The value of an advisor: Why we believe it’s higher than ever

Russell Investments has always focused on the value of advisors. And never was an advisor’s value so obvious as during 2020.

It was a year that tested both investors and advisors in so many ways. Financial markets fell sharply early in the year, when the global spread of the COVID-19 virus forced a sudden shuttering of economic activity, only to recover strongly. Those investors who followed the advice of advisors and stayed in the market tended to fare well.

Most financial advisors had further challenges, as they had to switch to a virtual environment seemingly overnight. For many, harnessing the available technology was a steep learning curve.

That’s why we think it is the perfect time for you to place a sharper focus on the full value of your advice and communicate that value to your clients.

We’ve also reassessed the formula we use in our annual Value of an Advisor report to reflect the broadening role of a holistic financial advisor. Our new formula more closely reflects the tangible benefits of working with an advisor.

Let’s take a look at the full value equation of an advisor’s services. The data clearly shows that the value is much greater than the typical advisory fee.

A is for your active rebalancing philosophy

When markets are rising calmly, it can be easy to underestimate the importance of regular rebalancing. But in a rollercoaster year like 2020, active rebalancing of a portfolio may have helped create a smoother rider for investors.

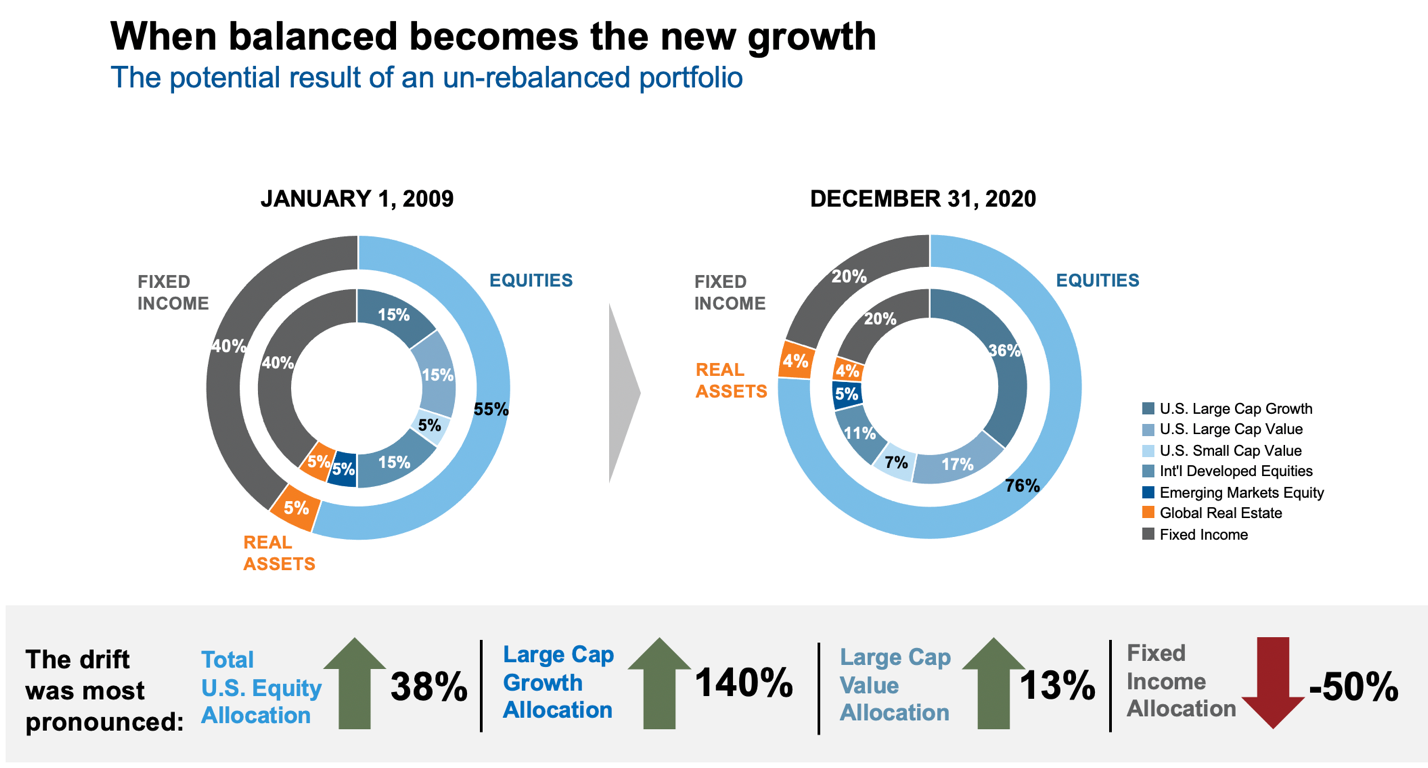

Rebalancing can also help ensure true diversification is still in place. 2020 saw a few key technology names dominate returns over the year and substantially increase their weighting in the S&P 500® Index. Without regular rebalancing, a client’s portfolio could have become overly heavy in large-cap U.S. tech stocks, potentially creating an overweight of risk if that single sector dropped.

