Tax-loss harvesting: Frequency matters

Executive summary:

- Many advisors wait until the end of the year to harvest tax losses, but that may not be the best policy

- Stock markets frequently go up in the last two months of the year so better harvesting opportunities may be available at other times

- When it comes to tax management, every season is tax season

Many of us start off the new year vowing to shed bad habits and take on better ones. I'm hoping to replace the bowl of chips I have after dinner with a bowl of carrot sticks. Here's something a lot easier to accomplish, for those of us in the financial services industry: rather than scrambling at the end of the year to book tax losses for your clients to use against their capital gains in the future, institute a policy to conduct tax-loss harvesting as a regular feature of your portfolio tax management.

And if you're not doing portfolio tax management as a regular feature of your services to your clients, here's another suggestion. The new year is a great time to start!

At Russell Investments, we know that many advisors consider the last few weeks of the year to be tax-loss harvesting season. We know it is a hallmark of their end-of-year financial planning. But we believe every season can be tax-loss harvesting season. There are many benefits to conducting this key tax-management technique all year long.

If you are among the advisors who has waited until December to tax-loss harvest, ask yourself: is there any particular reason you do this at the end of the year? Is there a good reason it's a once-a-year activity for most investors? More importantly, is there a better way to do it? These might be simplistic questions to some, but the answer to the last question may be eye-opening.

Why do investors tend to tax-loss harvest at the end of the year?

There are three primary reasons why this is an end-of-year activity for many investors and financial advisors:- To offset gains realized during the year: For many, loss harvesting is done at the end of the year as a way to balance out or offset gains realized during the year. These realized gains could mean a sizable tax bill for the year for investors. So it becomes a scramble at the end of the year, digging through the portfolio to identify holdings with losses than can be "harvested" to try to minimize some or all of the realized gains.

- This is when everyone does it: Financial advisors often tell me they conduct end-of-year loss harvesting because that's what they were told to do. At the start of their careers, they picked this up as an end-of-year activity from the more senior and experienced advisors and industry professionals around them. The business and financial advice media also highlights this heavily as something you do during"tax-loss harvesting season."

- Procrastination: Honestly, who truly looks forward to digging through an investor's account looking for"investment mistakes" and "losers?" It's a time-consuming activity since it needs to be done account by account, client by client. It takes time and energy and finding those "losers" are reminders of unsavory investment decisions. As such, there is a tendency to procrastinate and wait until the end of the year to do tax-loss harvesting.

How has year-end tax-loss harvesting worked for individuals?

Since many investors and financial advisors perform their tax-loss harvesting activity once a year, at the end of the year, let's look at the effectiveness of this strategy.

The U.S. stock market, based on the S&P 500 Index, has ended the year positive more than 70% of the time since 1926. Over the past 70 years, in terms of monthly returns:

- November has been the single-best stock market month.

- December has been the third-best stock market month.

In other words – on average -- waiting until November and December to perform tax-loss harvesting may be limiting investors to two of the worst months to harvest losses.

U.S. equity: Months with UP and DOWN markets / 1950 - 2023

|

# of Up Years |

# of Down Years |

Avg. Monthly Return (S&P 500) |

|

|

January |

44 |

30 |

1.12% |

|

February |

40 |

34 |

0.03% |

|

March |

50 |

24 |

1.18% |

|

April |

53 |

21 |

1.59% |

|

May |

45 |

29 |

0.36% |

|

June |

42 |

32 |

0.19% |

|

July |

44 |

30 |

1.34% |

|

August |

42 |

32 |

0.10% |

|

September |

34 |

40 |

-0.64% |

|

October |

44 |

30 |

0.97% |

|

November |

52 |

22 |

1.95% |

|

December |

56 |

18 |

1.57% |

Source: Factset & Morningstar Direct. As of 12/31/2023. U.S. Equity: S&P 500 Index. For months Jan. 1980 – Jan 1988; Price Return, Feb. 1988 forward: Total Return. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

As the chart above shows, it's important to actively manage for taxes throughout the course of the year, and not just as an end-of-year exercise. Moreover, in addition to loss harvesting, there are more active tax-managed strategies available to mitigate the tax drag in investment portfolios. These also can be implemented through the entire year.

Does timing your tax-loss harvesting matter?

The short answer is YES!

