and competent way

- MANAGE – Succeed in surviving or in attaining one's aims

Why does it matter? Because a tax-managed approach strives for a better after-tax outcome

Let’s take this down to a personal level that everyone can understand: through the lens of academic grades.One of the goals for our triplets is for them to get As and Bs.Many of you probably have done something similar with your kids.Now, let’s relate this to the different approaches we often see with non-qualified portfolios.

- If my oldest triplet daughter Addison is getting a C in math, she will be AWARE (knowledge or perception of a situation or fact)—as will I—but being aware of something doesn’t imply action to do anything about it. How does this apply to non-qualified accounts?

- Consider scenario #2 above. The non-IRA uses municipal bond funds for the fixed income weighting, but all the equity weights are the exact same between the IRA and non-IRA. We think we can do better.

- If my middle triplet Emily is getting a B in science, not only is she AWARE of her grade—and again, so are we—but she’ll say to me, Dad, a B is pretty good, and I already understand Science really well. I feel like I’m being EFFICIENT in my work in science class, so I can study other things that are harder for me. I’m working in a well-organized and competent way. BUT, she’s not applying herself or trying to manage to the best outcome, which would be an A in science class.

- Consider scenario #3 above. The non-IRA is using inherently efficient ETFs/index funds. Awareness is one thing, being inherently efficient is another, but the next step is managing to taxes—that’s a completely different ballgame. We think we can do better.

- If my youngest triplet Hailey is getting an A in English class, she is managing her course load while setting a high bar for herself. As parents, we’ve set that goal or outcome for our kids.Then, when they MANAGE all of the things thrown at them, they can then succeed in attaining their outcomes. That is the definition of manage.

- Consider scenario #4 above. Managing implies action, not just one time, but consistent action to sustain the desired outcome. There is a big difference between being competent (part of the definition for being efficient) and being successful (part of the definition of manage).

MANAGING for taxes and the difference it can make for investors

Consider the following two scenarios addressing individuals and advisors and the MANAGE aspect of non-IRA accounts:

- Most (if not all) individual investors wait until post-Thanksgiving at year-end to engage in their tax-loss harvesting exercises on their non-IRA accounts … more on this in the chart below.

- Many advisors find it hard to scale their loss-harvesting activities across hundreds of different non-IRA accounts within their entire book of business. It becomes increasingly challenging as each advisor's client establishes his or her own cost basis when they invest.

If we can agree that a HUGE part of the MANAGE phase within a non-IRA account is tax-loss harvesting, why do we wait to do tax-loss harvesting until year-end?

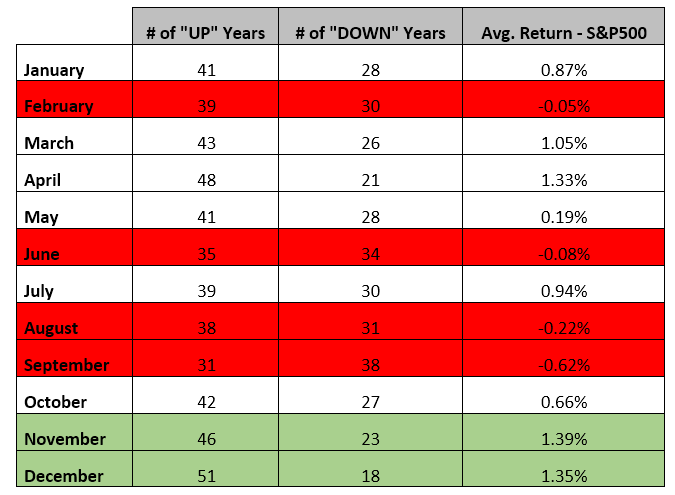

Indeed, the IRS does allow tax-loss harvesting to happen in any of the 12 months of the calendar year.How has year-end tax-loss harvesting worked out over the last 68 years? The chart below outlines the average monthly return as well as the number of up market months and down market months in the S&P 500 since 1950.

Chart: Monthly S&P 500 Returns (1950 to 2018)

(http://www.moneychimp.com/features/monthly_returns.htm)

Click image to enlarge

Note: Past performance is no guarantee of future results.

It’s ironic that individual investors are looking for loss-harvesting at year-end, which over the last 68 years has been the worst time to be looking for losses, as the months of November and December are typically the two of the best market months in terms of market returns.

When should we be looking for losses instead?Ideally, in the months where the market is down … but, if you’re like my family, this is the last thing we’re doing in February, June, August and September:

- What we’re actually thinking about instead of loss-harvesting portfolios:

- February – how to get out of the frozen tundra of Wisconsin

- June and August – where should we go on our summer family vacation

- September – what do we need to do to get ready for school again

So, what’s your PROCESS for MANAGING non-IRA accounts?

When you partner with Russell Investments for non-IRA accounts, you’re employing a time-tested process that is so much more than just tax-loss harvesting at year-end. We believe in managing with purpose.

Our trading desk is staffed 24 hours a day by traders averaging more than 15 years of experience across the investment spectrum.Our team is systematically looking for loss positions 12 months out of the year to offset taxable gains.

Remember: Words matter when it comes to taxes

The next time you’re dealing with a non-IRA account, look at the word choice.By partnering with Russell Investments and our tax-managed approach, you know that we are singularly focused on maximizing the investor’s after-tax return.When you manage to a certain expectation, you are looking to drive better results using ALL the investment capabilities.It’s not what you make, it’s what you keep. Let us find a way to help you keep more.

Related articles:

Tax-managed investing 101: Understand the basics and slay the beast