For example, if an investor had purchased a hypothetical balanced portfolio of 60% equities and 40% fixed income in January 2009 and it had not been actively rebalanced since then, by the end of 2020, the risk profile of the portfolio would look very different. That original balanced portfolio would have become a growth portfolio, with 80% invested in equities and only 20% in fixed income. That would expose the investor to risk they didn’t agree to and could be a concern if equity markets suddenly reversed, as we saw in early 2020.

Click image to enlarge

For illustrative purposes only. Source: Hypothetical analysis provided in the chart & table above for illustrative purposes only. Source for both chart & table: U.S. Large Cap Growth: Russell 1000 Growth; U.S. Large Cap Value: Russell 1000 Value; U.S. Small Cap: Russell 2000; International Developed: MSCI World ex USA; Emerging Markets Equity: MSCI EM; Global Real Estate: FTSE EPRA NAREIT Developed: Fixed Income: Bloomberg U.S. Aggregate Bond.

B is for behavioral mistakes coming into focus

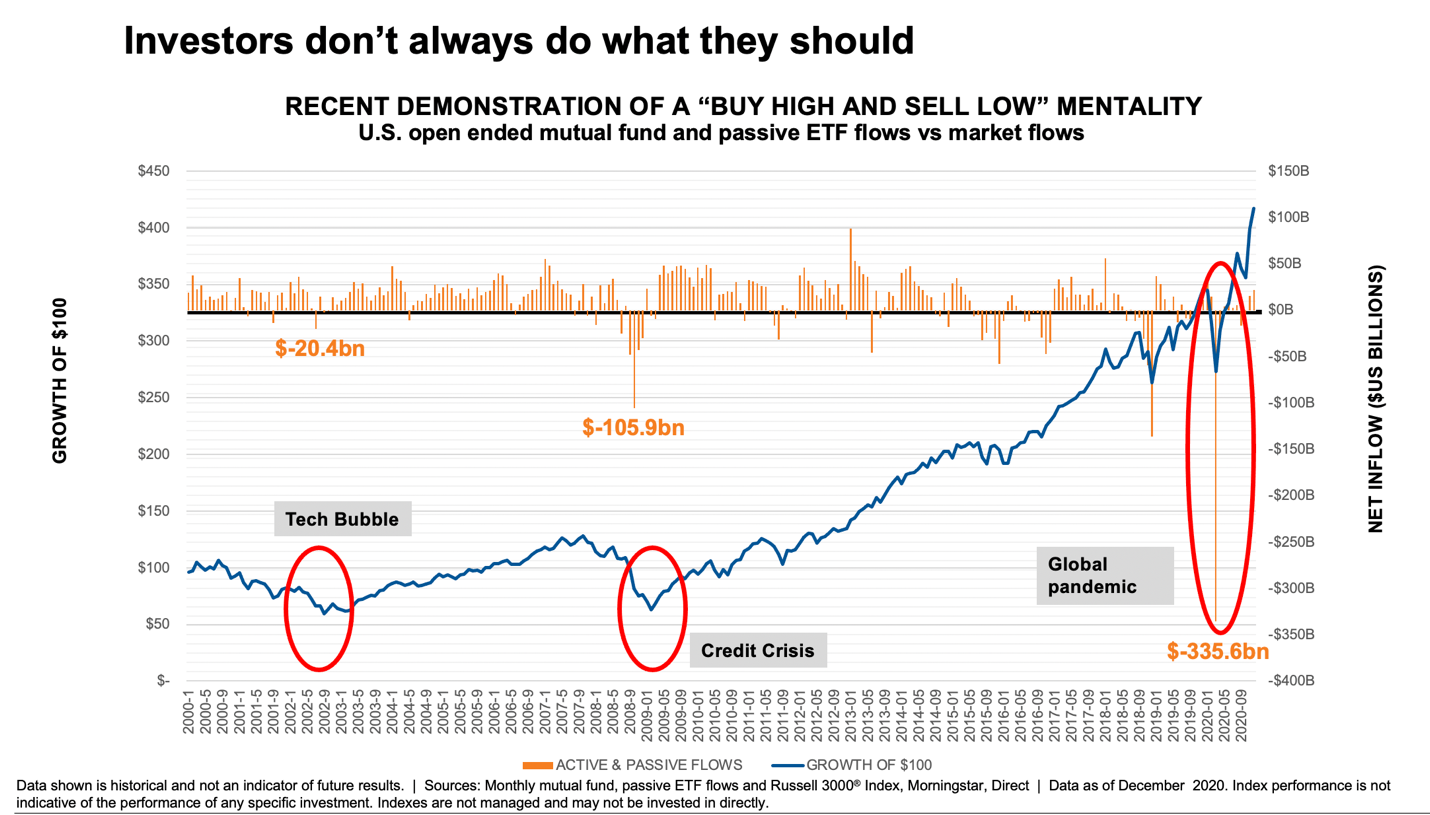

2020 was a wild ride. Many investors were tempted to run for the exit in mid-March, when the S&P 500 Index registered the largest weekly decline since 2008.