Done correctly, tax-loss harvesting takes advantage of market corrections—in a sense turning lemons into lemonade. The volatility seen in the first few months of 2020 are a good example. The market's reaction to the start of the Covid pandemic was an ideal time to be harvesting losses. The U.S. Federal Reserve's series of interest rate hikes to battle inflation in 2022 presented a number of opportunities throughout the year to harvest losses. And in 2023, even though the market was largely positive, the volatility seen in the winter and summer months created loss-harvesting opportunities. Advisors need to be ready to act—and to act quickly. As an advisor, you also need a systematic process to understand which clients may benefit.

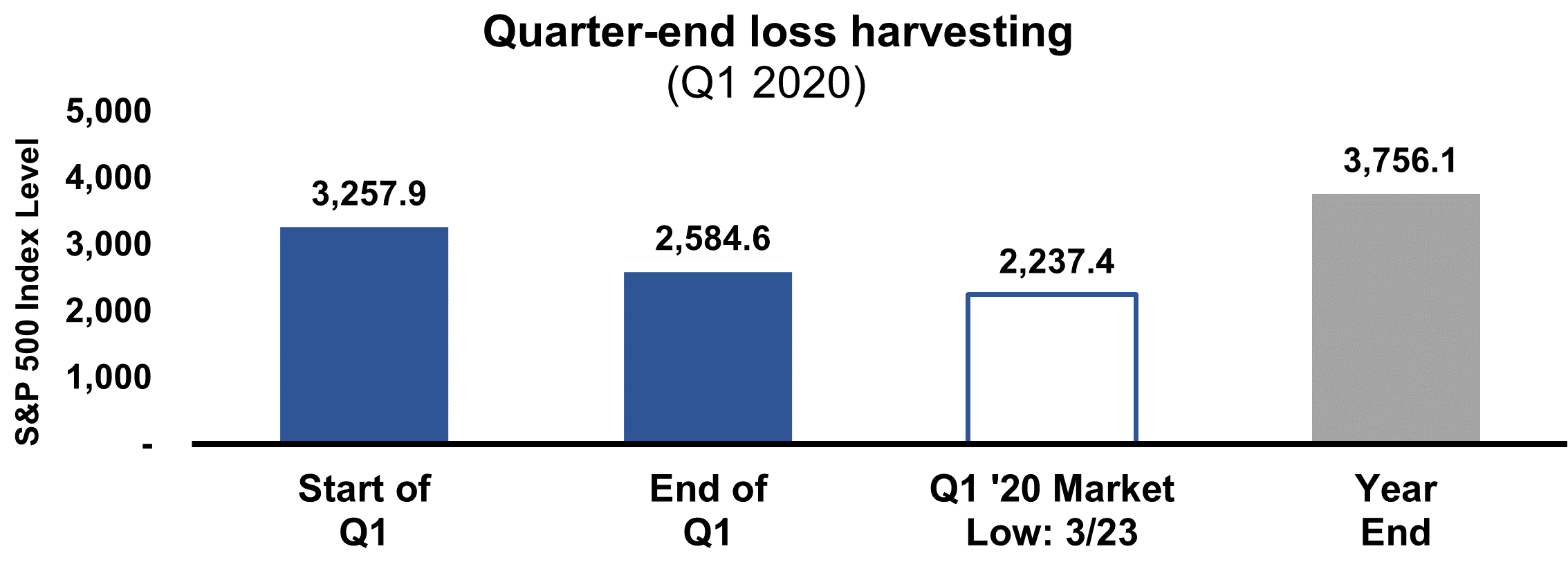

