2024 Tax rates: Essential insights for financial advisors

Executive summary:

- When it comes to taxes, it's always best to be prepared for any future changes that could either benefit or hurt your clients

- This year's inflation-related adjustments to tax brackets and standard deductions could give some of your clients more flexibility to manage their capital gains

- Advisors should prepare now for the expected expiration of the 2017 Tax Cuts and Jobs Act

The page has turned, a new calendar has been hung. Many changes to our tax system are behind us now, and yet there is lots ahead of us. We are nearly at the midpoint of this decade. What does that mean for us and how our income and investments are taxed? As tax-aware financial advisors, what should you be prepared for this year, and more importantly how can you help your clients plan for the future?

There are two key things to focus on:

- Immediate changes you need to know about 2024 and tax rates

- What you need to plan for in 2025 and beyond

2024 Tax news and changes

There are no major changes to tax law expected at the Federal level this year; but it is going to be a busy election year so stay tuned. And there are changes to tax brackets that you need to be aware of that might actually benefit your clients, and can help you plan for their future tax bills.

There are a number of tax-related items that are adjusted for inflation, including income tax brackets and the standard deduction. First, the standard deduction for taxpayers increased. This allows tax filers to have a larger upfront deduction, which helps lower the Adjusted Gross Income (AGI) on their tax returns. Second, the income tax levels for each tax bracket have increased. This also should be a net benefit to taxpayers as the threshold to move into a higher tax bracket has risen. Thirdly, for capital gains taxation the income brackets have increased as well. This could mean more flexibility for some investors to realize gains. The specific tax brackets and rates can be found in the tables below.

EXHIBIT 1: STANDARD DEDUCTIONS

| 2022 | 2023 | NEW! 2024 | |

| Single | $12,950 | $13,850 | $14,600 |

| Married Filing Jointly | $25,900 | $27,700 | $29,200 |

| Head of Household | $19,400 | $20,800 | $21,900 |

Source: IRS.gov as of 11/30/2023

EXHIBIT 2: INCOME TAX BRACKETS

Table 1. 2024 Federal Income Tax Brackets and Rates for Single Filers, Married Couples Filing Jointly, and Heads of Households

| TAX RATE | FOR SINGLE FILERS | FOR MARRIED INDIVIDUALS FILING JOINT RETURNS | FOR HEADS OF HOUSEHOLDS |

| 10% | $0 - $11,600 | $0 - $23,000 | $0 - $16,550 |

| 12% | $11,601 - $47,150 |

$23,200 - $94,300 | $16,551 - $63,100 |

| 22% | $47,151 - $100, 525 | $94,300 - $201,050 | $63,101 - $100,500 |

| 24% | $100,526 - $191,950 | $201,050 - $383,900 | $100,501 - $191,950 |

| 32% | $191,951 - $243,725 | $383,900 - $487,450 | $191,951 - $243,700 |

| 35% | $243,726 - $609,350 | $487,450 - $731,200 | $243,701 - $609,350 |

| 37% | $609,350 or more | $731,200 or more | $609,350 or more |

Source: IRS.gov as of 11/30/2023

EXHIBIT 3: CAPITAL GAINS TAX BRACKETS

Table 6. 2024 Capital Gains Tax Brackets

| FOR UNMARRIED INDIVIDUALS, TAXABLE INCOME OVER | FOR MARRIED INDIVIDUALS FILING JOINT RETURNS, TAXABLE INCOME OVER | FOR HEADS OF HOUSEHOLDS, TAXABLE INCOME OVER | |

| 0% | $0 | $0 | $0 |

| 15% | $47,025 | $94,050 | $63,000 |

| 20% | $518,900 | $583,750 | $551,350 |

Source: IRS.gov as of 11/30/2023

Generally speaking, for most taxpayers and investors, these 2024 changes should be net positives. The higher thresholds for income tax brackets could also allow you to start planning for future potential tax increases. An additional change for some taxpayers to be aware of is the "estate and gift tax exemption" increase from $12.92 million in 2023 to $13.61 million in 2024.

