Capital gains – Misconceptions and opportunities

Executive summary:

- With tax season approaching, now may be an ideal time for advisors to discuss capital gains with their clients

- Tax-smart advisors can help dispel misconceptions about capital gains and manage the tax bill on their clients’ portfolios

- Educating clients on taxes can differentiate an advisor from their peers and potentially boost their business

There is no doubt that taxes are complicated. The U.S. tax code, for example, is almost 7,000 pages long. Then throw in all the different tax brackets that exist and the not very user-friendly forms, schedules, worksheets, filing dates, documents, publications and much more. There are a variety of taxes: federal taxes, state taxes and municipal taxes; there are income taxes, investment taxes, sur-taxes, wealth taxes, estate taxes and more. It’s no wonder that some people I know—and I doubt they are alone—barely glance at their tax documents but just hand them over to their accountant to deal with.

This is where you, the advisor, can play a significant role. This is your opportunity. In my view, taxes on investments are one of the most misunderstood aspects of our tax code. And chief among the types of taxes that few investors understand and actively work to minimize are capital gains taxes.

The thing is: you CAN take steps to manage the taxes on an investment portfolio. In fact, our annual Value of an Advisor study has found that advisors who take a tax-smart approach to investing can potentially provide additional value to their clients. After all, the fewer taxes a client pays on their investment portfolio, the greater their potential after-tax wealth.

As your clients are now receiving their 1099-DIV forms for 2022, it may be the ideal time to discuss capital gains with them. It’s likely that many investors saw their investments lose ground in 2022 as both stocks and bonds declined over the year. And it’s just as likely that many will receive a tax bill related to capital gains on that portfolio anyway. Talk about rubbing salt in the wound! While this may be a tricky conversation, that’s precisely why you should bring up the topic. To help avoid such conversations next year, and the next year, and the year after that, and so on ... grab the opportunity now to introduce your clients to tax-managed investing.

The first step may be to educate your clients about capital gains and what they can do about them.

Follow along as I seek to dispel two key misconceptions related to capital gains. And in the process, I am going to give you THREE opportunities that could improve the productivity of your investment practice. You do not need to be an accountant to do this. You just need to know enough to provide valuable advice to your clients. Advice that they are most likely not getting, but really need. Especially with tax season right around the corner.

Misconception #1: “Capital gains are just a byproduct of having positive performance in my portfolio.”

This is probably the most common misconception I hear. Many investors believe that paying capital gains is just part of the investing process, and when gains are paid, that means that they had some winners in their portfolio for which taxes are owed.

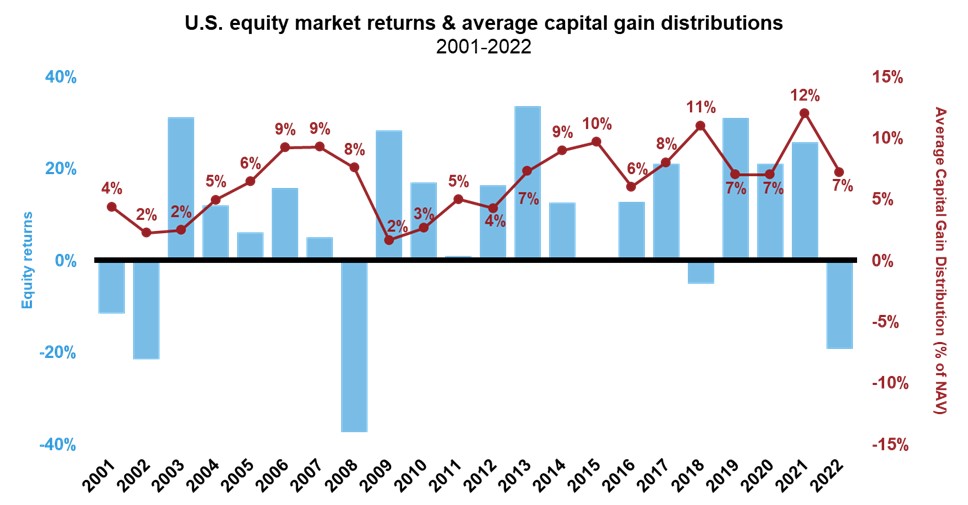

While capital gains are, to some degree, created by positive portfolio performance, the reality is many are driven by portfolio activity. As the chart below shows, in 2018 and most recently in 2022, markets ended the year in negative territory, but many mutual funds and ETFs still distributed capital gains.

