T is for tax-smart planning and investing: the value of considering the impact of taxes on investments

Would you willingly pay higher taxes on your income? Silly question, right? Nobody wants to pay more taxes than they have to. And yet, thousands of people do so every year.

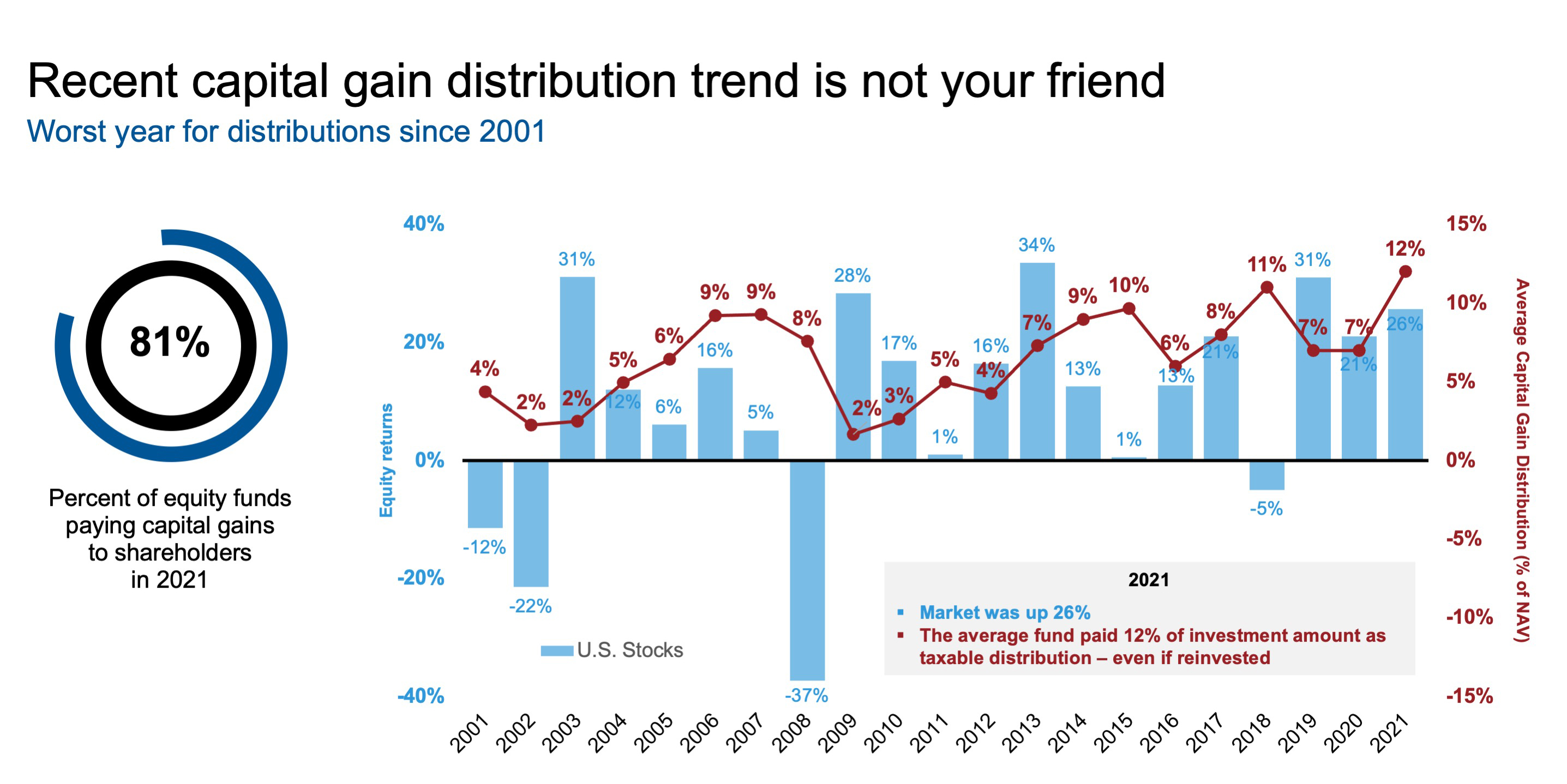

I'm talking about the taxes that investors pay on distributions from their holdings. These taxes can be the biggest fee that investors pay—and 2021 was a banner year in that regard. According to Morningstar, 81% of U.S. equity funds paid a capital gain distribution last year, with the average distribution at 12% of net asset value (NAV). That was the highest level in 20 years! Those distributions are taxable and can result in a hefty tax bill.