Many of the tax facts and figures shown above are available in this handy document that we produce annually for advisors and their clients.

2025 Elections and beyond

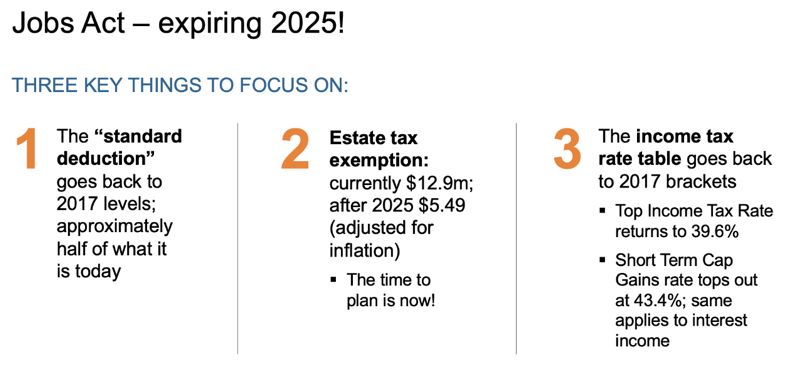

Let's cut to the chase. The key things to remember are: 1) 2024 is a full election year and 2) the Tax Cuts and Jobs Act of 2017 expires at the end of 2025.

We have received an assortment of questions around the upcoming presidential election and what that could mean for tax bills in 2024. The bottom line is that the impact is expected to be minimal. There will be very limited ability by Washington DC to effect comprehensive tax law changes this year. There are two primary reasons for this. First, being an election year there's typically a decrease in substantial legislation changes in Congress. Second, the slim vote margins in both the House and the Senate make it difficult for either party to push through major changes.

As a side note, this is something you can let your clients know if they are worried about what the election outcome could mean for their investments. Generally, markets – just like taxes – move on considerations outside of politics.

That being said, the outcome of the election will influence the different tax changes that are major parts of the Tax Cuts and Jobs Act of 2017 (TCJA). The three major items we are focused on are 1) a reduction in the standard deduction, 2) the estate tax exemption declining substantially, and 3) the income levels of the tax brackets being reduced as well as tax rates increasing.

Source: https://www.taxpolicycenter.org/taxvox/buckle-2025-promises-be-historic-year-tax-and-budget-policy

https://www.irs.gov/

While it's too early to make predictions on political outcomes (there probably is never a good time to try to predict politics!), there are things we all should be planning for. Once 2025 rolls in and the new administration is in place in Washington DC, there will be active conversations related to tax law changes. What you can do right now is take advantage of today's historically low tax rates to help your clients potentially reduce their tax bill. If you are wondering how, consider these three things:

- Transition out of low cost-basis securities using today's relatively low capital gains tax rate.

- Ensure "non-qualified" accounts (which refer to taxable investments if the term is unfamiliar) are fully tax managed. This entails optimizing the tax efficiency of both equities and fixed income investments, while also aligning the asset allocation with tax considerations.

- Help your clients thoughtfully plan their legacy. Using today's estate tax and gift tax exemption amounts, have meaningful discussions about how to plan for the next stage. Whether its directing funds towards charitable contributions or leaving a legacy for heirs, proactively address tax implications to preserve a greater portion of their assets. Start planning now.

Take action

Use the certainty of today plus the uncertainty of tomorrow to put your clients and their investments in a better position now. Procrastination is not an ally in this endeavor. Seize control over what you can influence—and one significant aspect within your control is the taxation of investments. Almost all of us will face an annual tax bill on April 15. But there are steps you and your clients can take now to make the next one as small as possible. We can help; let us help you. At Russell Investments we have a multitude of resources on tax-managed investing, providing insights into proactive measures you can implement now and throughout the year. Take the first step today by exploring one of our most popular guides on maximizing after-tax wealth.