What do those Amazon boxes have to do with your clients’ Form 1099-DIV?

One of the more trivial things that I have noticed over the past two years is the sheer number of Amazon boxes being delivered in my neighborhood and specifically to my house. Every time I see the truck pull up, I’m always wondering now, who is that box for and what could possibly fit in that box? I’ve also come to learn that with five lovely ladies in my household, very rarely are these Amazon boxes for me.

Why do I tell this story about boxes being delivered to my house that are almost never for me? Well, it is tax season, and your client base has been receiving the litany of different tax forms recently. If they’re like me, they’ve put all those forms in a manila folder or shoe box and have already forgotten about them. Well, if your clients have investment accounts, they’ve received Form 1099-DIV (among a host of other forms).There are LOTS of boxes on these tax forms, but today I want to unpack the essential few boxes that really should matter to you and your clients. These boxes on Form 1099-DIV are analogous to those Amazon boxes that are actually for me—and you can bet I pay attention to them. We think you should do the same with these four boxes on your clients’ Form 1099-DIV.

How to help clients with investment taxes

Alright, let’s look at the four boxes that matter, and they matter A LOT.

Click image to enlarge

Box 1a: Total ordinary dividends – Not as simple to apply a single rate to the dollar ($$) amount, because this box contains both types of dividends, some at the lower rate AND some at the higher rate (see bullets below)

- Includes qualified dividends (lower rate) AND non-qualified dividends (higher rate)

- Includes net short-term capital gain distributions from mutual funds and/or REITs (higher rate)

- Includes taxable interest income from mutual funds (higher rate)

Box 1b: Qualified dividends – Generally, lower tax rate for qualified dividends

- Dividends paid by a U.S. company or qualifying foreign company

- Not all foreign dividends are qualified

Box 2a: Total capital gain distributions – Mostly long-term capital gain distributions which are taxed at the lower tax-rate

- Net long-term capital gain distributions from mutual funds or REITs

Box 12: Exempt-interest dividends – Generally, tax-free at the federal level

- Interest income from municipal bond funds.

Box 1a – Box 1b = Non-qualified dividends – Taxed as ordinary income and often a higher corresponding tax rate

- Includes interest income and dividends from REITs

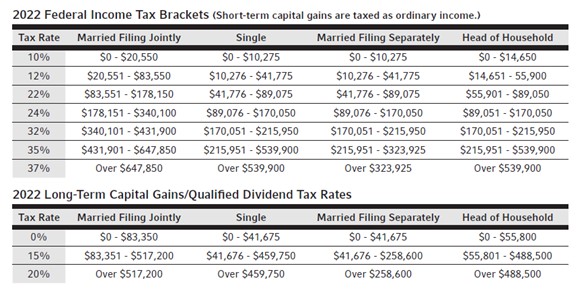

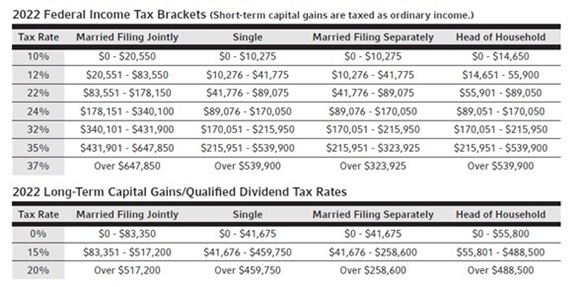

Why do these boxes matter SO much? Well, any $$ amounts in these boxes force an investor to apply different tax rates: not all investment return is treated/taxed equally in the eyes of the IRS. What do I mean? Let’s say one of your clients is Joe & Joan Traditional Taxpayer and they collectively report income of $400,000 in 2021. That puts them in the:

- 35.8% marginal tax bracket (32% + 3.8% NIIT*)

- 18.8% long-term capital gains/qualified dividend bracket (15% + 3.8% NIIT)

You may say, it’s just math—so, what’s the math?