This is why T—for being a tax-smart advisor—is the fourth letter in our annual Value of Advisor study. We believe advisors who can help their clients avoid unnecessary taxes can add substantial value.

Value of an Advisor = A+B+C+T

This is the last blog doing a deeper dive into one of the letters in our easy-to-remember formula: A+B+C+T. Earlier we discussed the other components of an advisor's value: the active rebalancing to keep a client portfolio on track, the behavior coaching to help avoid knee-jerk reactions to market volatility and the customized wealth planning that families now require.

This blog will look at the value of being a tax-smart advisor. Advisors who consider the impact of taxes throughout the investment process can help their clients achieve potentially greater returns by reducing the bite that taxes take.

Let’s start by looking at the impact of managing taxes on distributions. As you can see from the illustration below, distributions are a constant in good or bad market environments. Without proper tax management, investors could face substantial tax bills on those distributions.

Source: Morningstar. U.S. Stocks: Russell 3000® Index. U.S. equity funds: Morningstar broad category ‘US Equity’ which includes mutual funds and ETFs (and multiple share classes).

For years 2001 through 2020 % = calendar year cap gain distribution ÷ year-end NAV, 2021 % = cap gain distribution ÷ respective pre-distribution NAV. For years 2001 through 2013, used oldest share class. 2014 forward includes all share classes. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. As of December 31, 2021.