This is where the advisor’s behavioral guidance really comes into focus. Without that guidance, many investors could have sold low in March—in fact, $335.6 billion was pulled out of U.S. equities in that month.1 Investors who remained invested saw the index rebound 17.6% in the following three days, and not just fully recover, but actually return 18% by the end of the year. Imagine the hit to a portfolio if an investor client missed out on just those three days.Click image to enlarge

Markets can be unpredictable. But their long-term trend has been up. Remember that the S&P 500 Index has finished the year in positive territory 74% of the time since its inception in 1926. Investors who are guided by advisors—and stick to their plans—are likely to benefit.

Statistically, the average stock-fund investor’s inclination to buy high and sell low cost them 2.02% annually in the 36-year period from 1984–2020. We believe there is good value in an advisor’s hard-but-simple task of helping clients stick to their long-term financial plan.

C is for customized client experience

If someone wanted a cookie-cutter, one-size-fits-all investing experience—at very little cost—they could use a robo-advisor. Robo-advisors generally don’t provide a financial plan, ongoing service, or guidance. In most cases, they just give the investor the option of choosing from a pre-selected list of funds, provide annual statements and a phone number to call in case of questions.

Now consider this: A lot of advisors have historically anchored their value on investment management—on the skills they bring around asset allocation, security selection and portfolio construction. But, as we just shared, robos do this, too—and typically for a much lower (and on average, declining) fee. Is anchoring your value on the one part of your service model that risks becoming commoditized really the best strategic decision for your business? It will be hard to justify a 1% fee for something an investor can get elsewhere for much less in many cases.

We also recognize that an advisor’s role has changed in recent years. At one time, an advisor was essentially a broker—selecting investments for clients. Now, most advisors are expected to provide holistic wealth advice for entire families. Indeed, between 2017 and the end of 2020, there has been a 39% increase in advisors delivering comprehensive planning services.2

We have found that the value that advisors deliver through the customized experience is much higher than the cost of an automated service and cookie-cutter plan from a robo-advisor.

P is for product alignment with goals

How can you provide a customized experience for each client? It seems there’s not enough hours in the day—or the year.

This is where the use of models can really help you free up time, while still ensuring each of your clients gets the customized client experience they value.

For example, you could choose a core investment strategy for all of your clients—the strategy in which you have the deepest conviction and the broadest knowledge. You could then outsource more specific strategies—such as small cap investments, or international investments, or high yield fixed income—and include a selection of those strategies in your client portfolios. Or, you could outsource the tax management of the strategies to a firm that dedicates time and expertise to creating products that provide clients with the best possible tax profile.

The time you would have spent researching stocks, meeting portfolio managers and analysts, tracking those stocks, documenting trades and conducting ongoing research is now available for you to spend time with your top clients—giving them the personalized experience they crave.

A recent study3 has found that by using model strategies, a financial advisor could save 7.7 hours a week. Multiply that by the number of weeks worked in a year and you end up with an extra 385 hours—time you could spend deepening your relationship with your top clients.

1 Source: https://static.twentyoverten.com/5e0f642709752828dbb0c6e0/-mjyNOiwG/Outsourcing-Money-Management-article4.pdf, AssetMark, 2019. Accessed on Feb 3, 2021. Assumptions: Advisor outsources 50-89% of AUM. Advisor works 50 weeks per year.

