An oldie but a goodie: The global balanced portfolio

In hosting a recent virtual study group with a few select advisors, one advisor kept having to leave the discussion because she had so many Amazon packages being delivered. Another kept having to excuse himself because the show his kids were watching on Netflix was playing too loudly in the background. This sparked a discussion among all of us about the influence that these tech companies have—both in our current lives and in markets. We all agreed that it’s remarkable how a handful of large companies can consume our attention spans and wallets to such a degree.

This conversation isn’t new; it usually comes up after periods of market volatility. When the S&P 500 continuously goes up, advisors tell me their clients are happy investing into the market through a passive index fund. But when markets go down, some clients start asking for defensive, actively managed strategies that look for opportunities outside of the U.S. to potentially lower risk.

My colleague Joe McNally explored this topic in a previous blog, You can't retire on a benchmark. Joe examined the challenges our industry has created by focusing too much on benchmark returns—and in this case, one focused on the 500 largest publicly traded U.S. companies—versus helping clients reach their desired outcomes.

Concentrated line-up

Let’s look at the risk present in chasing the S&P 500 index because of the concentration of a few large companies.

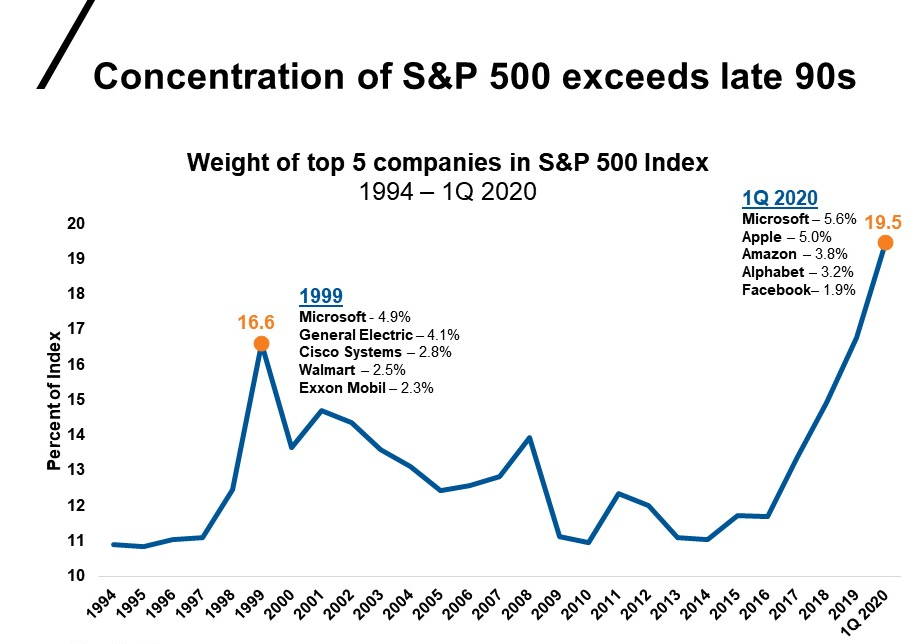

Click image to enlarge

Source: Factset

Weights based on year end values

Alphabet represents both A&C share classes

As illustrated in the chart below, the top five capital-weighted stocks in the S&P 500 today now represent around 20% of the market cap. The last time the top five stocks had this type of capital weighting was in 1999 at about 18%—before the tech bubble burst. Microsoft is the only stock still represented in this statistic 20 years later.

Not surprisingly, the question many investors face today has become: Are you paying too much for the remaining 495 stocks you own? If a small concentration of stocks represents 20% of the index 20 years later, do you carry the risk of owning more losers along with the winners over the long haul?

As the market cap weighting increases in the S&P 500, the narrow leadership of growth drives most market returns. The potential risk in a client’s portfolio is the market volatility resulting from the top five stocks representing 20% of the market selling off. That’s adding insult to injury.

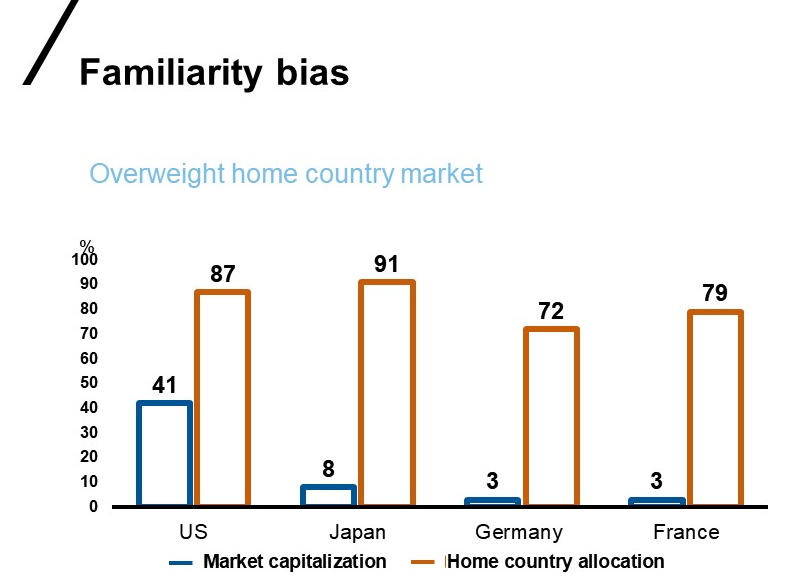

Getting too familiar: Buying what you know

Humans prefer what is familiar or well-known. Since sheltering-in-place, many of us may be using more Amazon and Apple products. The same holds true for investing: many investors prefer stocks based in their own country. This home-country bias may show up well in our investment portfolios.

