Tax rate uncertainty: Should investors consider realizing gains sooner vs. later?

Investors hate uncertainty. Today’s tax rate environment is the definition of uncertainty. This lack of clarity makes financial planning challenging. If tax rates are going up, should investors do anything today in advance of changes that may or not happen? How might possible tax increases impact existing portfolios? For appreciated assets, should investors consider paying a possibly lower tax today and re-investing in a tax-smart approach?

President Biden campaigned on increasing tax rates across a wide array of categories. The questions on investor minds are:

- Which rates? (Ordinary income? Pass-through income? Capital gains? Dividends? Carried interest? Corporate? etc.)

- How much?

- What income thresholds?

- What might be the impact to current portfolios?

- And if tax rates are changing, then when?

But it’s not only President’s Biden’s campaign plan to consider. There are many (Senate, House, outside groups) contributing ideas and tax plans. The final bill will be a compromise for whatever it takes to secure 50 votes in the Senate.

To help understand how a tax increase may impact existing portfolios, let’s focus on capital gains tax rates.

Long-term capital gains/Qualified dividends

Currently, long-term capital gains (LTCG) and qualified dividends enjoy preferential—lower—tax rates than ordinary income, short-term capital gains and non-qualified dividends for investors above a certain threshold. Then-candidate Biden campaigned on increasing these rates to equal the higher ordinary income tax rates for taxpayers making more the $1 million. That is a big number. Much of the recent discussion seems to be bringing this threshold way down.

Biden also campaigned on not increasing taxes for couples with taxable income less than $400,000. We will see where that goes in future discussions.

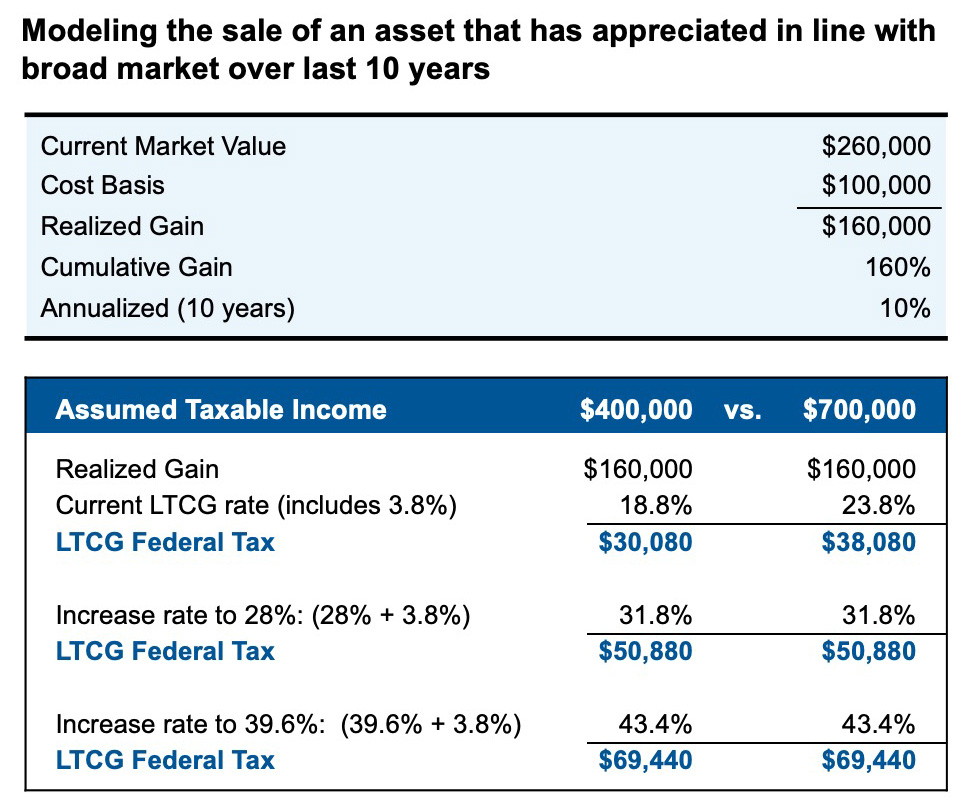

Let’s look at the dollar impact of increasing LTCG rates to a married couple, Joan and Joe Taxpayer. We will assume that Joan and Joe have a hypothetical stock they purchased 10 years ago for $100,000. And this stock has grown in line with the S&P 500 Index at an annualized return of 10% per year, for a gain of $160,000. (We assume no reinvesting of dividends or similar distributions that would adjust the basis.)

Joan and Joe want to know what a change to the LTCG rate might mean to this investment. Given the lack of clarity on how LTCG may change, let’s look at a LTCG tax rate increases of both 28% and 39.6%. The 28% could be a compromise number lower than the 39.6% that Biden campaigned on. Again, the campaign plan stated taxable income of more than $1 million, but lowering this threshold will certainly be debated.

If their taxable income is $400,000 and the LTCG rate increases to 28%, their tax bill goes up by $20,800—a 69% increase. This increase might give Joan and Joe Taxpayer something to consider. If their taxable income was $700,000 (or higher), an increase to a 28% rate comes with an increased tax bill of $12,800—a 34% increase.Again, something worth considering. The tax rate increase to 39.6% (the top proposed rate for ordinary income) represents a material difference in tax expense and would be something worth evaluating.

What should the client do? It depends. Do they plan on selling this asset regardless of what happens to tax rates? If they are certain to sell in the next 12-18 months, they may want to consider pulling the transaction forward into 2021 and not waiting until 2022.Should they consider selling regardless to take advantage of the current tax rate? The answer depends on if they have a more compelling investment alternative.