Yes, you read that correctly. You can have a portfolio with a negative number on the Dec. 31 statement, but if there is turnover, wash sales, short-term holding periods, dividends/income … then investors are likely to still receive a capital gain distribution on which they will pay taxes. Embedded gains, forced liquidations when we see mass outflows and more can play into this equation. I recommend keeping the conversation simple: “Capital gains are driven by portfolio activity, rather than performance alone.”

For years 2001 through 2020, % = calendar year cap gain distribution ÷ year-end NAV, 2021 & 2022 % = total cap gain distribution ÷ respective pre-distribution NAV. For years 2001 through 2013, used oldest share class. 2014 forward includes all share classes. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Misconception #2: “There’s nothing I can do about taxes, it’s just a part of the process.”

Closely tied to the first misconception, this one comes up often. If you read Russell Investments blog posts and know about our tax-managed process, you know this to be inaccurate. Taxes can, in fact, be managed. We have a phrase we like to use: “Avoiding taxes can land you in jail, managing for taxes is just smart investing.”

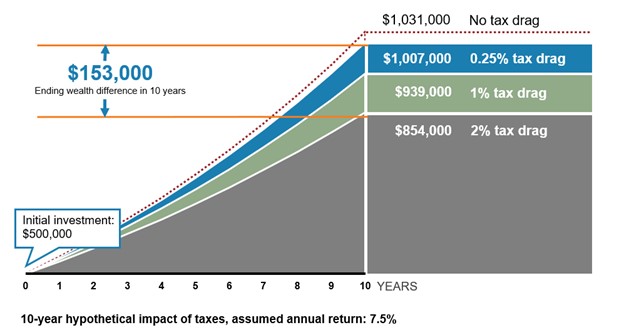

As we’ve just noted, portfolio activity is what drives a good chunk of capital gain distributions and therefore, there are things we can do about them! At Russell Investments, we take a hands-on approach to investing to manage for issues such as: holding periods, turnover and income/dividends, which can contribute to the generation of taxable gains. We also look for tax-loss harvesting opportunities year-round to create what we call tax assets that can be used to offset potential capital gains. In short, we work to actively reduce the tax drag on a portfolio. We define tax drag as the amount of investment return lost to taxes. This means that if your client’s portfolio saw a return of 5% and has a tax drag of 2%, by the time taxes are paid on that account in the spring, they have netted just 3%. Or in a year such as 2022, a -14% return can turn into -16%. When it comes to taxable (non-qualified) accounts, it’s not about what you make, it’s about what you keep.

The after-tax edge

Hypothetical growth of $500,000 over 10 years at 7.5% per year

This is a hypothetical illustration and not meant to represent an actual investment strategy. Tax drag is the reduction of potential investment returns due to taxes. Taxes may be due at some point in the future and tax rates may be different when they are. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

Now let’s turn to the opportunities that these misconceptions can create. At Russell Investments, we are about more than just highlighting and debunking the misconceptions. We focus on how an opportunity can be found and then used to your advantage. Follow along as we highlight THREE key opportunities you can take advantage of to position your advice and planning practice at the forefront of your clients’ minds.

Opportunity # 1: Education

I don’t blame investors for not understanding capital gains. This is a relatively tough concept that can get quite heady. I recommend you keep your conversations on the topic simple, and only take a deeper dive if the client asks for greater understanding. We’ve created two pieces for exactly that reason, which you can use with investors this tax season. Our 1099 Guide is designed to help you connect the dots for your clients between their 1099-DIV form and their investments. We show you how to run the numbers to help your clients better understand how their investments are taxed. The tax season essentials flyer can help you address some of the misconceptions around investment taxes using simple charts and illustrations.

In my experience, what investors want from their advisors is basic education and prudent money management. I feel very strongly that tax consideration is a core tenet of prudent money management. The days of building out a lineup of investments to utilize across all clients’ accounts (qualified and non-qualified) are coming to an end and this brings us to opportunity #2. Many clients balk at an advisory fee or internal expense, but rarely consider what is likely the biggest fee they pay – taxes!

Opportunity #2: Differentiation

Opportunity # 3: Business and asset growth

Of course, being able to provide additional value and education to investors can help attract new business or increase the share of wallet from your existing clients. I sometimes ask investors (and encourage the advisors I work with to do the same), what does your current financial advisor do to manage for taxes? I always get one of two responses: I don’t know or nothing. Either one is a fantastic opportunity for education, differentiation, and therefore, asset gathering. If you, as a financial advisor, can develop a crisp understanding of capital gains and obtain a process and/or strategy to manage them, you just might find a whole new market open up.

If you’d like to learn more about the who, what, why, and how of tax management, please reach out! We’d love to help educate you and your clients and provide guidance on tax-managed investing.