While investors may be familiar with the products a company provides, they may be less familiar with the investment fundamentals of the stocks themselves. For example, the market capitalization of Amazon is $1.2 trillion, with a trailing price to earnings (P/E) ratio of 115.1 Apple's market capitalization is $1.3 trillion with a P/E ratio of 25.2

Moreover, home-country bias limits the amount of diversification in investor portfolios and exposes investors to significant country-specific risk. Investors who diversify their portfolios tend to represent global market capitalization better.

Click image to enlarge

Source: Market capitalization of domestic listed companies (2017, in current USD)---World Bank https://data.worldbank.org/indicator/CM.MKT.LCAP.CD?view=map Accessed on May 15, 2019. Home country equity allocation—John R. Nofsinger, The Psychology of Investing, Fifth Edition, Pearson, 2014, p. 89.

The case for the balanced portfolio

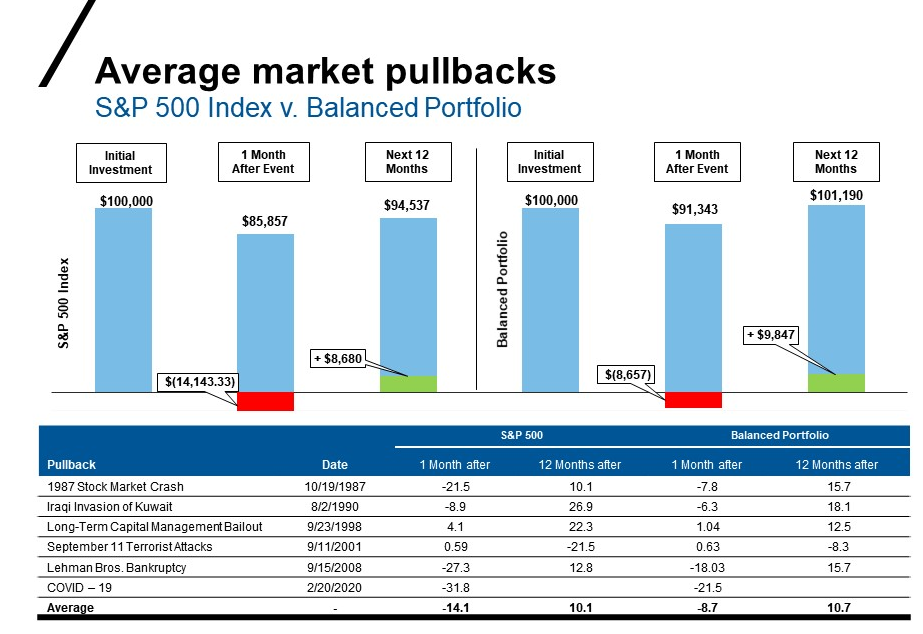

An advisor I work with frequently shares an example of two types of investors. One investor chases the S&P 500 market returns, both up and down. The other investor is in a diversified portfolio, focused on the long-term and not moved by short-term market moments. Let’s look at these two investors’ hypothetical $100,000 portfolios over time (see below). By taking the average return one month after a market-moving event, the balanced-portfolio investor only loses $8,657, relative to the S&P 500 losing $14,143. If you then take the average return starting one month after the event, a balanced portfolio actually gains $9,847, relative to $8,680 gained by the S&P 500. This leads to a balanced portfolio holding up much better during negative market events, while also gaining more, given its diversification.

Click image to enlarge

Source: Morningstar Direct – S&P 500 Index, Balanced Portfolio - BBgBarc US Agg Bond TR USD 40%FTSE Nareit Equity REITs TR USD 10/19/1987-2/18/2005 then FTSE EPRA Nareit Developed NR USD 2/18/2005-3/31/2020 4% MSCI EAFE NR USD 17% Russell 1000 TR USD 34% Russell 2000 TR USD 5%. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

