What do bread-making and investing (amid the pandemic) have in common?

Many people confined to their homes during the global pandemic began baking bread to pass the time and reduce the need to purchase groceries. It also was a simple activity to do during a very complicated time. Dough can be made with only three basic ingredients: flour, water and salt. But as bakers worldwide know, what turns it into a golden loaf of bread is the key ingredient: time.

Bread is known as the staff of life, or in simpler terms, as a staple of our diet. As such, it has endured for thousands of years, and over time has taken many forms—from baguettes to bagels, sourdough to rye, bannock to buns, challah to ciabatta.

Three key ingredients

While different types of bread include many additional ingredients (think raisins, seeds, eggs, and so on), all start with the basics of flour, water and salt. Then, taking a standard box loaf as an example, the baker kneads them together into the dough. That mixture is allowed time to rise. The risen dough is often kneaded more than once, deflated, shaped and allowed to rise again. Finally, the dough is placed into the oven, baked and then removed to be enjoyed.

Investing follows a similar process. There are three key ingredients: stocks, bonds and cash, which are the building blocks of a standard asset allocation. The baker—or investment professional—then combines them into an optimal mix, which we will call the balanced portfolio. Other ingredients can be added, such as alternatives or unconstrained fixed income.

The mixture then needs time

Like anxiously waiting for dough to rise it is possible to get impatient with an investment strategy and deviate from your plan. In scary times investors may feel a need to adjust their mix and move to more conservative allocations. In times of strong market performance investors may feel the need to speed things up and lean into high-growth strategies.

But just like fussing with your dough may impede its progress, so will constant changes to your investment portfolio. Left unimpeded, growth can become significant over time.

Now let’s take this concept and apply it to a balanced portfolio.

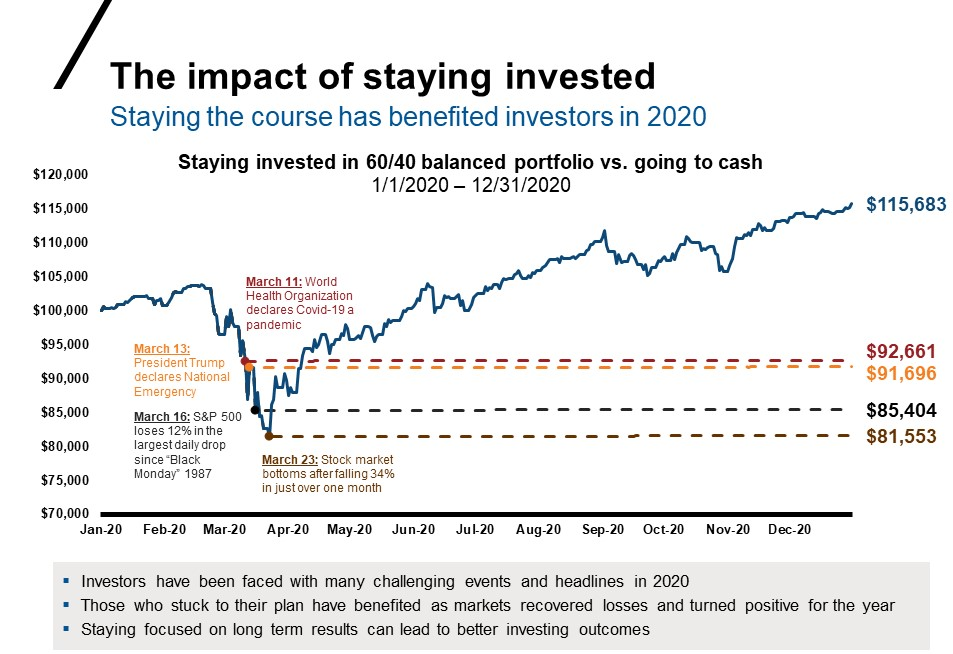

We will start by focusing in on the most recent year, 2020.

A $100,000 investment in a 60/40 balanced portfolio would have grown to more than $115,000.