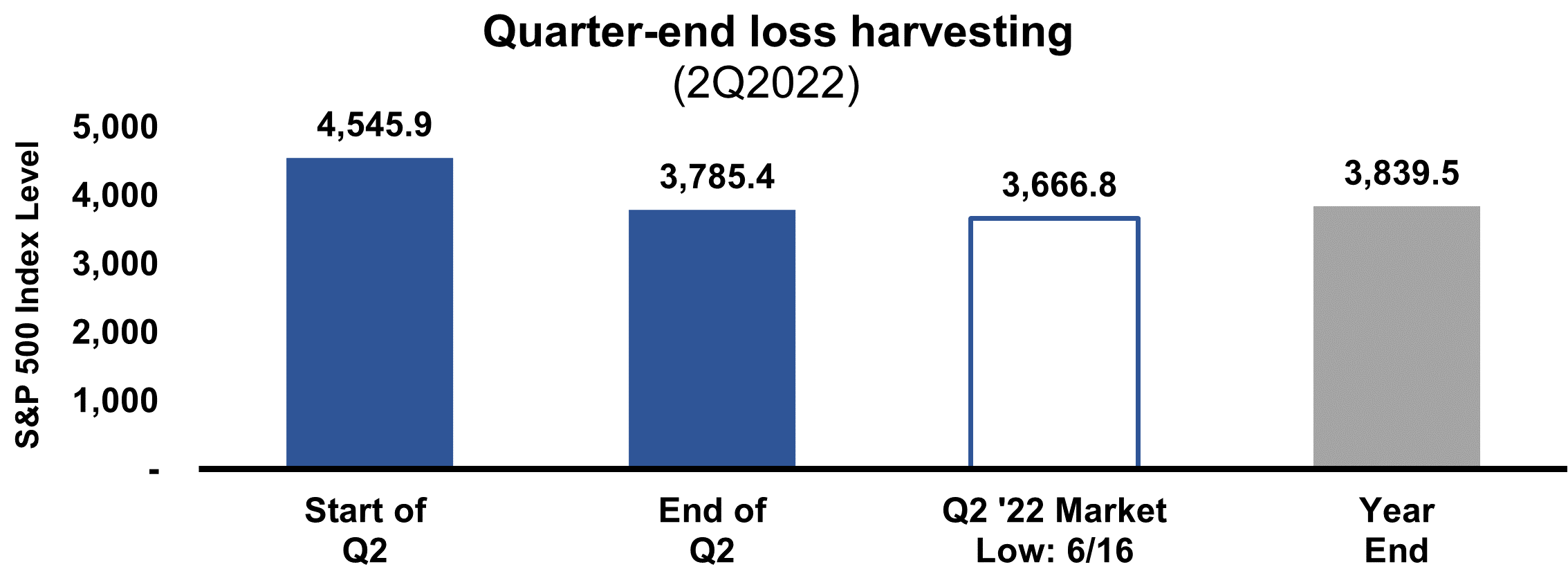

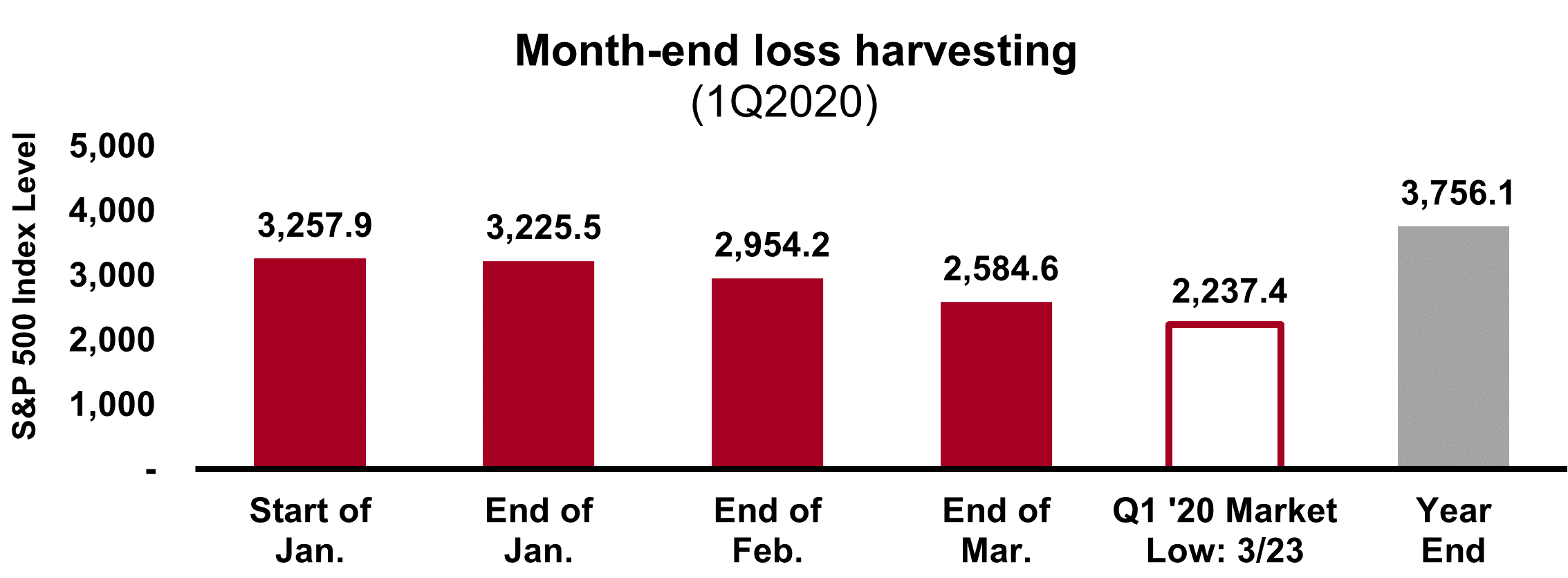

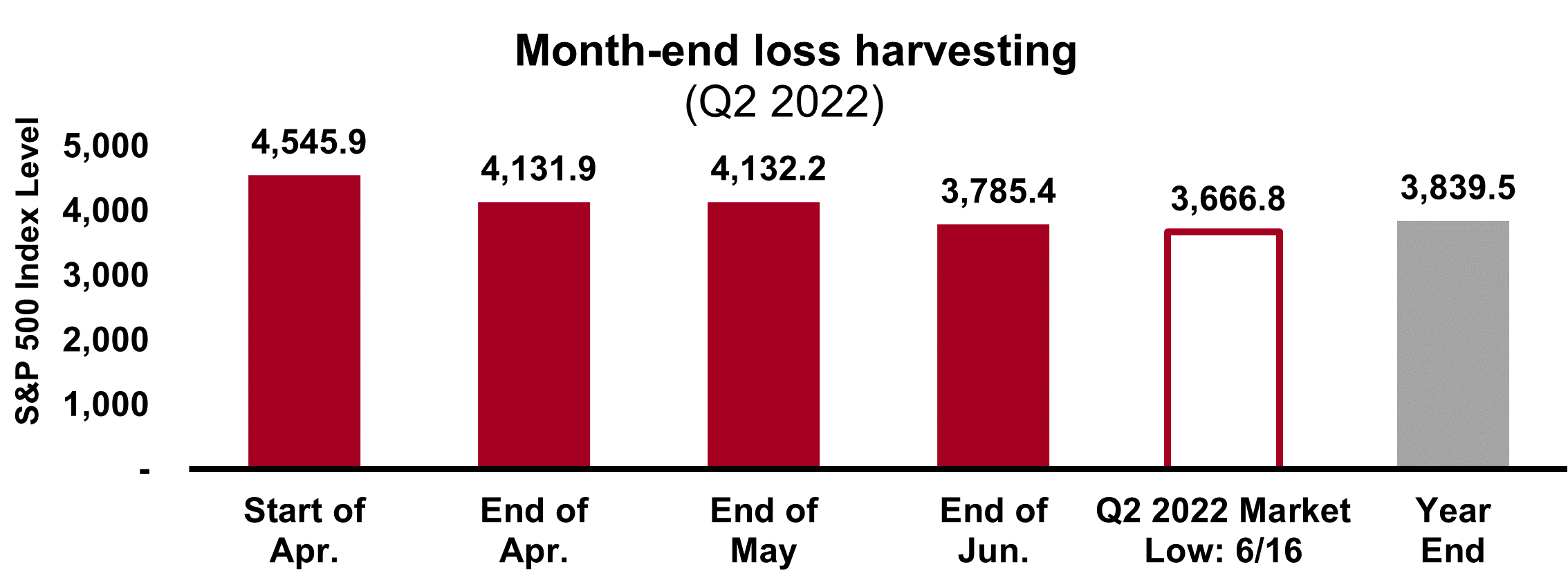

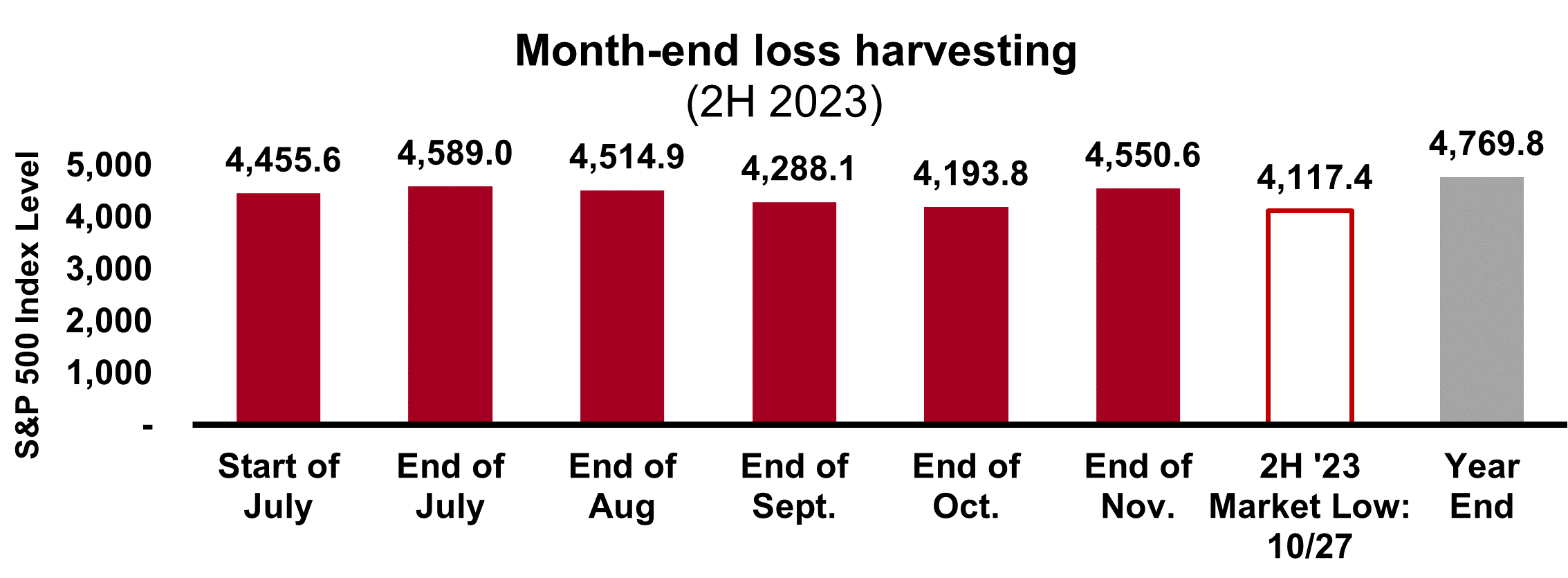

Let's look at several recent 8-10%+ market corrections: the first quarter of 2020, the first and second quarter of 2022 and the second half of 2023.

Did the timing of tax-loss harvesting matter? What if tax-loss harvesting was systematic through the partnership with an overlay manager? And what if the overlay manager's process only looked at valuations at month or quarter end- or even year-end? Let's look at two different scenarios:- Loss harvesting at quarter-end

- Loss harvesting at month-end

For illustrative purposes only.

Note that the best time to harvest losses (market low) did not coincide with quarter-end dates.

For illustrative purposes only.

Once again, the best time to harvest losses (market low) was not on the last day of the month.

It's easy to see the difference between the market low and the month-end or quarter-end. While no one can call the market bottom in the moment, having a process that looks beyond specific dates widens the opportunity set to achieve better results from loss-harvesting efforts. The illustrated differences show the importance of having a systematic tax-loss harvesting program that is monitored and run constantly, whenever markets are open. We believe the best tax-managed programs have robust, experienced, in-house trading capabilities that are laser-focused on seeking the optimal after-tax returns for investors and are prepared to harvest losses whenever they occur, even if the trading activity falls on Christmas Eve.Timing matters… when it comes to tax-loss harvesting

That's the moral of this story. Every season could and should be tax season – when it comes to tax planning and tax management. Tax-loss harvesting is such an important part of After-Tax Wealth Creation – too important to have it be done just once a year, at the end of the year. In order to opportunistically take advantage of the market movements to create these valuable tax assets, investors need to act fast and be ready at all times. Using a fully integrated tax-management process that systematically harvests losses when they are created gives investors a leg-up on saving more on taxes and generating better after-tax wealth.

1 Source: Morningstar, 2024.