With Tax Day fast approaching, your clients may be asking how

the recent tax changes will impact their portfolios. Here are a few related topics that have been coming up in my discussions with advisors lately.

- Tax rates on investment gains didn’t change

- Changes to the Kiddie Tax may catch many investors by surprise

- Determining the pass-through income deduction is confusing

- What should we call the new tax bill?

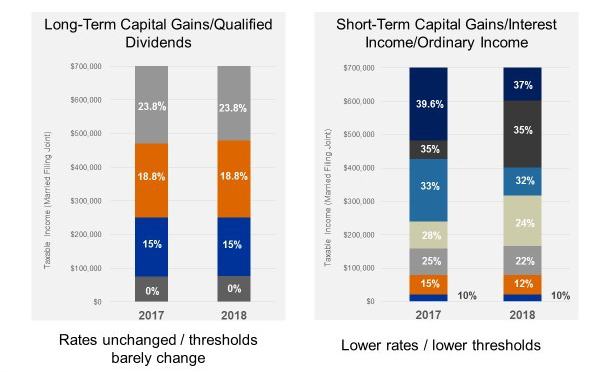

Tax rates didn’t change for long-term investment gains

Most of the headlines about the Tax Cuts and Jobs Act (TCJA) have focused on the reduction of the taxable income thresholds and the generally lower tax rates applied to taxable income. One aspect that tends to get glossed over is:

Tax rates on long-term capital gains and qualified dividends did not change. Yes, the taxable

thresholds for these investment gains changed modestly—but nothing compared to the revisions for taxable income, short-term capital gains, interest income and non-qualified dividends, as you can see in the charts below—and their rates didn’t budge.

Source:

Source:

What’s the key takeaway for investors and advisors?

Tax rates didn’t go to 0%. Anyone with gains/taxable income above $77,400 for Married Filing Joint (MFJ) status is still paying taxes. Being tax-smart about investment gains remains just as important under TCJA as under prior tax law.

Don’t let changes to the Kiddie Tax catch you and your clients off guard

Changes to the “Kiddie Tax” haven’t received as much press coverage as other tax changes. I won’t go into the details on when/how/why the kiddie tax applies. But broadly, it centers around the unearned income of dependent children under specific circumstances. The tax kicks in for dependent unearned income above $2,100 and often is the result of investment gains from mutual funds, stocks and bonds.

The tax rate applied to that unearned income has increased—quite dramatically. Prior to the TCJA, the tax rate for income above the $2,100 was generally

the parents’ marginal tax rate. Assuming the parents’ filing status was MFJ, this marginal rate could progress up to 39.6% for taxable income above approximately

$479,000.

Under the TCJA, the marginal tax rate on unearned income is no longer that of the child’s parents. Rather, it is now

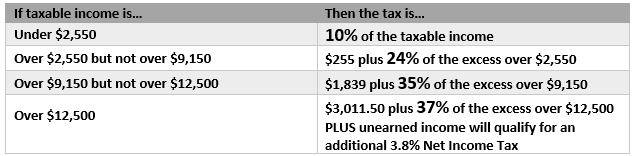

the tax rate applied to trusts and estates.

2018 Trust & Estate Tax Rates (and Kiddie Tax rates):

Source:

Source:

As the table above shows, the trust tax rates are extremely punitive: They hit the top marginal rate of 37% with taxable income as little as

$12,500. What’s more, the 3.8% Net Investment Income Tax (NIIT) kicks in at taxable income above $12,500 for trusts—where it doesn’t apply for a couple filing MFJ until Modified Adjusted Gross Income (MAGI) above $250,000.

That is a very material difference!

What’s the key takeaway for investors and advisors?

Spare your affected clients an unpleasant surprise on the change in the Kiddie Tax rate. Warn them about it and consider tax-smart investments that strive to maximize pre-tax return while also working to limit taxable distributions to provide attractive after-tax returns.

Pass-through income determination is hard

One of the goals of the TCJA was to simplify the tax code. The increase in the standard deduction which will absolve many taxpayers from needing to itemize their deductions and deal with the hassles around Schedule A, accomplishes some of that simplification goal.

But I would argue that the part of the TCJA that addresses the 20% pass-through income deduction tied to certain partnerships, S-corps and sole proprietorship is the

opposite of simple. In my opinion, this part of TCJA should be renamed the “CPA/Tax Attorney Full Employment Act.” Application of this pass-through deduction will be challenging in practice. An unintended consequence resulting from this part of the TCJA is the treatment of pass-through income resulting from Real Estate Investment Trust (REIT) investments.

A direct holder of a REIT will generally be able to apply the 20% business income deduction, but a holder of a REIT

mutual fund will not. Unfortunately, this distinction seems to have been the result of an oversight in the bill drafting and finalization process—it doesn’t appear that REIT mutual fund holders were intentionally omitted. However, it will literally take

an act of Congress to fix this mistake.

What’s the key takeaway for investors and advisors?

You may want to encourage any clients who have meaningful income from pass-through entities to consult with a tax professional. As for REIT mutual funds, we still believe their diversification and return pattern may help improve risk-adjusted after-tax returns. It’s unfortunate that REIT mutual fund holders can’t get the intended tax break but we don’t consider that a reason for investors to avoid REIT mutual funds.

Is it really called the Tax Cuts and Jobs Act?

As originally written, the bill was titled the Tax Cuts and Jobs Act (TCJA). But because nothing is easy in Washington, D.C., in last minute parliamentary proceedings, the official name was changed to

“To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018”. Unfortunately, that name doesn’t have a short abbreviation or catchy acronym: TPRPTTIIIVCRBFY2018 hardly rolls off the tongue! Although the Tax Cuts and Jobs Act is not the official name, many commentators have stuck with the original name—and shorter abbreviation—the TCJA. It’s good enough for me.

The bottom line

While the changes to the U.S. corporate tax code within TCJA are permanent, most of the changes impacting individual taxpayers will expire after 2025. Given that we have two presidential elections before then and House/Senate elections every two years, it’s likely that the tax code will evolve. The best response remains to help your clients invest smartly around taxes. The goal is not avoiding a tax, but achieving higher after-tax wealth. Looking for tax-smart equity and muni bond investment options may help in reaching successful outcomes for clients’ taxable assets.