The time to embrace tax management is now

Editor's note: Unlike most of our other articles, this one is aimed at investors. If you’re an advisor, consider sharing this one with them.

It seems likely that taxes are going to go up.

The Biden administration has made it clear raising taxes is a key part of funding its agenda. You can’t hide. Ignoring won’t help. The time for action is now.

We are past the point of campaign rhetoric and are now at the stage of actual proposals. We have already seen the opening salvos in what we know is likely to be a drawn-out negotiation to increase taxes.

What do we do next? Where can we turn for help?

There is no magic bullet. Taxes are as certain as death, to paraphrase a famous quote usually attributed to Benjamin Franklin. But at Russell Investments we believe that you shouldn’t pay more taxes than required. There are a few tried and true ways to help you keep more of what you make in your portfolio and your pocket. Let us explain.

The only certainty is uncertainty

What we don’t know is what tax rates will look like going forward, or even which thresholds and which taxes—income, capital gains, estate, corporate, etc.—will be impacted. This includes tax strategies such as estate planning and issues such as estate tax exemption limits and cost basis step-up rules. The negotiation and the horse-trading in Congress have only just begun.

What we do know is that there is a deep desire by the new administration to increase revenues to help offset the cost of the support programs related to COVID-19 and other policy goals.

In the face of this level of uncertainty, there is something we can do:be prepared.There are actions that can be taken now to be ready for when there is clarity on which taxes will increase and by how much.AND there are steps that can be taken today that you can benefit from no matter what happens next.

Click image to enlarge

Tax rates assume tax status of Married Filing Joint (MFJ).

Source: https://www.taxpolicycenter.org/taxvox/biden-would-raise-taxes-4-trillion-over-10-years-mostly-highest-income-households

Embrace tax management

Some investors may believe that they are dodging a larger tax bullet through the use of exchange-traded funds (ETFs) or passive investment solutions such as index funds. To paraphrase a commercial of old, this is not your father’s tax-efficient portfolio.Why settle for something that strives to be a little better than average?That’s what you may get by investing in ETFs and index funds.Yes, they often do better in lowering the cost of taxes than the average mutual fund, but why not aim higher than beating the average?Why not do better by a lot?

At Russell Investments, we believe you can attack the tax problem head-on.Our suggestion? Embrace active tax-managed investing.

What is active tax-managed investing?

It can be considered a better way to get to a more comfortable retirement: it’s about minimizing the impact of taxes on your portfolio and thereby helping maximize your after-tax wealth. Tax-managed investing and tax management work in partnership. Tax management lowers the cost taxes can and do have on your returns and portfolio value.Tax-managed Investing is a more thoughtful way of investing your hard-earned money.

Tax management is more than just tax-loss harvesting once a year, and also more than just using a buy-and-hold approach.By embracing active tax-managed investing and using all of the techniques that are part and parcel of true tax management, it is then possible to keep more of what you have earned.Tax management is about focusing on the long term; it uses tax loss harvesting as a way to offset the tax impact of realized capital gains.Minimizing the tax cost of dividends as well as interest payments is an additional component of tax management and tax-managed investing.Being smart about turnover and trading activity and maximizing the use of tax-lot level accounting when it comes to that trading activity is an advancement in tax management that takes tax-managed investing to another level.

Tax management is about both sophistication and simplification.We here at Russell Investments believe investors deserve more—more after-tax wealth and a better retirement outcome.

Look at the transformation in automotive technology to understand the evolution of authentic tax management.For years, small tweaks in car design and their engines, transmissions, the way fuel is combusted, even the composition of the rubber in the tires were made to squeeze a little more mileage out of every gallon.More recently, we experienced a major evolution in combining electrification and combustion to take a major leap forward in automotive technology.

That leap is similar to the evolution of tax management for investment portfolios.Instead of little tweaks, active tax management has progressed by ensuring every part of the portfolio is considered when it comes to controlling the tax impact. This includes everything from trading activity to tax-loss harvesting (an activity that generates tax assets and creates tax alpha) to harvesting frequency to tax-lot level accounting to yield management to interest taxation.Even asset location within the model portfolio is considered as critical to after-tax success.

