Not all tax-managed solutions are created equal

As humans we try to make sense of things. This is necessary for survival. We order, segment and compartmentalize things so that the we can move forward with our daily lives. While in many ways this is good and necessary, there are drawbacks to this. Too often, it ends up in a situation where we throw out the baby with the bath water as the phrase goes. Sometimes we need to take a step back and say, what am I missing?

Not all tax-managed solutions are created equal

The tax-managed space is one such area where we see this happen. There are a number of views investors and advisors have when it comes to a topic such as tax management. Many of them are potential positives, such as:

- It lowers my tax bill

- It helps me grow my after-tax wealth faster

- My money is working for me better and faster

- It’s not what you make, it’s what you get to keep

- Unfortunately for some, the topic of tax-management has some other, less than positive things come to mind:

- My returns might not be as good if I do this

- Tax-management means I have to give up something

- If I just run faster I can outrun the tax bill

Here's the thing. While all of the above items, good and bad, may be true at times or may be true with specific solutions, broadly placing everything in the same bucket and then negatively labeling is definitely limiting. It’s the equivalent of throwing out the baby with the bath water.

It’s about outcomes

At the end of the day, what is likely most important to an investor and advisor is does this fit the bill, and does it do what I need it to do? In a taxable account, this means two things: 1) did I get the return I need for this strategy to meet my goals, and 2) how do I keep most of the return in my pocket by potentially minimizing the drag of taxes?

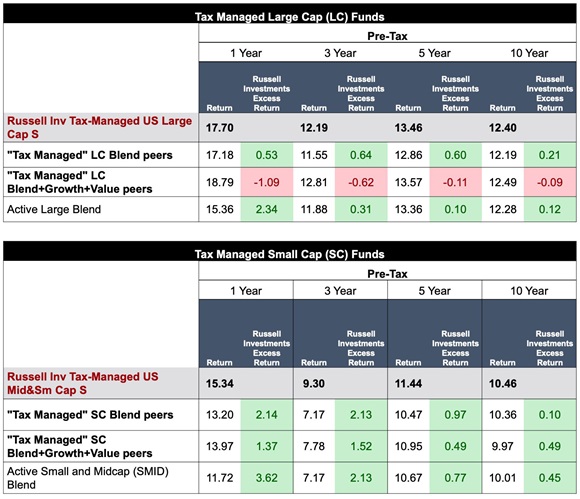

Actual numbers: Pre-tax returns

Let’s take a look at the actual numbers. Table 1 shows the pre-tax returns side by side for two different asset classes. What is being displayed here, in order, is a comparison, first looking at U.S. large cap, followed by U.S. small/mid cap. The comparison shown is the Morningstar blend universe for each asset class, a tax-managed peer group of just blend managers, a tax-managed peer group consisting of blend, growth and value managers, and then the Russell Investments tax-managed fund for that specific asset class. The tax-managed peer group is a sub-group created out of the Morningstar universes by screening for the word tax in the fund’s name.

Pre-tax returns (as of December 31, 2020)

Performance quoted represents past performance and should not be viewed as a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Current to the most recent month-end performance data may be obtained by visiting https://russellinvestments.com.

Tax-Managed U.S. Large Cap Fund : Annual Total Operating Expenses: 0.95% Annual Net Operating Expenses: 0.92%*

Tax-Managed U.S. Mid & Small Cap Fund : Annual Total Operating Expenses: 1.29% Annual Net Operating Expenses 1.20%*

Source: Morningstar Large Blend, Morningstar Large Growth, Morningstar Large Value, Morningstar Small Blend, Morningstar Small Growth, and Morningstar Small Value universes. See disclosures at end of article for peer group methodology. Active Large Blend: US Fund Large Blend excluding ETFs. Active Small and Midcap (SMID) Blend: US Fund Small Blend and US Fund Mid Blend excluding ETFs.

What you can see here is, on a pre-tax basis over the last one, three, five and 10-year periods, having a focus on tax-management did not harm returns. In fact, both tax-managed peer groups listed here as well as the Russell Investments funds outperformed the Morningstar Blend universes in both asset classes! This hopefully dispels the myth that by having a focus on tax-management an investor is giving something up. Again, while there might be periods where performance results could fluctuate and move the tax-managed comparisons to negative, this clearly shows there is not necessarily a disadvantage being created for investors who choose to go down the tax-managed route.

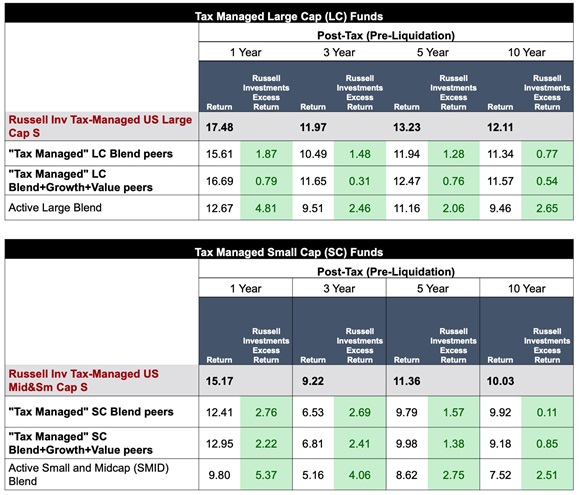

Actual numbers: After-tax returns

In the second comparison shown here in Table 2, we mimic the periods, asset classes and constituent comparison of the first table, but instead place the focus on what the after-tax returns look like.

After-tax returns (as of December 31, 2020)

Performance quoted represents past performance and should not be viewed as a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Current to the most recent month-end performance data may be obtained by visiting https://russellinvestments.com.

Tax-Managed U.S. Large Cap Fund : Annual Total Operating Expenses: 0.95% Annual Net Operating Expenses: 0.92%*

Tax-Managed U.S. Mid & Small Cap Fund : Annual Total Operating Expenses: 1.29% Annual Net Operating Expenses 1.20%*

Source: Morningstar Large Blend, Morningstar Large Growth, Morningstar Large Value, Morningstar Small Blend, Morningstar Small Growth, and Morningstar Small Value universes. See disclosures at end of article for peer group methodology. Active Large Blend: US Fund Large Blend excluding ETFs. Active Small and Midcap (SMID) Blend: US Fund Small Blend and US Fund Mid Blend excluding ETFs.

Highlighted here, which should come as no surprise after seeing the results from the first table, is that the after-tax returns for the different constituent categories have a widened positive gap versus the overall Morningstar blend peer universes. Not only do the tax-managed peer groups maintain their more positive results vs. the Morningstar peer universe, they expand it on an after-tax basis! This further hopefully dispels the myth that by embracing tax-management you need to give something up. The reality shown here is that by embracing tax-management, you may gain something instead.

Even more impressive in this analysis are the outcomes generated with the two Russell Investments portfolios relative to both the tax-managed peer groups and the Morningstar peer universes. There is clearly a dispersion of returns across managers focused on tax-management. Through a strong tried-and-true investment process focused on generating both solid pre- and post-tax returns, the Russell Investments portfolio is able to set itself apart. Hence, not all tax-managed solutions are created equal.

Taxes need to be an investment consideration

Taxes are a cost when it comes to investments. The impact of taxes is a drag on a portfolio’s after-tax returns. In essence, it’s a fee of sorts—a government fee being applied to investment portfolios. We believe this is something that should be managed to both minimize its impact and maximize the after-tax return on investor experience.Tax-management should be a major consideration when constructing an investment portfolio for a taxable investor. Because at the end of the day, it’s not what you make, it’s what you get to keep.