T is for tax-smart investing

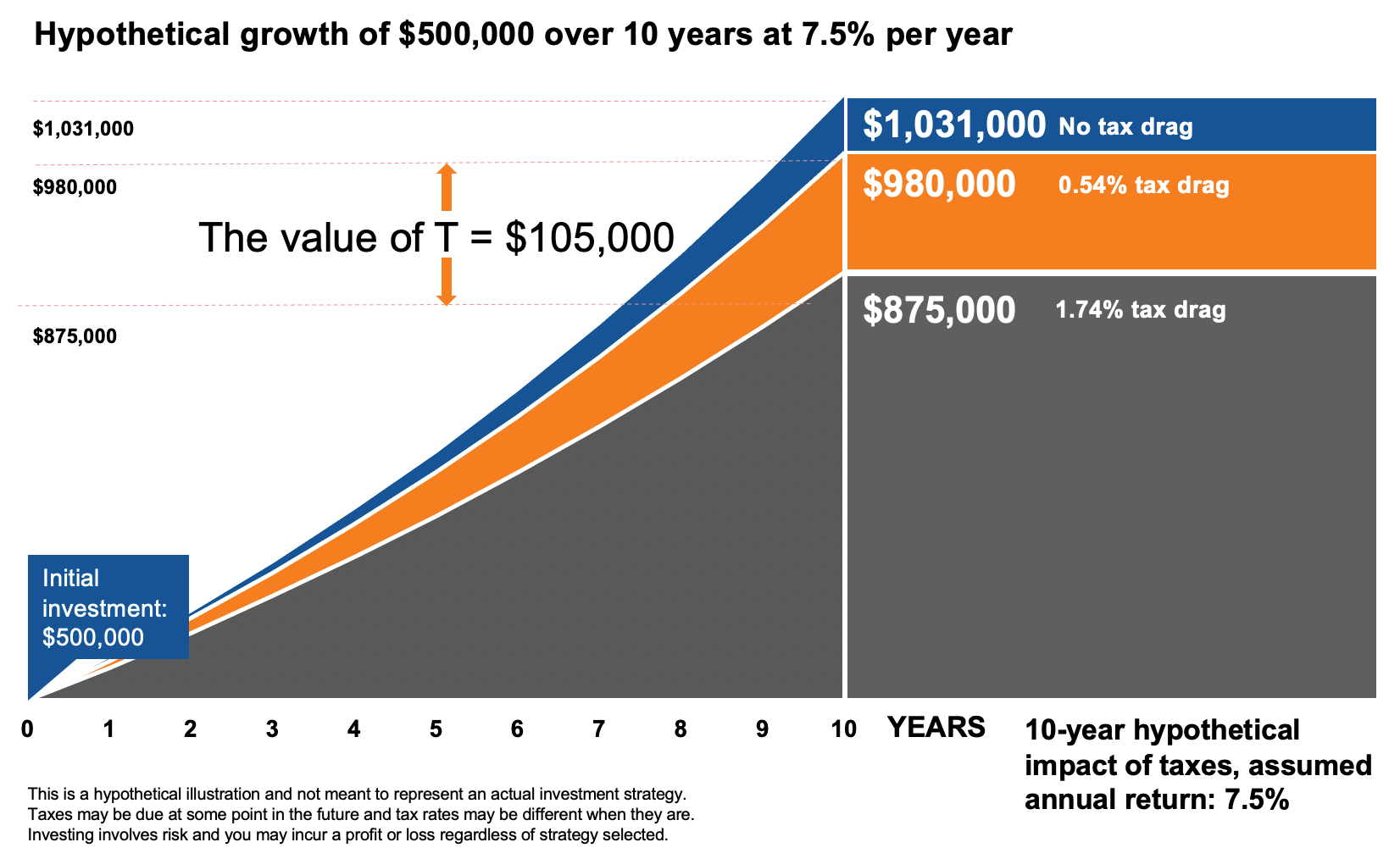

Why should we be concerned about tax management? Because taxes can have a significant impact on returns. Our research has shown that investors lost an average of 1.74% of their return from non-tax managed U.S. equity products in each of the five years ending December 31, 2020. Just that number is larger than the total fee most advisors charge.

More importantly, over time, that kind of tax drag can add up. For example, a $500,000 investment that lost 1.74% annually to taxes would only be worth $875,000 in 10 years, assuming a 7.5% average annual return. But that same investment with no tax drag would be worth $1.03 million.

Click image to enlarge

A tax-managed approach to investing can not only give your clients more money to work with and further invest. It can help differentiate your practice.

As we emerge from the global pandemic, the next issue we may have to face is how to pay for the historic government stimulus packages that kept the economy afloat in 2020. That stimulus added more than $3 trillion to our country’s total debt. With that in mind, it seems likely that taxes are only going to go up over time.

So don’t wait to get tax-smart. Now more than ever, using a tax-managed approach can potentially provide significant value to your clients and help you stand out from your peers.

The bottom line: Communicate your value

What a year. On top of everything else 2020 threw at us, it put many investors’ life savings at stake. We’re grateful that advisors were on the frontlines, guiding investors through the many pitfalls. Our research makes us strongly believe that advisors have never been more valuable.

Advisors, stand tall. We believe in your value. We see your commitment. You’ve never mattered more.

1 Source: Russell Investments, Morningstar Direct. Based on monthly mutual fund, passive ETF flows, Russell 300 Index

2 Source: https://www.envestnet.com/press/envestnet-moneyguides-latest-advisor-survey-find-financial-planning-services-fees-rise

3 Source: https://static.twentyoverten.com/5e0f642709752828dbb0c6e0/-mjyNOiwG/Outsourcing-Money-Management-article4.pdf, AssetMark, 2019. Accessed on Feb 3, 2021