The hidden cost of cheap portfolios

Once upon a time, in what feels like eons ago, I boarded a flight from Denver to Austin. Since it was a short flight, I decided to fly as cheaply as possible: I chose a discount airline and searched for the lowest fare I could find. I was secretly proud of my frugality.

However, although I had satisfied my wallet, I soon learned that I had inadvertently punished myself in other ways. Once I arrived at the airport, I was charged extra for my check-in bags (eliminating the cheap fare advantage). My flight was delayed. The customer service call center had hour-long wait times. The mobile app was useless. The staff at the gate were rude and poorly trained. The customers were all miserable. When we finally did board the plane, the seats were stiff and uncomfortable. By the time I arrived in Austin it was hours past when I was supposed to land. I was exhausted, frustrated, and remorseful for having flown on a cheap carrier.

Cheaper isn't always better

In the financial industry today, there seems to be a race to the bottom from a fee standpoint. Clients want the least expensive portfolios, with the best return and zero risk! They challenge their advisors on the fees they’re paying and are always on the lookout for the cheapest product or service.

But cheaper isn't always better. Intuitively we know this. We know that when we pay for a cheap product, we are going to get a sub-par experience. This can create additional costs we didn't initially factor in.

We’ll show how a relatively inexpensive portfolio can actually cost an investor more than 7% in forgone return. Let me explain.

The hidden cost of cheap things

Certain portfolios like passive exchange-traded funds (ETFs) or index funds offer low-cost exposure to market sectors. But, just like a cheap flight, they have setbacks.

Behavioral costs

When an airplane experiences turbulence we all crave human reassurance. There have been a few moments in my life when I’ve been on a plane during horrible turbulence and found myself wondering if those were my last moments on earth. When the pilot came on the speaker and told us in a calm, soothing voice that we were just experiencing a little storm and it was nothing to worry about, we all breathed a sigh of relief. Having reassurance from a professional who knows exactly what’s happening is sometimes all we need to weather storms.

During times of market turmoil (such as the 2020 global pandemic), clients and advisors need reassurance from their investment providers. They need insight into what is happening and what their investment partners are doing to navigate the storm.

But many cheap portfolio providers do not have a robust service and support team. They charge low fees and therefore don’t have excess profits to invest in a well-developed external sales force. When advisors or clients have questions about cheap portfolio products, they must dial into a call center. The representatives at these call centers are mostly young professionals with only a few years of experience in the business.

By contrast, a large investment solutions provider would have an exceptionally well-trained wholesaler force. Many wholesalers have been in the industry for multiple decades. They have seen all kinds of market environments. Many of them have industry designations that give them even greater insight into how to navigate changing market conditions. You cannot pay these individuals entry-level salaries. A large, global firm would not be able to attract this talent if they were charging the lowest fees out there.

During the 2020 pandemic, Russell Investments worked hard to keep our business partners well informed. Many of our wholesalers were able to provide advisors and their clients the reassurance they needed to stay invested in the markets. We were the pilot during a storm. We helped prevent clients from making emotional, knee-jerk reactions. By preventing poor behavioral mistakes, we may have helped reduce the soft costs associated with emotional decision-making. This likely saved many clients from panic selling, which kept them in the market and potentially earning money. Would you get the same result by dialing into a call center?

Many low-cost portfolio providers did not have the same level of intimate service or support to solve for this need. This begs the question: during times of market turbulence who do you want to be flying with—a cheap carrier or a premium airline?

Higher tax drag

When you buy a cheap airline ticket, many of those low-cost carriers charge you extra for your bags. Sometimes these bag fees can completely nullify the discount you received on your fare. This means that when you think you’ve saved money on the trip, when you factor in those additional fees, you’ve actually incurred higher costs.

Cheaper portfolios like ETFs or index funds have a reputation for being tax efficient. This is because they have less turnover than active funds and in some cases this can result in lower capital gains. But, that's not the whole story.

At Russell Investments, we believe there is a very big difference between tax efficient and tax managed. Inexpensive portfolios like ETFs and index funds are designed to give you low-cost access to a particular market sector. The goal of the product is to provide low-cost exposure. Tax efficiency is a byproduct of trying to achieve a different objective.

By contrast, tax managed portfolios have the specific goal of providing superior after-tax returns. Russell Investments engages in active year-round tax-loss harvesting to take full advantage of market volatility whenever it strikes. We can actively reduce the tax implications of our portfolios, which helps clients minimize their tax bills and maximize their after-tax returns. We refer to this as tax alpha.

Passive portfolios do not offer an active approach toward generating tax alpha. Especially in the case of ETFs, they are considered tax efficient because of their inherent structure. But they may be limited in their ability to offset taxable events in their portfolios.

At Russell Investments, we have a robust, dedicated team of traders and portfolio managers whose sole job is to harvest losses advantageously throughout the year to offset the gains we are incurring. This requires additional human capital and higher costs than passive counterparts. However, this service strives to lower the tax bill year over year. The additional expense works to lower tax drag and maximize after-tax return.

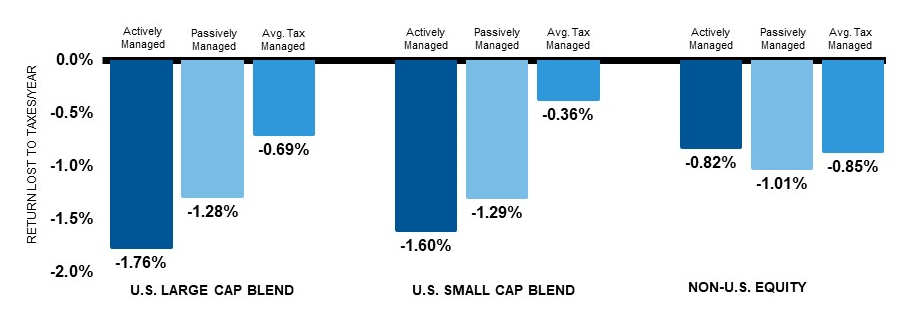

When we look at industry averages and compare the tax drag of active, passive and tax-managed portfolios, we can see that the tax drag is higher for both active and passive portfolios than it is for those which are designed for tax efficiency.

