Can financial advisors help with taxes? Yes! Here’s how.

Some of the most successful advisors I know are not the best prospectors or salespeople. Rather, they are very good at finding great opportunities. Through my work with financial advisors over nearly 10 years, I have realized the best opportunities arise when you can genuinely help solve another person's problem.

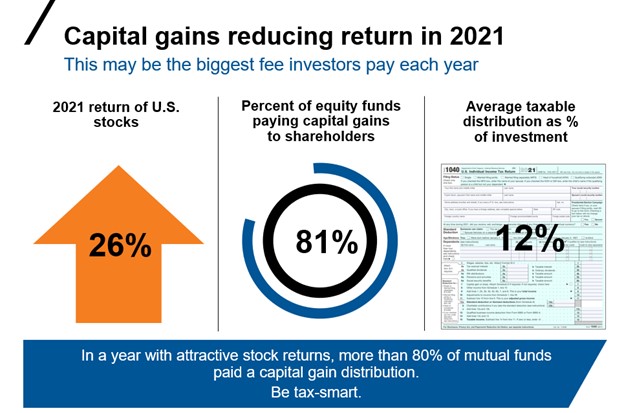

As the regional director for Russell Investments covering north Texas and Oklahoma, I often help advisors conduct client meetings. Since the beginning of the year, I cannot count how many times I've heard clients complain about taxes. It is a real problem for many folks! All the facts and figures we talk about at Russell Investments feel much more real, seeing how frustrated and stressed this has made some individuals I have met. Unfortunately, it doesn't surprise me. In 2021, 81% of equity funds paid a capital gain distribution, with the average distribution at 12% of net asset value (NAV). Those distributions are taxable and can result in a hefty tax bill.

Click image to enlarge

U.S. Stocks Returns =Russell 3000 Index; U.S. equity funds: Morningstar broad category ‘US Equity’ (large/mid/small V/B/G) which includes mutual funds and ETFs (and multiple share classes). Average U.S. equity fund Distribution: Capital Gains/Share (% of NAV) based on Morningstar U.S. OE Mutual Funds and ETFs. % = Calendar Year Cap Gain Distributions / Year-End NAV. Distribution is assumed to be made at last day of year and reinvested.

Potential impact on the investor’s wealth

Stop and think about that for a moment. Think of your mother or a close family member being invested in an equity fund that paid the average capital gain distribution. If their account was valued at $500,000 at the end of the year, they would have received a 1099 Form with $60,0000 in box 2A. At a 15% capital gains tax bracket, the IRS will knock on the door with a tax bill for $9,000. Unless it improves their overall situation, I wouldn't want my mother nor my clients to pay that amount of tax on their investments.

Potential impact on the value of your advice

Many of our clients and prospects are dealing with this problem right now. Almost any client or prospect you talk to would probably let you know they were shocked or unhappy with the tax bill their CPA informed them about recently. The thing is, that tax bill is unnecessary. There are strategies that do not distribute capital gains or are able to minimize distributions. As an advisor, you are able to help potentially solve your clients’ tax problem by approaching them with a tax-managed strategy. I believe there is no better time than right now for an advisor to differentiate themselves through tax planning and tax mitigation strategies, for three reasons.

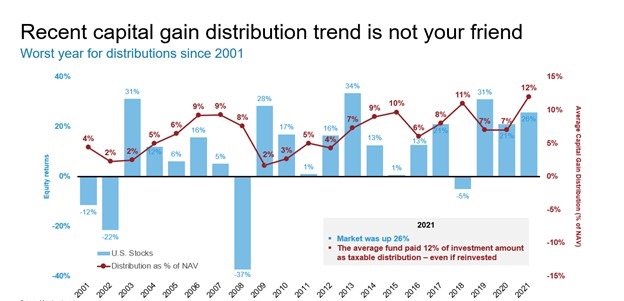

1. My good friend and colleague Tom Flynn says, "Capital gains distributions continue to cause tax bills year after year that either limit our client's returns in the good years or magnify their losses in the bad years." As noted, last year the average capital gains distribution for the industry was 12%. This was the highest average distribution in more than 20 years and topped the 11% average distribution we saw in 2018. However, 2018 and 2021 were completely different regarding the market’s return. 2018 was a year where clients saw a pullback of 5% and still got hit with taxes. However, in 2021, the market was up 26%1 and clients got hit with taxes. My point is that it doesn't matter if the market is up or down; clients continue to get hit with these potentially unnecessary distributions year after year. Suppose you can show a prospect or client a strategy that limits their exposure to distributions like this but doesn't jeopardize their after-tax return. It could be an opportunity for you to differentiate your approach from your competition and help solve the client's problem.