This gain is achieved despite the fastest 30% drop in the history of the S&P 500 Index between Feb. 20, 2020, and March 23, 2020, because—just as dough deflates during kneading as part of the baking process only to resume its rise—the S&P 500 grew by 39% between March 24, 2020 and June 30, 2020, and continued rising from there.

For investors who moved to cash at or near the lows in March, the outcomes look very different, with ending values significantly lower than their $100,000 initial investment.

Click image to enlarge

Source: Morningstar. 60/40 balanced portfolio: 60% S&P 500 Index + 40% Bloomberg US Aggregate Bond Index; rebalance daily. Cash: ICE BofA US 3 Month Treasury. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

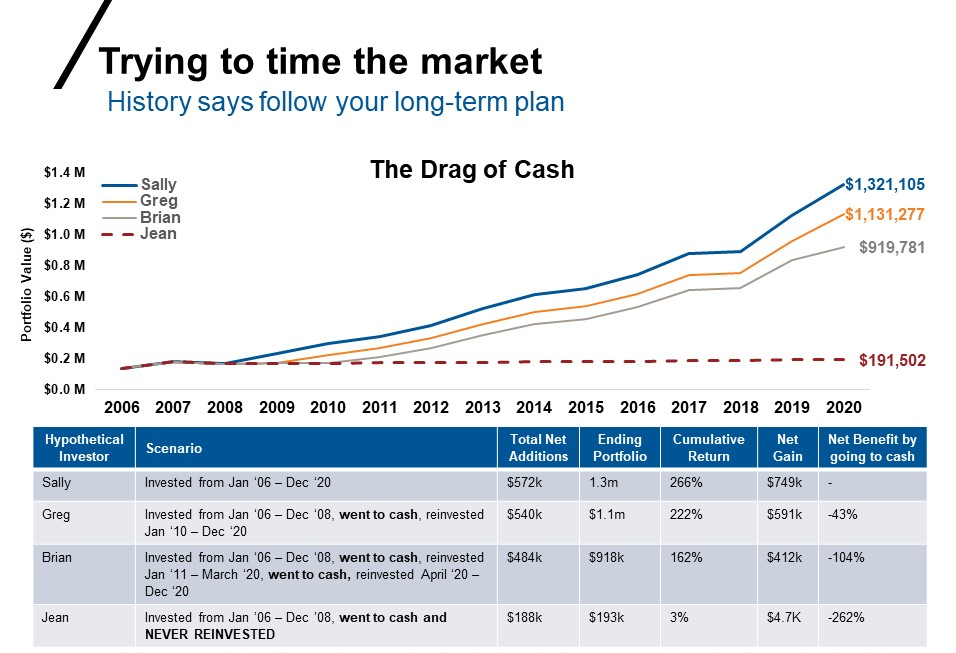

Now let’s step out and take a longer-term view of an investment of $100,000 plus quarterly contributions of $8,000 into a balanced portfolio.

Left to grow untouched over the past 15 years, the portfolio would have grown to greater than $1.3 million.

In contrast, if the investor were to change their strategy along the way again by adjusting their portfolio and moving to cash during the global financial crisis in 2008 (akin to fussing with the dough!), their returns would have been significantly lower.

While investors could have made up some of their lost ground by moving back into their balanced portfolios following periods of recovery, none of the market timing strategies included below would have kept pace with staying invested.

Click image to enlarge

Source: Morningstar Rebalance monthly. Net Benefit by going to cash Net Benefit by going to cash: Cumulative return of Greg, Brian, or Jean minus cumulative return of Sally. Balanced Portfolio: 60% S&P 500 Index, 40% Bloomberg Aggregate Index. Cash: 1.25%.For illustrative purposes only.

The bottom line

In both cases short and long, investors would be well served to look to our friends the bakers, who don’t fuss with their dough and remain invested with their goals in mind.

While the goals may differ—for bakers, it may be a warm, beautiful golden loaf they can enjoy and share with their loved ones, while for investors, it could be funding a child’s college education, gifting to charity or a safe, secure retirement spent with friends and family—in both cases, time remains a critical ingredient in achieving the desired outcomes.