Does the original investment rationale still make sense? If not, maybe this is a chance to pay the tax and move to a more tax-smart investment option. Would the sale make sense in the context of the total financial plan and investment goals? Each scenario will depend on specific circumstances.

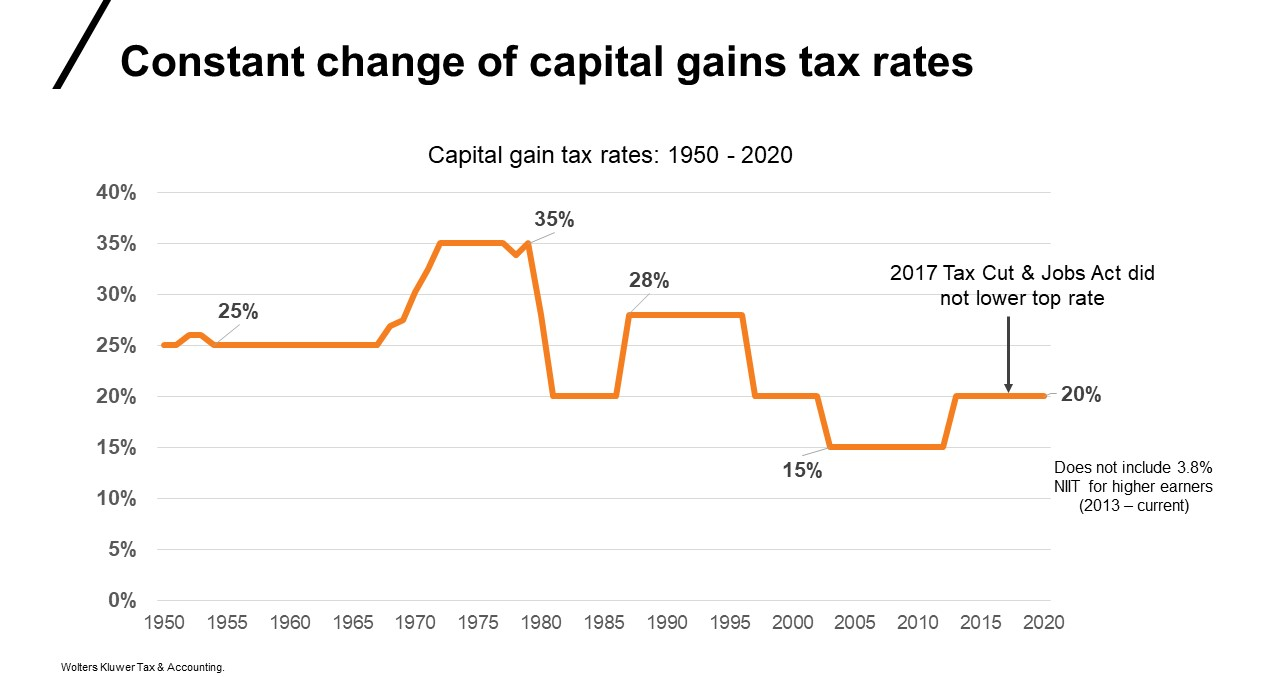

History of capital gains tax rates

The uncertainty around the size, the threshold and timing of any rate change makes much of the analysis challenging.

While this can be frustrating, remind your clients that the capital gains tax rate has changed over time. Politicians will continually turn these dials in the constant battle of aligning federal revenues with expenses and/or aiming to achieve specific policy goals. See the pattern in the exhibit below for the path on capital gains tax rates. Note that the passage of the Tax Cuts and Jobs Act in December 2017 did not reduce the top rate on capital gains.

When?

Focus on the enactment date of any tax changes—not necessarily when a bill may be passed. As I wrote previously, it seems that anything passed this year would not be effective until January 2022. The longer the process takes, the more likely that date will become. Tax reductions have generally been retroactive while increases take effect the following year. If that is the case, you will have time to have discussions with clients.

Keep your eye on how willing the more moderate Democratic senators are to some of the tax ideas put forth. Not every idea or headline you see will gain traction. And getting all 50 Democratic senators on board will be no easy task. It’s not impossible, but it will not be a rubber-stamp approval.

The bottom line

Tax proposals and ideas are coming at us quickly. Any final tax bill will go through many negotiations and changes to secure the needed votes for passage. Look for tax changes (or attempted changes) to:

- Capital gains and dividend tax rates and thresholds

- Ordinary income tax rates and thresholds

- Treatment of pass-through income

- Corporate tax rates

- Carried interest

- Lower threshold for estates

- Reducing or eliminating the step-up in basis for appreciated assets at death

(Note that increases to ordinary income tax rates and lowering of the estate threshold is scheduled to happen after 2025.)

Investors may want to consider pulling some capital gains recognition forward in 2021 (if possible). The same goes for dividends. Deferring any deductions into later higher tax rate years may make sense as well, since tax deductions will generally have more value with higher rates.

In the example laid out earlier, you can see the impact on an increase in the capital gains rate for an investment that has appreciated in line with the broad market over the last 10 years. The impact is not immaterial. It may be an opportunity to realize the gain and move to a more tax-smart investing approach.

Discussions should continue to focus around what makes sense in line with the financial plan and goals for each investor. Given so little clarity on specifics, it really is a case of not letting the tax dog wag the tail. But it does seem like rates are going up.