Taxes: More benefits of kicking the can down the road

As we discussed last year, there are definite benefits for investors to defer recognizing capital gains into future years. Why? The ability to defer the recognition of gains consistently and thoughtfully can lead to improved after-tax outcomes for investors. However, beyond improved returns, there are additional benefits to deferring taxes, including greater optionality and control of one’s investment portfolio. Throughout this blog, we will discuss the various potential benefits of kicking the can down the road.

Tax treatment: Long-term vs. short-term capital gains

One of the most simple benefits of delaying gains for as long as possible is the significant difference in the tax rates related to long-term vs. short-term capital gain realization. A realized gain on an investment held for one year or less is a short-term capital gain, while a gain on an investment held for more than one year is considered long-term. Under current law, short-term capital gains are treated as ordinary income with a top tax rate of 40.8% (37.0% plus 3.8% net investment income tax (NIIT)). Long-term gains receive beneficial tax treatment through a lower top rate of just 23.8% (including the NIIT). With the tax on short-term rates nearly double the long-term rate, it is clearly advantageous to try to defer the recognition of capital gains for more than a year. The current tax debate has long-term capital gains tax rates and thresholds in its crosshairs. Regardless, kicking the can will likely still be beneficial.

Possibly recognizing gains when in a lower tax bracket

Considering many (not all) individuals will have lower taxable income in retirement than in their working years, deferring capital gain recognition until when one may be in a lower tax bracket can be beneficial. Consider the incremental NIIT of 3.8% that applies above a specific modified adjusted gross income (MAGI). For the married filing jointly filing status, this threshold is $250,000. Additionally, the long-term capital gains rate is 0% when taxable income is less than $80,800. Proper planning in later years, including keeping thresholds like these in mind, can provide investors with greater flexibility on which bracket they will fall into in order to reduce—or possibly eliminate—the amount of tax on recognized gains. Kicking the can down the road for the timing of capital gain recognition plus thoughtful tax bracket awareness can materially improve after-tax outcomes.

Gifting assets to individuals

Providing monetary gifts to children or grandchildren is something many individuals desire to do during their lifetime. However, those with highly appreciated assets may find it more tax advantageous to directly gift the assets instead of providing cash. When gifting shares to an individual, the recipient inherits the same cost basis of the position, meaning the unrealized gain does not go away. However, if the recipient is in a lower tax bracket when the shares are sold, this could result in less tax paid on the gains than if the original owner sold the shares themselves and provided the gift in cash.

Donating assets to charity

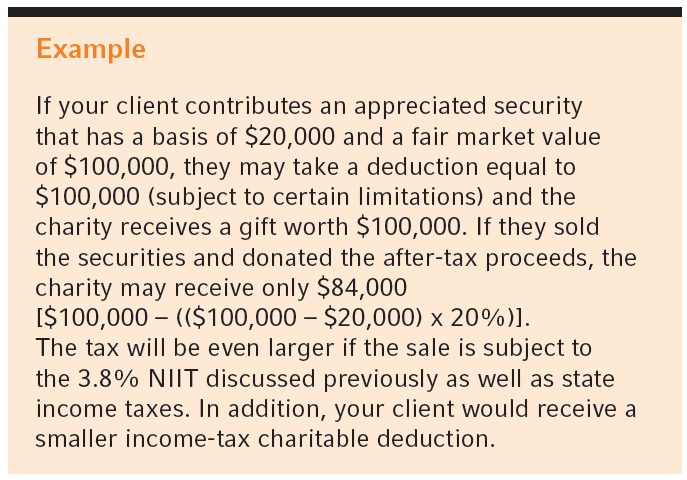

Charitable giving is another topic that is often included in an individual’s financial plan. Like when gifting to an individual, investors who hold appreciated assets may find it is more beneficial to donate assets that have unrealized gains than to donate cash. Again, if assets are sold to get cash for the donation, the individual would still owe tax on the amount of the gain. On the other hand, if the assets are donated directly to the charity there would not be any capital gains tax due since the gains have not been realized. The giver is also able to claim the full fair market value of the donation as a deduction. As an additional benefit, unlike the case when gifting to individuals, assuming the charity is a tax-exempt entity, the charity will not owe any taxes on the asset once sold. Once again, strategically planning to donate appreciated assets instead of cash helps to maximize your giving, since in this case a capital gains tax can be completely avoided.

Step-up in cost basis

Under the current tax law, beneficiaries who receive appreciated assets after the original owner passes away do not inherit the original cost basis and tax liability for the assets. Instead, these assets are passed on at the higher current market value to the beneficiary to create a new adjusted basis. Similar to charitable giving, deferring gains in this manner has a significant benefit since the capital gains tax can be avoided altogether. While there are plans to look at changing this tax-free step-up in basis, it may be that proposing these changes will be easier than obtaining congressional approval of such changes.

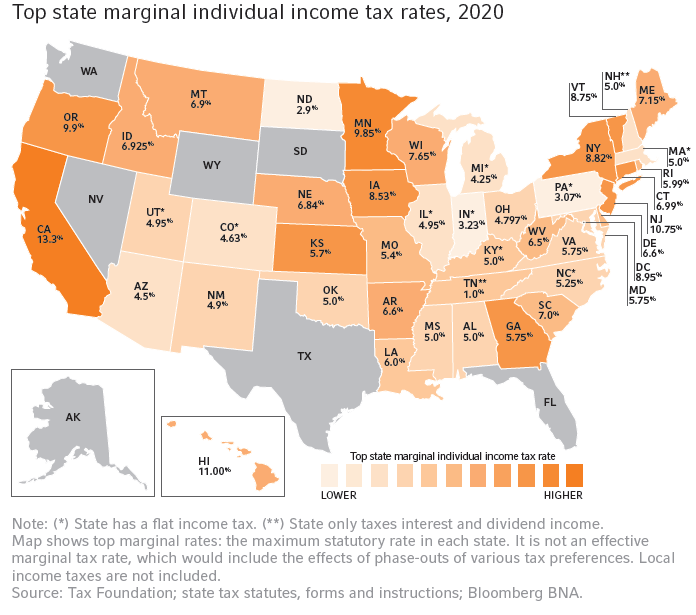

Lower state tax rates

Many of the potential benefits of kicking the can down the road have focused on federal tax law. But it’s important to keep in mind tax considerations at the state and local levels as well. For example, individuals may spend their working years in high income-tax states such as California or New York, but may retire in a state where the income tax rate is significantly lower or potentially 0%. Having the ability to postpone the tax bill until a lower state income tax rate applies can help improve after-tax outcomes.

Click image to enlarge

Summary: Retaining control over one’s portfolio

Given the current debate over tax policy, we’re reminded that tax rates and tax laws are always changing. Using an investment approach that strives to defer gain recognition can provide the flexibility needed to help deliver the best after-tax outcome as additional tax changes come forward.

While the math of the power of compounding of taxes not paid is powerful, there are additional reasons to consider the deferral of recognizing gains. While one should not let the tax tail wag the dog, deferral of gain recognition is an example of where kicking the can down the road is a good thing.