- $$ numbers in Box 1a = Total ordinary dividends (typically equity dividends and interest income from bonds/money markets/CDs/etc.)

- $$ number in Box 1b = Qualified dividends

- Joe & Joan apply the 18.8% rate to that raw $$ number

- Subtracting the $$ numbers in Box 1b from the $$ numbers in Box 1a = your total non-qualified dividends

- Joe & Joan apply that 35.8% rate to that raw $$ number

- $$ number in Box 2a = Total capital gain distribution (whether you actual sold your investment positions or not)

- Joe & Joan apply the 18.8% rate to that raw $$ number

- $$ number in Box 12 = Exempt-interest dividends

- Joe & Joan typically apply the 0% tax rate to that raw $$ number

Maybe your client isn’t Joe & Joan Traditional Taxpayer. Well, take their situation and their income and look where they fall on this chart ... use those tax rate percentages instead. Russell Investments has a handy guide you can use to help your clients find the tax rates that apply to them.

Click image to enlarge

Source: Internal Revenue ServiceAs many dads can probably relate, if I ever want to cue my 14-year daughter’s infamous eye-roll, I’ll use one of my many sayings. One of my favorites that applies here is: Details matter, and they matter A LOT! Here’s another saying for this audience: Unless it says tax-managed, then it’s not being managed for taxes!

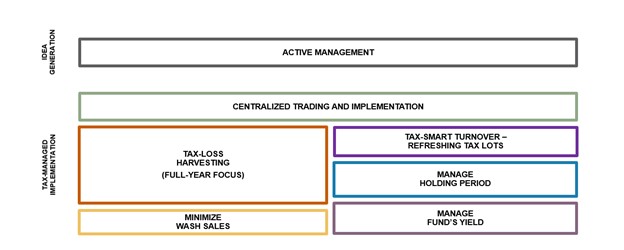

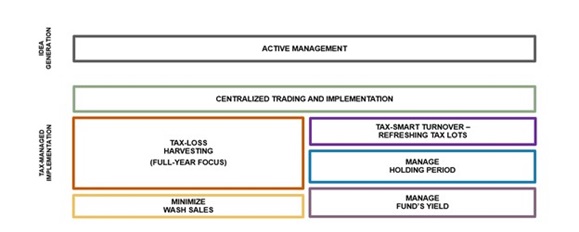

The reality is almost every investment product only solves for one side of the algebra equation. Their sole focus is generating return. They let the investor figure out the taxes later. Later means more than four months AFTER their year-end investment statement. They’re not focusing on all the many intricacies that are involved in tax management. The chart below shows a few of the factors a true tax-managed solution will consider:

Click image to enlarge

Source: Russell Investments. For illustrative use only.At Russell Investments we believe to solve the proverbial algebra equation you must solve for both sides of the equation: return and taxes.

In focusing the total portfolio on tax-management AND using the many tax-management techniques over the full calendar year, those details add up. What do I mean?

Check out our 1099 Guide and compare the vastly different tax outcomes between Joe & Joan Traditional Taxpayer and Uncle Sam & Aunt Betsy Tax-Aware Taxpayer.

The bottom line

The real question is: How do Joe & Joan Traditional Taxpayer lose $15,000+ without trying? Answer: By not paying attention to details! Knowing how to calculate if your client is paying too much investment taxes puts you in a better position to help them do something about it. It’s not all about existing clients either: our 1099 Guide could help you win more business from potential prospects and other sources.

In our annual Value of an Advisor study, helping clients reduce the impact of taxes (financial professional login required) is one of the greatest value-adds advisors may bring to the client relationship. Don’t miss this opportunity to turn tax season into a productive relationship and business-building strategy.

So, the next time those Amazon boxes show up on your front porch OR you’re helping your client sort through those many boxes on their Form 1099-DIV, remember those four boxes. They matter, and they matter a lot.

*Net Investment Income Tax