Capital Gain Taxes: An easy way to understand the impact they can have

Let’s be honest—taxes are complicated. Trying to make sense of it all can be quite frustrating for many investors. Whether it’s the forms you need to fill out, the information you need to gather to fill in those forms, the many different tax rates that exist, what actions trigger different tax rates … it’s almost as if you need a master’s degree in tax policy just to understand how to pay your taxes.

Regardless, we all need to understand how taxes work. Because taxes have an impact on our income, our wealth, our lives and our ability to have a comfortable retirement. And even more than understanding taxes, we need to know what to do about them.

Taxes on investments: Fees of no value

For many people, their investment portfolio will be the primary source of income in retirement. When it comes to the taxable part of the investment portfolio (often referred to as non-qualified accounts) what is the impact of taxes on this key source of retirement income?

Let’s take a look at how taxes play out and the impact they can have on investment outcomes. The focus here will be on capital gains distributions. These are annual distributions that come out of many mutual funds. While many investors think of them as a dividend, they are actually a return of capital. Investors often do not understand the deep impact these distributions can have on their long-term wealth.

The impact of capital gains distributions

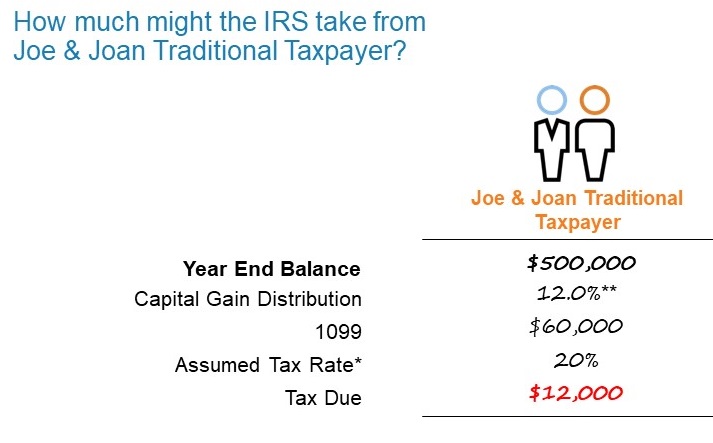

We’ll start by looking at the experience of a traditional investor couple. Let’s call them Joe and Joan Taxpayer. At the end of 2021, they have a balance of $500,000 in their taxable accounts.

The average capital gains distribution in 2021 was quite high at 12%. This number by itself doesn’t mean much to most people; but when you do the math, that results in a $60,000 taxable distribution on Joe and Joan’s Form1099-DIV as shown in our hypothetical illustration below. This is the number that they are going to have to pay capital gains taxes on.

For the sake of simplicity, let’s use a 20% tax rate in this example. This is the top long-term capital gains tax rate at the federal level (excluding the 3.8% investment tax surcharge).

Let’s add it up: 20% of a $60,000 distribution means that Joe and Joan Traditional Taxpayer will receive a $12,000 tax bill. This is not a small amount!

A hypothetical illustration.

*20%: Represent top long term cap gains rate, excluding 3.8% Net Investment Income Tax

**12%: Represents 2021 average capital gain distribution % of Morningstar broad category ‘U.S. Equity’ which includes mutual funds and ETFs.

Active Tax Management: A better outcome

Is there a better way?

Yes, there is, by focusing on active tax management. By using a more hands-on and intensive approach to managing taxes and minimizing capital gain distributions, a better result may be achieved.