Click image to enlarge

Source: Morningstar

U.S. Stocks: Russell 3000® Index. U.S. equity funds: Morningstar broad category ‘US Equity’ which includes mutual funds and ETFs (and multiple share classes).

For years 2001 through 2020 % = calendar year cap gain distribution ÷ year-end NAV, 2021 % = total cap gain distribution ÷ respective pre-distribution NAV. For years 2001 through 2013, used oldest share class. 2014 forward includes all share classes. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

2. Many advisors tell me most of their assets are qualified and that tax management isn't important to their clients. First, when I hear this, I think there is an opportunity to conduct a re-discovery exercise with their clients and see if things have changed. Second, as you can see below, nearly half of all mutual fund assets are held within taxable accounts. That means there are $11.2 trillion of assets to potentially uncover. The opportunity is more significant than you think! Lastly, think back to conversations with your clients and prospects over the past year. If you heard of someone selling a ranch, rental property, receiving an insurance payout, or selling a business … stop right there! Those could be potential candidates who may benefit from tax-mitigation strategies. My point is that there are a lot of non-qualified assets out there. Instead of fishing on only one side of the pond, why not fish the whole thing!?

Click image to enlarge

Source: 2021 ICI FactBook

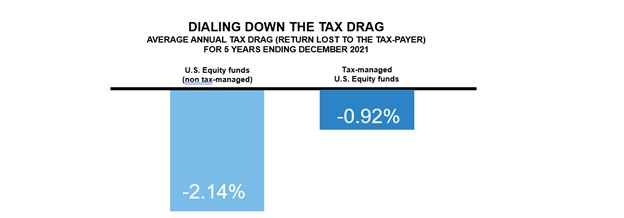

3) Many advisors underestimate the impact that taxes can have on a client's overall net return and net worth. This is because it is not as black and white as other values they may find on their statement. Clients can see their overall return, fees and more, but nowhere on their statements does it show they may have lost more than 2% of their return to taxes. If it did, I probably wouldn't be writing this article on how big an opportunity tax-managed investing is. I think this is one of the most significant areas of opportunities to showcase your value as an advisor. Our research shows that investors who don’t hold tax-managed mutual funds lost an average of 2.14% of their return from U.S. equity products in each of the five years ending Dec. 31, 2021—because of taxes. However, an investor who held tax-managed U.S. equity funds would have felt a tax drag of only 0.92%. That was the difference in return between non-tax-managed U.S. equity funds and tax-managed U.S. equity funds. That is a significant amount of value you could be delivering to your clients as a tax-smart advisor. You should take credit for it and showcase it to prospective clients.

Click image to enlarge

Source: Russell Investments. Tax-managed: funds identified by Morningstar to be tax-managed.

Universe averages*: Created table of all U.S. equity mutual funds and ETFs as reported by Morningstar. Calculated arithmetic average for pre-tax, post-tax return for all shares classes as listed by Morningstar.

Morningstar Categories included: U.S. ETF Large Blend, U.S. ETF Large Growth, U.S. ETF Large Value, U.S. ETF Mid-Cap Blend, U.S. ETF Mid-Cap Growth, U.S. ETF Mid-Cap Value, U.S. ETF Small Blend, U.S. ETF Small Growth, U.S. ETF Small Value, U.S. OE Large Blend, U.S. OE Large Growth, U.S. OE Large Value, U.S. OE Mid-Cap Blend, U.S. OE Mid-Cap Growth, U.S. OE Mid-Cap Value, U.S. OE Small Blend, U.S. OE Small Growth, U.S. OE Small Value.

The bottom line

You don't have to pick up the phone and make a hundred calls a day to find excellent opportunities. Changing your philosophy around managing non-qualified assets and putting processes in place to uncover non-qualified assets could make all the difference. With clients and prospects recently getting hit with the largest distributions in more than 20 years, an $11.2 trillion pool of assets to look for, and managing for taxes only adding to the value you bring to the table as an advisor, why wouldn't you make it a focus this year?!

1 As represented by the Russell 3000 Index