A Form 1040 review may help you find ways to improve after-tax wealth

Tax season is over. It’s easy to want to put it to bed and not revisit it until next year. Let’s be honest: most of us don’t ever want to revisit tax season. It’s a little like when a child goes to the doctor for their annual vaccinations: how soon can this be over, and can we never do this again? But prevention is the best form of medicine, as the saying goes. The same can be true for taxes. The time immediately following tax season is the time to analyze and prepare for the next tax season.

How do you do this? Where do you start? During tax season, the best way to analyze what’s going on and where the potential tax problems are in a client portfolio is through the Form 1099. But following tax season, it’s best to look at the total picture and then home in what might need to be addressed. The way to do this is to focus on the Form 1040.

Why start with Form 1040

Looking through an investor’s Form 1040 can yield good insight into investment-related income. There are many other schedules and tax forms related to investment activities (Schedule1, Schedule B, Schedule D, etc.), but at some point, all flow through Form 1040.

Overcoming investor objections

We hear some reservations by financial advisors about asking to see a client’s Form 1040. For most of us, wage and tax information is very personal and we are quite protective of it. But what needs to be kept secret from the investor’s financial advisor? You already know their name and address, marital status, number of children, Social Security number, wage information, as well as other things like property owned, business holdings, etc. There is very little that you, as their financial advisor, don’t already know.

It’s important to explain to the investor that Form 1040 plus other tax documents can help you better fulfil your role as their financial advisor. When it comes to investing for retirement, a thorough understanding of the financial picture is imperative. The chartered professional accountant (CPA) is just that in most cases—an accountant who fills out the form. Your role is to provide advice. You are better placed to do so when you know what might need to be adjusted to help lower their tax bill and improve their after-tax income.

While daunting, and for many of us quite hard to understand, Form 1040—plus a few additional forms and worksheets—provides a complete financial picture of an investor. An extensive review of Form 1040 annually can help uncover recurring events that could have tax implications.

Where to find clues: What to look for when reviewing a tax return

You don’t have to have a degree and career in forensic accounting to discover some useful tax clues. You just need to know where to look, what to look for and how to interpret what you are seeing.