Capital gains: When being below average is a good thing

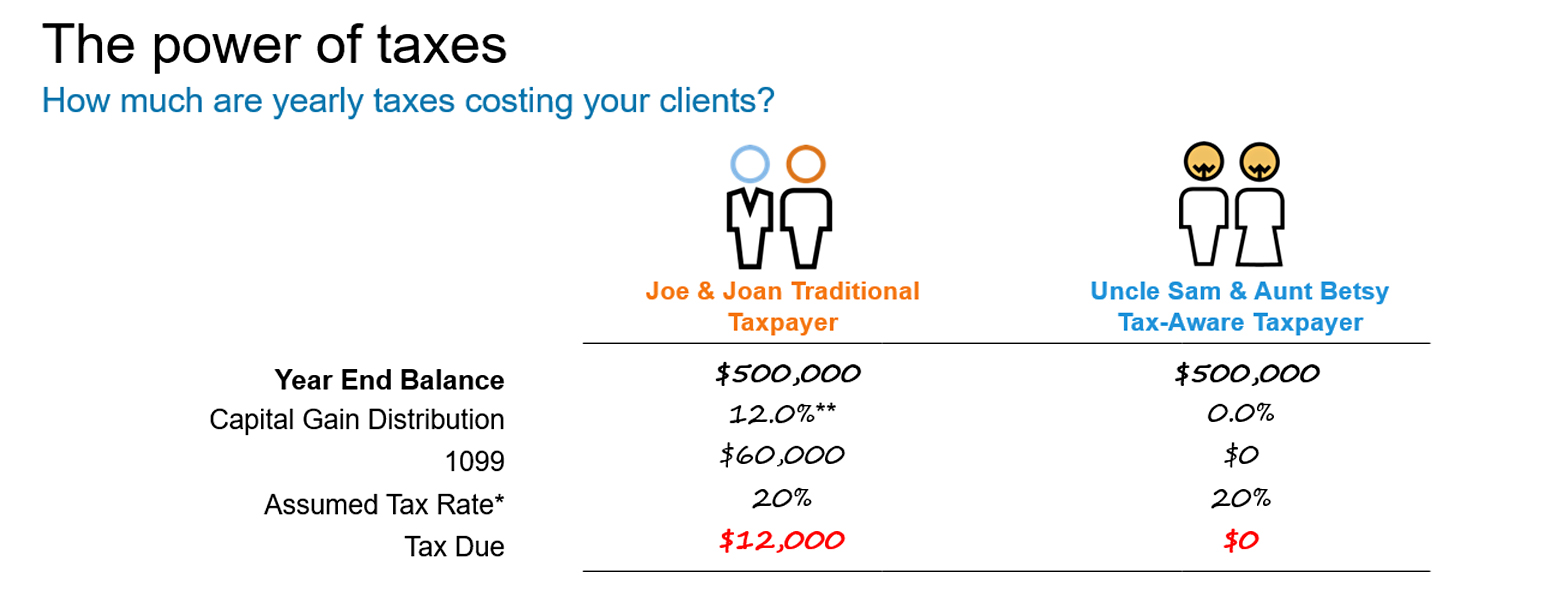

For example, if a portfolio worth $500,000 at the end of 2021 received the average capital gain distribution of 12%, the investor would likely receive a Form 1099-DIV with $60,000 in capital gains distributions. (This assumes a 20% tax rate, which is the top long-term capital gains tax rate at the federal level.) That will result in a tax bill of $12,000. That’s a big check to write to Uncle Sam.

However, if that same investor had held tax-managed mutual funds in that portfolio, it’s possible they would have received no capital gains distribution in 2021. That would mean the Form 1099-DIV would be zero. And the tax bill? Also zero.

How would your clients react when they realize your advice helped them keep potentially thousands of dollars they would otherwise have paid to the government? Do you see why tax management is such an important component to an advisor’s value?

Click image to enlarge

A Hypothetical Illustration

*20%: Represents top long term cap gains rate, excluding 3.8% Net Investment Income Tax. **12%: Represents 2021 average capital gain distribution % of Morningstar broad category ‘US Equity’ which includes mutual funds and ETFs.

Leveraging your client’s Form 1099-DIV to uncover opportunities

You don’t have to be a tax expert to be a tax-smart advisor. For example, you can walk your clients through the Form 1099-DIV to help them connect the dots between what they make and what they actually keep. On their own, clients are unlikely to understand the impact of distributions on their total wealth return. You, the advisor, can reveal what they may be sacrificing to taxes. And better yet, you can do something about it. Adopting a tax-managed approach may allow you to help your clients lower their tax bill between one year and the next.

