Be opportunistic: Tips on transitioning to tax-managed investing from a legacy mutual fund portfolio

With markets experiencing a lot of volatility lately (might be slightly understating that), and many of us experiencing work as well as daily-life scheduling changes of an unprecedented magnitude, it’s important to find the bright spots or even ways one might be able to take advantage of this time.

I recently wrote a blog on how to take advantage of this wild market ride we are on, specifically aimed at taxable accounts (non-qualified accounts in industry parlance). It’s important to think through investment decisions in a grounded, forward-looking manner.Long-term investing has a demonstrated track record of success, while short-term volatility tends to be just that … short term.So, to ask the question out loud, How specifically can an investor today potentially benefit from this volatility and market downturn?

Here are some pro tips specifically focused on how to think about transitioning out of a legacy mutual fund portfolio in order to invest in a tax-managed portfolio.Tax management is important in taxable accounts as the tax cost (tax bite, tax bill, tax drag … no matter the phrasing, it’s money that leaves your account and stops working for you) is significant and has a much more pronounced impact when a market downturn hits.

Transitioning from a legacy mutual fund portfolio

I will start by saying … we think you might be able to transition right now with no tax impact!

Did that grab your attention? Well, it's most likely true.If you held an average U.S. equity mutual fund for the last three years or for the last five years, there is a very good chance that you can transition today (sell out of these holdings is what we mean by transition) with no taxes due resulting from the transaction.In fact, there is a good chance that in addition to not having taxes due, the investor can mostly bank a tax-loss carryforward to be used in the future.

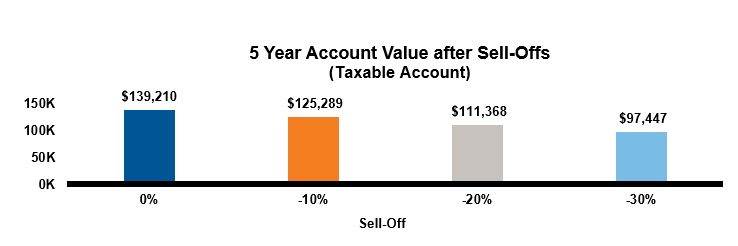

Specifically, $100,000 invested five years ago in a taxable account could now be worth $111,368. This is if you assume a 20% market/account decline.If you assume a 30% market/account decline, then this same account invested five years ago is now worth $97,447. How? Follow along with the math in Table 1 below.Keep in mind, the assumptions are using the average U.S. equity actively managed mutual fund pre- and after-tax returns.

Click image to enlarge

Note: This is a hypothetical illustration and not meant to represent an actual investment strategy.

Example of three hypothetical mutual fund portfolios

What you are looking at in Table 1 is the growth of three different hypothetical values (i.e. three different investor portfolios) using actual mutual fund total returns, pre- and after tax.

An investor with $100K after three years grew their portfolio to $141,474 before taxes,but got to keep $131,365 after taxes—$10k in taxes paid and compounding lost over three years.For the investor with $1 million as a starting point, their portfolio grew to $1,414,735 before taxes, but was left with $1,313,652—that’s over $100,000 in wealth lost to taxes and the compounding impact!

Click image to enlarge

Note: This is a hypothetical illustration and not meant to represent an actual investment strategy.

Source: Morningstar; returns are through 12/31/19. The Morningstar US Category Group “US Equity” includes the following Morningstar Categories: US Fund Large Blend, US Fund Large Value, US Fund Large Growth, US Fund Mid-Cap Blend, US Fund Mid-Cap Value, US Fund Mid-Cap Growth, US Fund Small Blend, US Fund Small Value, US Fund Small Growth.

Here’s how you can use market volatility to potentially lower a client’s tax bill

Assuming these investors are like most people, people like you and me, they don’t like paying taxes.And these numbers are not just staggeringly high, they are negative wealth creation.What can you do right now, especially if you don’t want to get stuck with a really high additional tax bill?Check out Table 2 and its corresponding graphs to see what can be done with market volatility:

Click image to enlarge

Note: This is a hypothetical illustration and not meant to represent an actual investment strategy.

This shows how different market moves can change the embedded gain situation of a portfolio, such as the examples I discussed above.Let’s take a look at the 3-year portfolio example. With what has already been paid out and the compounding impact of taxes due, with a -10% market move the total embedded gain is now reduced to $18,000 on the $100k portfolio.The payback period on making up that tax bill is actually not that high.Even assuming the highest marginal tax rate of 23.8% on the remaining $18k gains, that works out to be a tax bill of about $4,300.For most people that is doable to transition out of this account and into a tax-managed portfolio.

What about with a more extreme market move, let’s say one of -30%? Outside of the shock factor of such a market move, let’s think about how to be opportunistic here—in a way that potentially reduces the investor’s tax bill.That same $100k portfolio invested over the last three years now has an embedded loss in it, which means it's time to think about two things.First, transition now as the situation doesn’t get better than this for lowering a tax bill.Second, the investor can actually harvest a tax loss for themselves to use in the future.This is how you make lemonade out of lemons. And for that $1 million portfolio, well, this just makes the benefit potentially exponential for that investor.

Minimum first step: Redirect automatic reinvestment

At a minimum, it’s important to take a step.A first step, if the client is not ready to do a full-on switch.That first step is to turn off automatic reinvestment.Most investors have it turned on, which means that all their dividends, interest and capital gain distributions are reinvested.All three of these items get taxed in the year they are received; that money and those proceeds are now free and clear of taxes.Use these to start funding a tax-managed portfolio at a minimum.Take the first step if a full transition can’t happen right now.

Act now: Opportunities don’t last forever

We believe this is the time to take advantage of scenarios like the above, as this puts financial advisors and investors in a better position to address long-time tax problems with their portfolios.Use the above examples to think about the portfolios your clients have and what their tax bills have been.Plan through, prepare to act upon and then commit to taking the action steps necessary to first, be opportunistic today, and second, seek to place the client in a much more advantageous position after-tax, by transitioning to tax-managed investing.