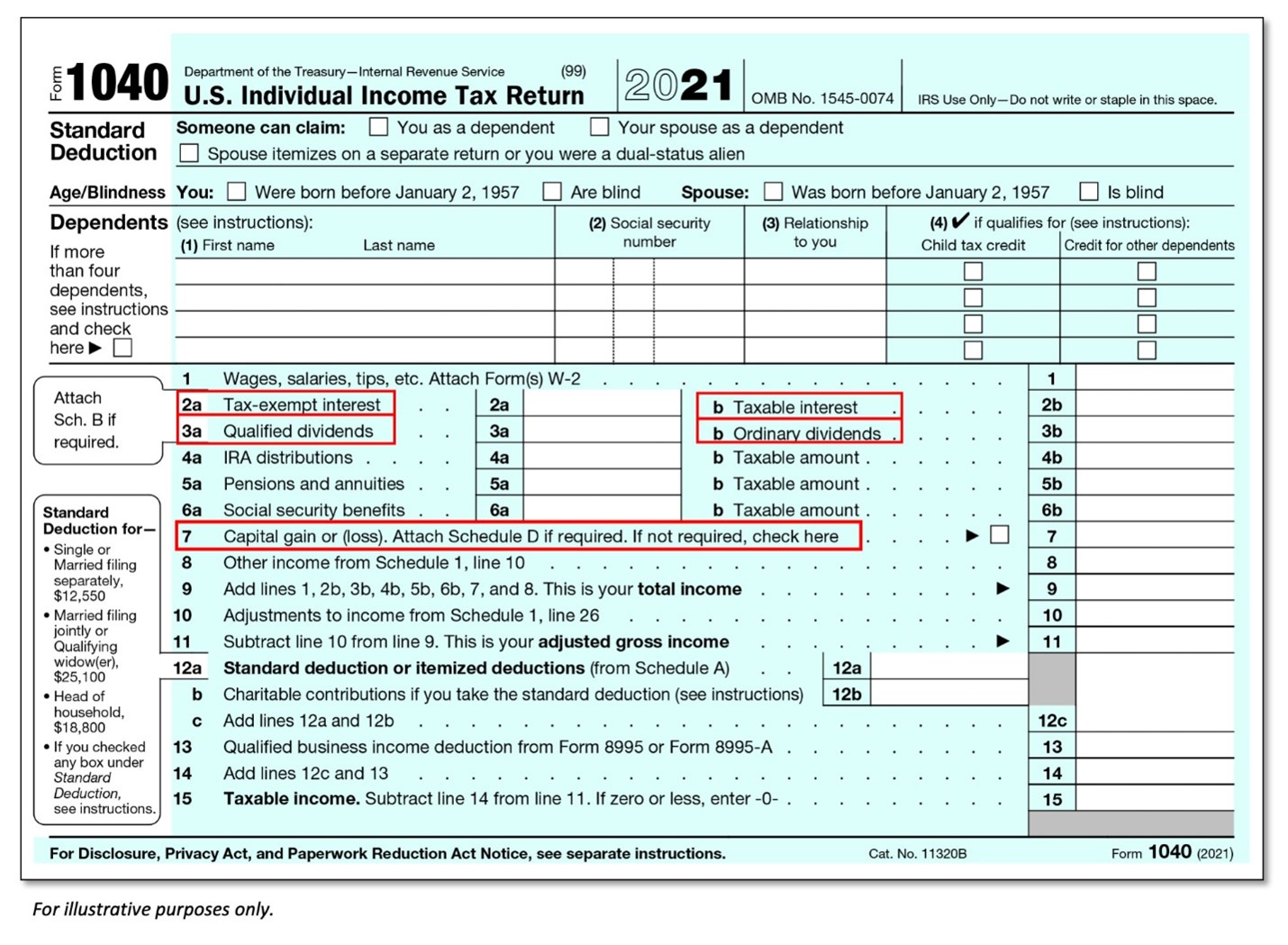

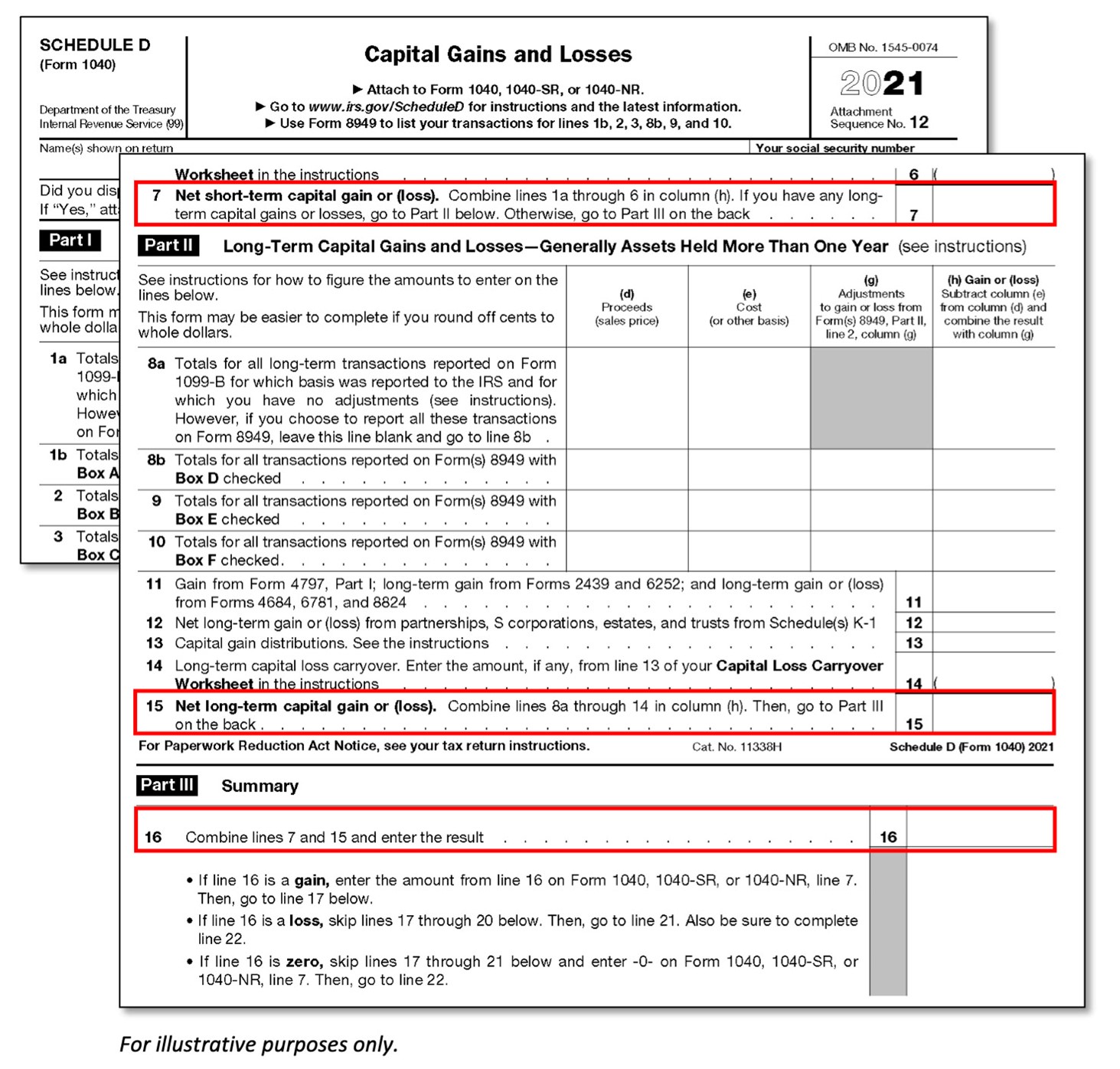

Let’s examine the forms below. We have highlighted in red the key items to look at where clues can be unearthed. Let’s start with Form 1040 and then Schedule D, Capital Gains and Losses. We’ll begin by looking at what Form 1040 can tell you about how much tax the investor is paying, first on interest and then on dividends and capital gains.

Click image to enlarge

Interest: Does the client understand the amount of taxes being paid on interest?

Line 2a: Tax-exempt interest income

- Interest from municipal bonds and municipal bond funds is reported here. This interest is generally tax-free at the federal level.

- If the vast majority of interest is tax-exempt, then things are likely looking good for the taxable investor.

- Line 2b equals the total received from taxable interest income. This includes interest-paying vehicles like savings accounts, CDs, taxable bonds and taxable bond funds. Note that taxable interest is taxed as ordinary income and at the highest marginal tax rate.

- Qualified dividends are generally taxed at the more preferential long-term capital gains (LTCG) tax rate.

- Ordinary dividends are taxed as ordinary income and will generally be taxed at a higher rate vs. qualified dividends. Short-term gains realized by mutual funds are recorded as ordinary dividends.

- The total of all capital gains from Schedule D is reported here. How big is this number overall? How large is this number relative to the investor’s income, and relative to their total portfolio? What is the breakdown of long-term and short-term gains (from Schedule D)?

Line 2b: Taxable interest

Dividends:

Line 3a: Qualified dividends

Line 3b: Ordinary dividends

Capital gains:

Line 7 of Form 1040: Capital gain (or loss)

Line 7 of Schedule D: Short-term capital gain. These are taxed as ordinary income. They should be avoided / minimized.

Line 15 of Schedule D: Long-term capital gain. These are generally taxed at a lower rate than short-term capital gains tax rates.

