How does a tax-managed mutual fund work?

Executive Summary:

- Tax-managed mutual funds have become popular because they help minimize an investor’s tax burden

- They use a variety of strategies to minimize taxable transactions

- Tax-managed mutual funds aim to pay little to no capital gains

Everybody loves a bargain. Buy one, get one free. The diner’s daily special. Your favorite clothing store holding a sale. Most of us jump at the chance to save money.

Our desire to keep more of our money in our own hands is one reason why tax-managed mutual funds have become so popular and are likely to become even more popular. Amid volatile markets, rising inflation, higher taxes and other issues that are nipping at our portfolios and pocketbooks, we all look for ways to keep more of our money working for us. Tax-managed mutual funds can help us do that.

Tax-managed mutual funds are designed to minimize embedded year-end capital gain distributions. These distributions trigger capital gains taxes which can impact the value of a taxable portfolio.

The objective of a tax-managed mutual fund is to generate returns via price increases, while avoiding annual capital gain distributions. Their investment objectives are generally to provide returns similar to non-tax managed funds, but tax-managed mutual funds also have an obligation to minimize taxable transactions within the fund itself. They do this in several ways, whether by selling some stocks at a loss to offset other gains, eliminating wash sales, scrutinizing tax lots, evaluating dividend-paying stocks, or by holding on to stocks rather than selling.

When a mutual fund is labeled as tax-managed, what does it mean?

When a mutual fund has words alluding to “tax-managed” or “tax-efficient” in its name, it is reasonable to expect that fund to have dual investment objectives, one of them being to minimize its investors’ tax burden. Most investment objectives found within the prospectus of equity mutual funds are “to provide long-term capital growth” or “long-term capital growth and current income”. Tax-managed mutual funds will generally include “on an after-tax basis” or “a tax-efficient investment return” within the language of their stated investment objectives.

While it is true that index mutual funds and exchange-traded funds (ETFs) are more tax efficient than traditional mutual funds, that is simply a byproduct of their construction and function. Many index funds have fairly low turnover and tend not to pay out distributions, but that's not always the case. Sometimes stocks get booted out of indexes with market-cap constraints or factor tilts when they no longer meet the indexes' criteria for inclusion. ETFs can tend to be more tax-efficient because of their ability to exchange securities in-kind rather than sell their holdings. However, certain types of ETFs are more likely to make distributions, such as actively managed ETFs or currency-hedged ETFs that employ derivatives contracts.

These types of investment vehicles do not have an explicit obligation to minimize their investors’ tax burden and generally do not carry the label of “tax-managed” in their names.

How does a tax-managed mutual fund work?

Tax-managed mutual funds work in the same way that traditional mutual funds do regarding their portfolio managers buying and selling securities with the intention of providing a return to their shareholders. Both a traditional and a tax-managed mutual fund could have the same general objective to outperform the S&P 500 Index, for example, and ultimately own a similar combination of stocks to achieve that goal. The key difference is that a tax-managed mutual fund takes proactive measures to minimize taxable transactions within the fund (i.e., buying and selling of securities).

In the case of a traditional mutual fund, let’s say its portfolio manager (PM) wants to take some profit from one of its investments, and reduce the position of that asset in the fund by 50%. A traditional PM may simply sell half the shares the fund owns in that stock and call it a day. In contrast, the PM in a tax-managed mutual fund will analyze the fund’s history of purchasing that stock over the years, and specifically sell the tax lots with the highest cost basis. From a record-keeping perspective, the shares with the highest cost basis will have smaller realized gains, and thus produce smaller capital gain distributions.

Another example of how a tax-managed mutual fund works differently than a traditional mutual fund is by proactively harvesting capital losses. Tax-managed mutual funds employ the same strategy as individuals who sell investments in their taxable investment accounts to harvest losses. Whether it is the result of a significant market downturn or via the process of periodically reviewing tax lots, PMs in tax-managed mutual funds can often identify positions with unrealized losses. Although the PM may have conviction in a stock trading below its original purchase price, they may sell it to realize the loss. If the PM maintains conviction in that security, they can buy it back 31 days later to avoid the wash sale rule, lock in the loss, and ultimately own the desired investment for the long haul. Traditional mutual funds cannot prioritize such tax-loss harvesting strategies with investments they intend to own for an extended period.

These are two examples from a set of ground rules that tax-managed mutual funds follow before ultimately making their buy and sell decisions. Implementing these additional parameters of tax-sensitive trading guidelines is a key distinction in how tax-managed mutual funds work differently than their traditional counterparts.

How do tax-managed mutual funds help investors lower their tax bill?

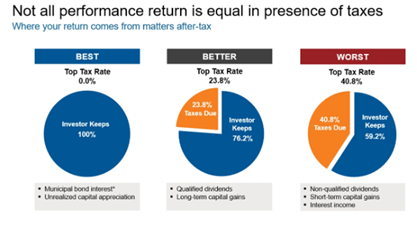

As we know, most traditional mutual funds distribute capital gains based on the trading activity that took place within the fund during any given year. When an investor receives their Form 1099-DIV for the taxable account that holds such funds, that distribution amount will be found in box 2a of the 1099 form. That dollar amount will be taxed at the corresponding capital gains tax rate, which can be as high as 23.8% (when including the NIIT*). That is money the shareholder must pay in taxes because of capital gain distributions, even if those distributions are reinvested back into the fund.

Tax-managed mutual funds aim to pay zero capital gain distributions and subsequently produce a “$0” in box 2a of the shareholder’s 1099 form. Since the shareholder will report $0 in capital gain distributions, there are no capital gain taxes to be paid.

Additionally, tax-managed funds attempt to minimize dividend income, which comes with a tax liability as well. Simply put, a lower amount of dividend income results in lower taxes due. Tax-managed funds go a step further, however, by trying to ensure that the income they do produce is in the form of qualified dividends. Qualified dividends are taxed at more favorable rates than non-qualified dividends.

A shareholder’s 1099 form will show ordinary dividends, which consist of both qualified and non-qualified dividends in box 1a, and qualified dividends in box 1b. The objective of a tax-managed mutual fund is to make sure box 1a and box 1b are the same dollar amount, and thus, taxing all dividend income at the lower, qualified dividend tax rate.

Click image to enlarge

Applies to federal taxes only. Source: Internal Revenue Service. Tax rates as reported by Internal Revenue Service as of 2022.

*Generally for municipal bonds, only interest from bonds issued within the state is exempt from that state's income taxes. Municipal bond interest income may impact taxation of Social Security benefits.

How do you judge tax efficiency?

Tax-managed funds don't guarantee tax elimination, but many employ strategies that can allow investors to minimize their tax burden and maximize their after-tax return. Common steps investors can take to research a mutual fund’s tax-efficiency are visiting its website to obtain historical distribution information, see if the fund has capital gain estimates, or if it may be carrying embedded losses. Morningstar also discloses the tax-cost ratios of all mutual funds, which measure how much a fund’s annualized return is reduced by the taxes shareholders pay on distributions. If you want to compare the tax-cost ratios of different funds, check out our Tax Impact comparison tool.

If you are selecting funds for your taxable clients, take the time to research any prospective mutual fund’s tax-managed strategy. Assess whether you believe it could successfully manage tax drag even in the worst of circumstances. Even when it is faced with sizable outflows, or a management overhaul? Of course, that's not to say you should simply recommend a fund because of its ability to minimize distributions. It will always be important to consider metrics such as a fund's management, strategy, record, and fees. However, neglecting to properly plan for the tax impacts that occur throughout the year can be very costly to your clients come tax season.

*Net Investment Income Tax