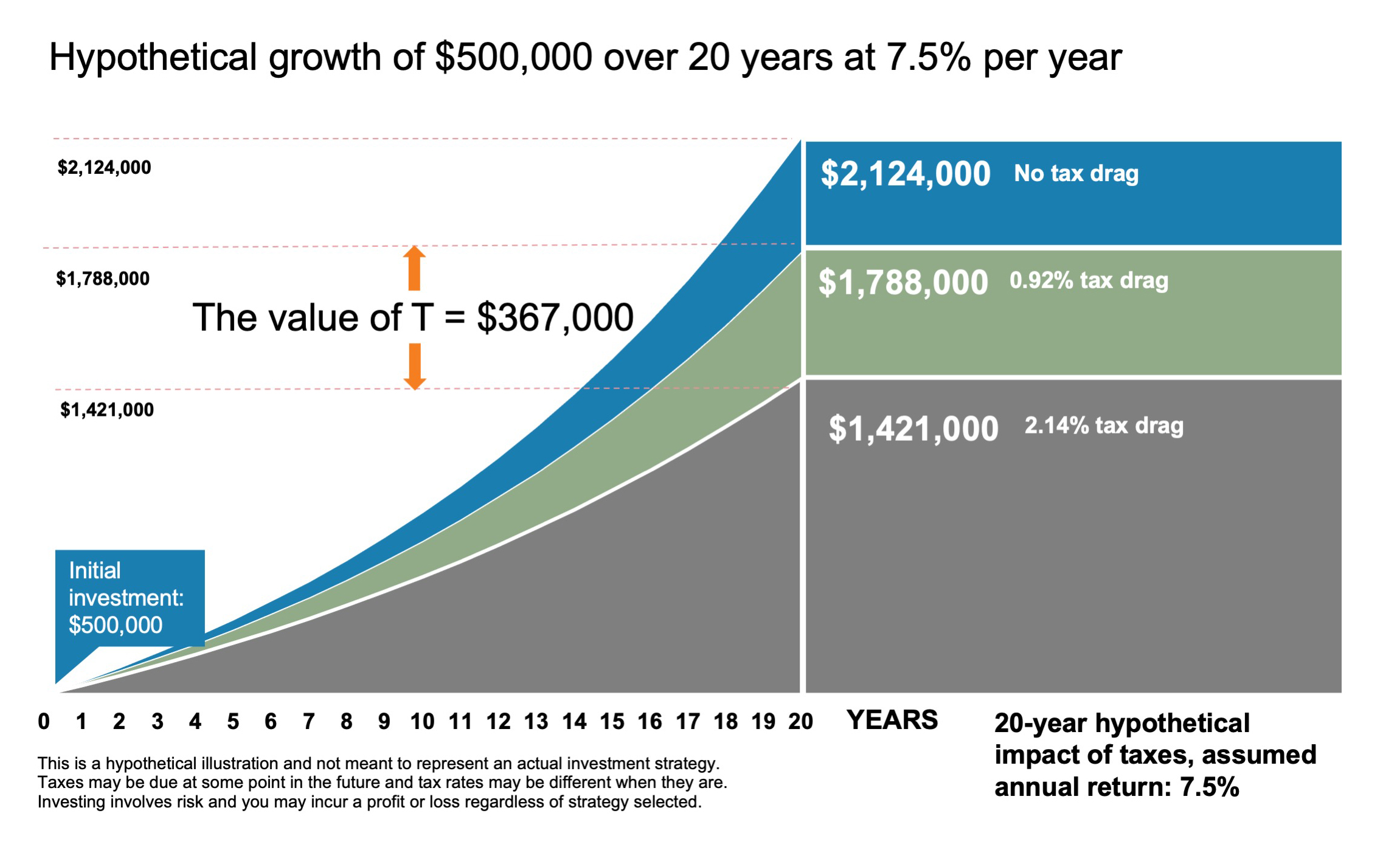

Our research shows that investors who don’t hold tax-managed mutual funds lost an average of 2.14% of their return from U.S. equity products in each of the five years ending Dec. 31, 2021—because of taxes. However, an investor who held tax-managed U.S. equity funds would have felt a tax drag of only 0.92%—a difference of 1.22%. That was the difference in return between non-tax managed U.S. equity funds and tax-managed U.S. equity funds. That return difference could be larger than the fee you charge your clients.

When to do tax loss harvesting?

Five-figure tax bills aside, continually facing large taxable distributions can have a material impact on the long-term wealth of investors. Therefore, we at Russell Investments believe taxes can be managed—through active tax-loss harvesting (not just once a year) to minimize short-term and long-term capital gain distributions, minimizing wash sales, managing holding periods and focusing on qualified versus non-qualified dividend distributions. These tools can help lower tax liabilities today and allow that money to remain in the portfolio to potentially grow in the future.

Tax drag: seeing is believing

The next chart shows the difference in portfolio growth when tax drag is removed.

Click image to enlarge

Our tax impact comparison tool, which uses Morningstar data, is a great way to assess the impact taxes have on investment returns to help make informed decisions for taxable accounts. Imagine being able to show investors the magnitude of this hidden expense ratio. This tool shows the amount of return lost to taxes (tax-cost ratio), after-tax return and pre-tax return, as well as their percentile rank within a peer universe.

We work with and educate many advisors on how to demonstrate the magnitude of tax drag on a portfolio to both clients and prospects. Making the evaluation of tax-managed investing easier can help these discussions be more compelling.

The bottom line

Taxes can be a major headwind for taxable investors. The good news is that the impact of taxes on investment portfolios can be managed intentionally, reaping potential benefits for investors and advisors alike. Helping your clients benefit from techniques like tax-loss harvesting or helping them mitigate the impact of taxable distributions can help set you apart from your peers. Seizing these opportunities during this period of uncertainty and volatility can help provide your clients and you with the confidence that you are helping them grow their after-tax wealth.

Amid market volatility, an economic downturn, higher inflation and political uncertainty, today’s investing environment is one of the most challenging of our lifetimes. At Russell Investments, we believe the role advisors play has never been more vital. When else have investors had a greater need of a counselor and guide to help them navigate these issues? This annual Value of an Advisor study quantifies that dedication and the resulting benefit.

Capital gains distributions happen in good markets, flat markets and bad markets. No one likes losing money AND then paying taxes on top of that. We don’t know how 2022 is going end up market-wise, but being a tax-smart advisor involves many things and one of them is not adding insult to injury for your clients. 2022 may be one of those years, so it may be prudent to be ready.