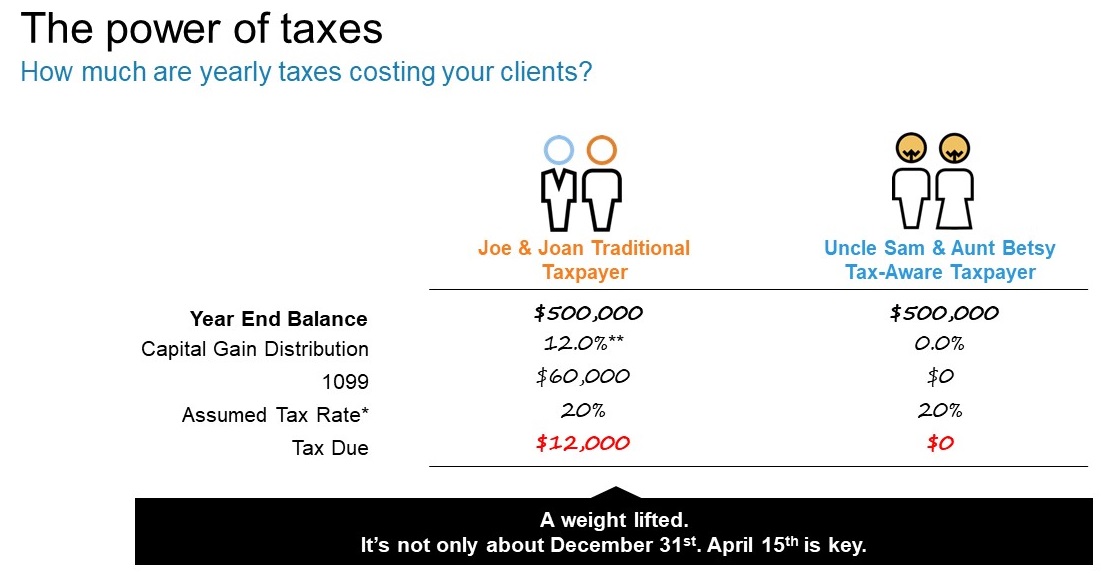

Let’s look at another example using a different couple – Uncle Sam and Aunt Betsy Tax-Aware Taxpayer. For comparison’s sake, we will use the same year-end $500,000 balance.

While the traditional investor last year experienced that relatively high 12% capital gain distribution mentioned earlier, an investor’s portfolio taking full advantage of active tax-managed solutions could have very well had a 0% distribution. A distribution of 0% means their money stays right where they intended—in their portfolio!

Let’s keep working through the math and still assume that same 20% tax rate. When you get to calculating the final figure, remember what we learned back in elementary school about multiplying anything times a zero—the answer is zero. That’s the tax bill for Uncle Sam and Aunt Betsy.

A zero tax bill—that is music to my ears!

A hypothetical illustration.

*20%: Represent top long term cap gains rate, excluding 3.8% Net Investment Income Tax

**12%: Represents 2021 average capital gain distribution % of Morningstar broad category ‘U.S. Equity’ which includes mutual funds and ETFs.

Adding it up

Let’s look at these two examples now side by side.

Look at the difference in these tax bills.

Which one of these two tax bills do you think your clients would rather pay?

A hypothetical illustration.

*20%: Represent top long term cap gains rate, excluding 3.8% Net Investment Income Tax

**12%: Represents 2021 average capital gain distribution % of Morningstar broad category ‘U.S. Equity’ which includes mutual funds and ETFs.

A Form 1099-DIV can be a valuable tool to diagnose the tax efficiency of your clients’ investments. Form 1099-DIV is one of many Internal Revenue Service (IRS) forms and is used to record investment-related income. The Russell Investments 1099 Guide helps you determine what to look for along with insights, implications and actions that can be taken to improve the tax efficiency of an investment. This could help your clients reduce their tax burden and potentially join the ranks of Uncle Sam and Aunt Betsy Tax-Aware Taxpayer.

The bottom line

While taxes may by complicated and confusing, they are important. The thing is, you don’t need to be an expert in taxes to address the problem they create for your clients.

An active tax-managed investing approach can lead to a much better after-tax outcome. Tax drag is not only a burden that weighs on returns over time, but also an indicator that portfolios are not deploying proper solutions. Russell Investments can help shine the light on both the problem as well as the solution.

We’re not only leaders in active tax management, we’re also pioneers, having spent the past 35 years sharpening an approach tailored to remove complexity, solve problems and save time. Tax management is our specialty, and we are here to serve advisors looking to unlock true return by helping their tax-sensitive clients keep more of what they earn.