Each of these areas left unmanaged and uncontrolled could be negatively impacted by any new and upcoming tax law changes.Passively waiting for those changes (the passive management approach) will not cut it. Active tax management allows you to more directly attack the problem. Doesn’t that sound like a better strategy?

The only constant is change

But (there always is a but) what do you do when you eventually need to sell your holdings? For example: cash out to fund a major purchase or pass a legacy along to heirs. Might this be more aggressively taxed under the proposed tax regime?

Yes—this is a central part of the new tax proposals.There are many unknowns on these topics as well, and the level of nervousness is understandably high.

Just remember … the only constant is change.

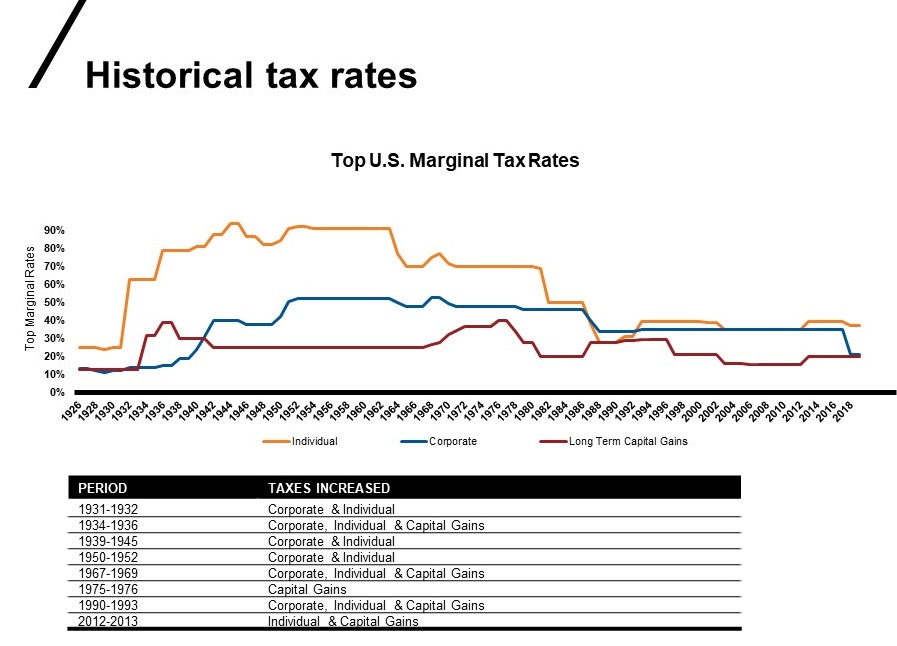

Taxes and tax rates come up as a conversation point, and even more so an action point, during every presidential administration.Just take a look at the variety of tax changes that have occurred since 1926.

Click image to enlarge

Source: Russell Investments, Tax Policy Center, St. Louis Federal Reserve

Take action now

What should you do?Begin by not being rash on the one hand nor complacent on the other.Realize that taxes are unlikely to go down from here, and embrace tax management for your taxable accounts.Making the switch from where you are right now to a portfolio better built to manage for taxes could potentially be the best strategy at this time.

Once you are on the tax-managed path it will be easier to wait out higher tax regimes on the hope (and expectation) that tax rates may decline in the future.There is no guarantee this will happen, but selling when tax rates are high is a guarantee of tax-related capital destruction.

Like I said, you can embrace a better option today by taking action and embracing tax management.After that, waiting it out to see what the future holds could very well be your best choice.

Let us help you. With our Tax Impact Comparison Tool, you or your advisor can run an analysis that shows the tax cost of a portfolio compared to one that uses a more optimal tax management strategy.In addition, we have additional resources that can provide a payback period analysis which shows how fast investors can make up the tax cost of switching.Reach out to your financial advisor.

Take the first step, take action and become informed.Be an informed investor, be a tax-smart investor.Embrace tax management.