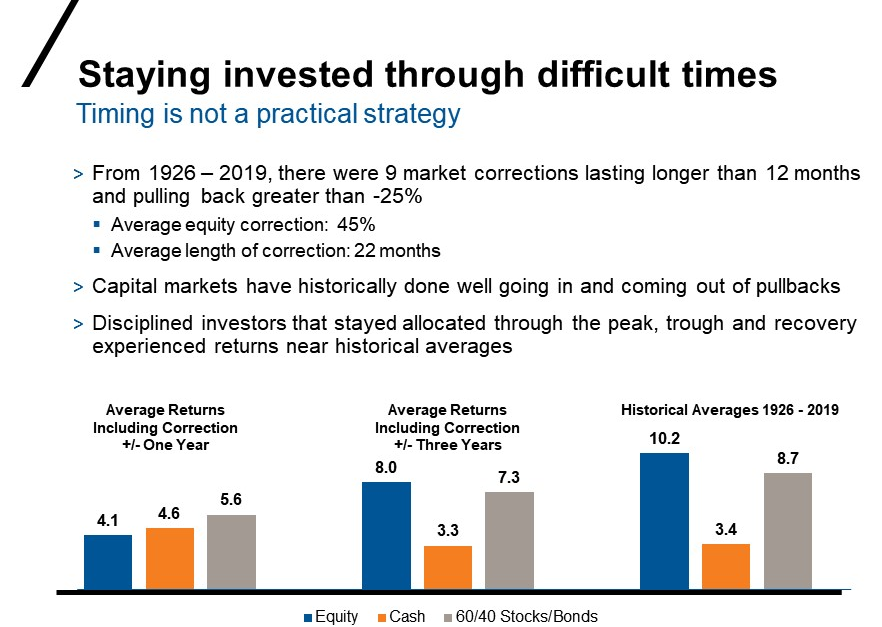

Staying invested

A balanced portfolio over time can help smooth out the investment experience. As you can see from the exhibit below of historical averages from 1926-2019, a balanced 60/40 global stock/bond portfolio has provided competitive returns for investors who stay invested during turbulent markets.

Click image to enlarge

Source: US Equity: Ibbotson 1926 – 1978, Russell 3000 Index 1979-2019, Fixed Income: Ibbotson 1926 – 1978, Bloomberg Aggregate Index 1979-2019, Cash: Ibbotson 1926 – 1978, Citigroup 1- 3 Month T-bill Index 1979-2019 Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

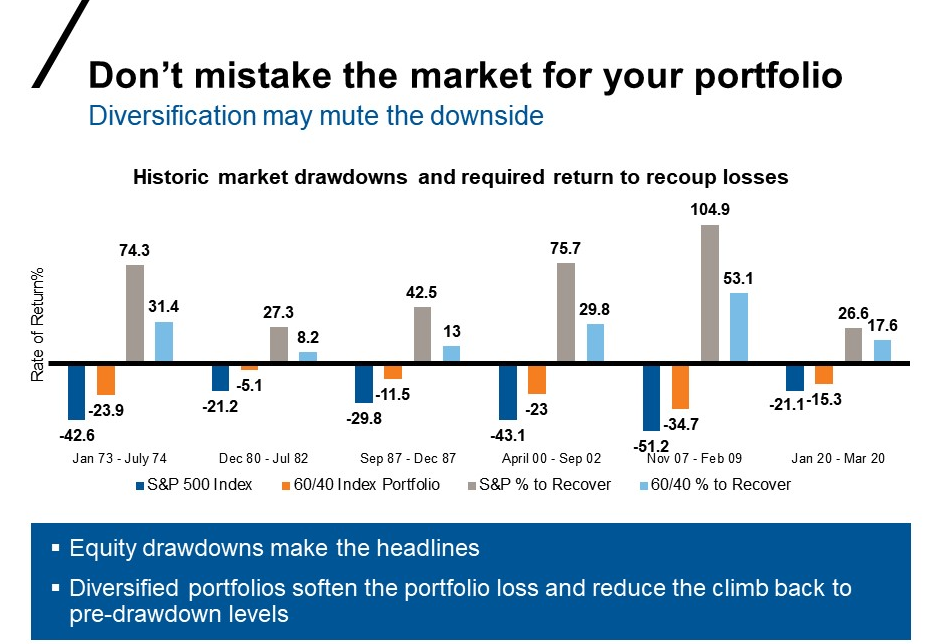

Diversification may mute the downside

When the market (as measured by the S&P 500 Index) went down 21% between January and March of this year, it was the drop that made the headlines. During the same period, a balanced portfolio was down 15.3%, as shown below. We all desire the market returns when things are going up, but not on the way down. A more diversified portfolio may help reduce the downside risk—and resulting pain—during historic drawdown periods.

Click image to enlarge

60/40 Index Portfolio: 60% MSCI World Index/ 40% Bloomberg Aggregate Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

The bottom line

As financial markets remain unpredictable, a trusted financial professional can help:

- Provide education on potential biases that may be affecting investment decisions

- Create a process that considers an investor’s goals, circumstances and preferences to keep them focused on long-term outcomes

During these uncertain times, helping clients appreciate an oldie but a goodie—the balanced portfolio—while also objectively recognizing biases that could lead to poor investment decisions are tasks paramount to an advisor’s role. And that’s why we believe advisors have arguably never been more vital than today.

1 Yahoo Finance as of 28 May 2020

2Yahoo Finance as of 28 May 2020