Average annual tax drag for 5 years ending March 31, 2021 (click image to enlarge)

Source: Russell Investments, Morningstar. Morningstar Categories included: US Large Blend, US Small Blend, Non-U.S. Equity = 25% Diversified Emerging Markets / 75% Foreign Large Blend. Average of Morningstar’s Tax Cost Ratio for universes as defined. Passive is defined as being an index fund as reported by Morningstar or part of an ETF Category. All returns are net of fees. *Tax Drag: Morningstar Tax Cost Ratio. See disclosures for methodology.

The tax drag of a cheaper portfolio can be likened to the additional baggage fees that airlines charge. In many cases, the cheaper portfolios have higher tax drags than more premium, tax-managed alternatives.

Adding it all up

Let’s take a sample situation. Let’s compare two investors. One investor places their assets in a passive portfolio, with a low expense ratio. The other investor chooses the premium option and invests in a tax-managed portfolio. They also hire an advisor and pay the 1.00% fee plus a 0.30% platform fee.

At this point, the fee breakdown is as follows:

|

|

Low-Cost Portfolio |

Premium Portfolio |

|

Expense Ratio |

0.30% |

0.70% |

|

Advisory Fee |

0.00 |

1.30% |

|

|

|

|

|

Total Cost |

0.30% |

2.00% |

This is typically where most clients stop their analysis. But let’s now think about the true costs these two investors may face.

Both investors invest on Jan. 1, 2020. Shortly afterward, a global pandemic breaks out, and many countries go into full lockdown. Schools switch to remote learning, businesses close, and the S&P 500 Index drops by 34% in 30 days (the fastest 30% drop in history). On March 23, the index hits a 2020 low.

The low-cost investor (let’s call them Investor 1) begins to worry and calls the 1-800-TOLL-FREE line listed on the website of the product provider. This is the first time this investor has ever dialed into the call center, and the person they are speaking with is a total stranger who does not have the same fiduciary liability that an advisor might have. After asking the representative a few questions about what’s happening, Investor 1 decides that there is too much uncertainty in the market right now and sells their portfolio.

The premium investor (Investor 2) also begins to panic and calls their financial advisor. This advisor knows them personally and also has a high fiduciary standard to uphold when giving advice. The advisor has already been briefed on the situation from their investment wholesalers. They’ve also had calls with other investments firms, so they can see what multiple companies are thinking. The advisor strongly advises Investor 2 to stay invested in the market. Investor 2 complies.

Eight days later, Investor 1 sees the market bounce off the lows and decides to re-invest the portfolio. They acknowledge they might have jumped the gun in selling, but they feel comforted by the knowledge they were only out of the market for eight days.

However, if you follow the orange line in the chart below, it shows us that being out of the market for only eight days cost the first investor 7.00% of their return for the rest of the year. By contrast, Investor 2, who listened to their advisor, stayed invested and avoided that behavioral cost (difference between blue line and orange line).

Click image to enlarge

Source: Morningstar Direct. Balanced Portfolio: 60% S&P 500 Index and 40% Bloomberg Aggregate Bond Index. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

By choosing a cheaper portfolio, Investor 1 underinvested in the resources that could have helped them make a better decision during a market selloff. This contributed to a behavioral mistake that cost the client 7.00% in return by the end of the year. Investor 2 was able to avoid this behavioral cost by paying for a financial advisor and a premium portfolio that came with a well-trained wholesaler team.

By the end of the year the breakdown of costs now looks like this:

|

|

Low Cost |

Premium |

|

Expense Ratio |

0.30% |

0.70% |

|

Advisory Fee |

0.00% |

1.30% |

|

Behavioral Cost |

7.00% |

0.00% |

|

|

|

|

|

Total Cost |

7.30% |

2.00% |

But the tale doesn’t stop there. At the end of the year, Investor 1 and 2 both receive a Form 1099 for their portfolios. Each 1099 results in a tax bill.

Despite holding a passive portfolio, Investor 1 receives a larger capital gain distribution because their portfolio did not have any tools to take advantage of the market volatility that occurred during the pandemic.

Investor 2 held a tax-managed portfolio that actively engaged in tax-loss harvesting during the pandemic selloff. Their tax bill was much lower, resulting in a lower tax drag.

The tax drags of the two portfolios are also listed on the fee schedule:

|

|

Low Cost |

Premium |

|

Expense Ratio |

0.30% |

0.70% |

|

Advisory Fee |

0.00% |

1.30% |

|

Behavioral Cost |

7.00% |

0.00% |

|

Tax Drag |

1.28% |

0.69% |

|

|

|

|

|

Total Cost |

8.58% |

2.69% |

When all is said and done, the investor who paid more for a premium service ended up paying less in overall cost.

The bottom line

To examine the difference between low-cost portfolios and more expensive portfolios, you must calculate the true cost of ownership. You have to factor in the additional soft costs that are incurred by choosing a cheap product.

Low-cost investment portfolios might give you less expensive exposure to the market, but they do not have as much room to invest in robust support staff, analytical tools, active positioning, tax-loss harvesting and so on. When markets experience turmoil you will not have as many resources as you would have with a premium provider to make better decisions. Whether you lose money to poor behavioral mistakes, or tax inefficiencies, cheap products can come with all sorts of hidden costs that reduce wealth in the long run.