Line 16 of Schedule D: Total capital gain. This is the investor’s total capital gain realized (Line 7 + Line 15). This schedule feeds Line 7 on Form 1040.

Click image to enlarge

Generally, it’s better to have fewer distributions (such as capital gains, interest and dividends) from your investments. This allows a portfolio to grow at a faster rate.

Many investors, however, rely on distributions from their investments to supplement their income in retirement. In these cases, we believe it’s important to use the information above to better understand if the portfolio’s income is being created in a tax-smart manner.

A quick summary of important questions to consider and answer:

- Does your client feel they paid more in taxes than they should have?

- If interest is generated, is it primarily tax-exempt interest income? Or is there a lot of taxable interest? Taxable interest is taxed as ordinary income.

- Is there dividend income? If yes, is it mostly qualified, or is it a lot of ordinary dividends? Generally, the tax rate is lower for qualified dividends, while ordinary dividends are taxed as ordinary income and often have a higher corresponding tax rate.

- If there is a sizable number of ordinary dividends, what is the source? Is it from mutual fund holdings? If so, those mutual funds might be generating a lot of short-term gains, which are taxed as ordinary income.

- Are there a lot of capital gains? How much of it is generated as short-term capital gains? Short-term capital gains are taxed as ordinary income, as noted above.

With these questions in your back pocket and with the above guide identifying which lines of Form 1040 are important and what they show, you are now better prepared to make more informed after-tax investment decisions.

The bottom line

Doing a review of Form 1040 places you in a bettermuch stronger position to help an investor align their portfolio to their after-tax needs. A quick summary can help you identify any issues regarding investment-related taxes. At the least, it shows the client that you are doing what you can to help them retain more of what they have earned through their investments.