Why the climate transition means renewables are here to stay

Fixed Income Survey 2020: Are markets sailing to the U.S. Federal Reserve’s rendition of steady as she goes?

In our latest assessment of the fixed income landscape, 48 leading bond and currency managers considered valuations, expectations and outlooks for the coming months.

Managers had to contend with a myriad of developments recently — a trade war between the U.S. and China, Brexit uncertainties, slowing economic growth and U.S. President Donald Trump’s impeachment proceedings. A new developing headwind, meanwhile, is the potential negative impact of the spread of the coronavirus on both the Chinese and global economies in 2020.

Some respite came in the form of phase one of a potential Sino–U.S. trade deal and some clarity over Brexit, after Prime Minister Boris Johnson’s Conservative Party’s commanding majority win in the UK general election. However, the main tailwind managers were expecting was action from the U.S. Federal Reserve (Fed). The Fed delivered three rate cuts as part of a mid–cycle adjustment approach.

Following this, markets seem to have agreed that 2020 will be steady as she goes. But then came the coronavirus outbreak. This, when coupled with the looming U.S. election - including the potential for candidates on the opposite side of the spectrum to go head-to-head, leads us to believe that 2020 is most likely to be anything but another typical year.

Market views

Views from interest rate managers

- On a weighted average basis, managers expect less than one interest rate cut for the U.S. in 2020. This is down from two interest rate cuts in the last survey.

- 50% of managers expect no movement from the Fed for 2020 and just 15% see one rate hike — which differs from the last survey when nobody expected any hikes.

- Meanwhile, 40% of them expect to see some adjustment from the Fed between Q2 2020 and Q4 2020.

- Inflation is expected to remain at current levels – namely in the 2.0%–2.2% range. However, we wonder if markets are accounting for the risk of presidential candidates with large fiscal spending proposals.

- Relative to our last survey, there were no changes in opinion regarding the 10–year U.S. Treasury interest rate in 12 months’ time (~1.8%).

- When asked about potential negative interest rates by the Fed during the next recession, 95% of managers responded that they do not believe the Fed will take rates into negative territory. 5% of managers expressed no view about the matter.

Views from credit managers

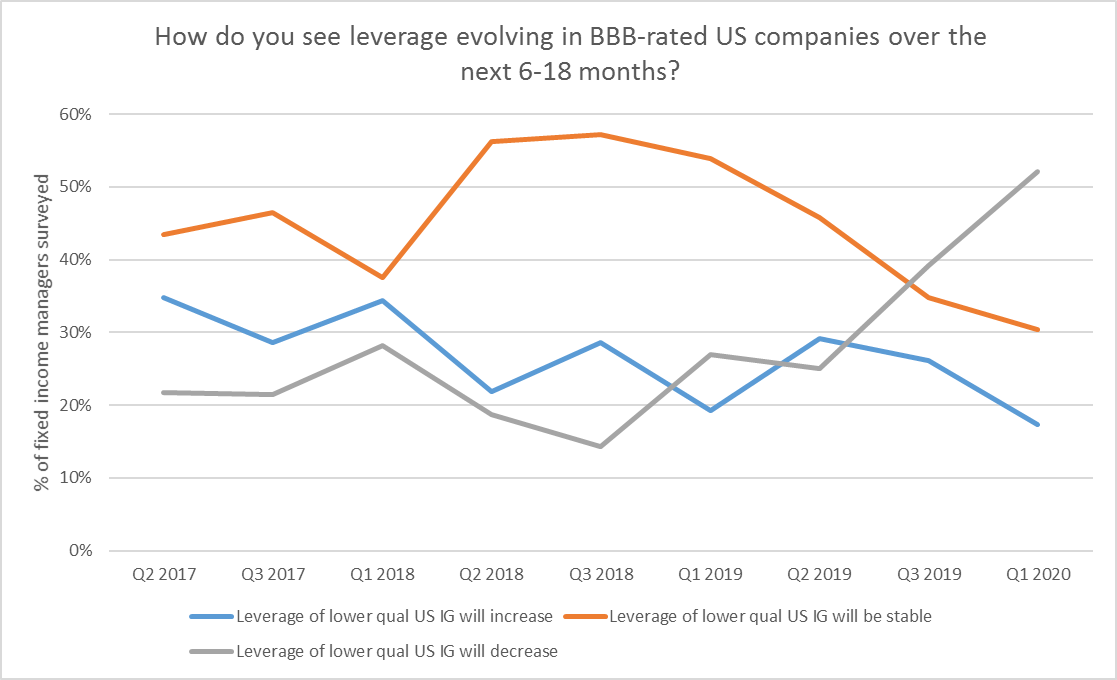

- Regarding performance in the BBB space, this is the first time since the survey started that managers expect leverage to decrease in the following 6–18 months (52% vs. 39% last quarter). This may be influenced by better sentiment on corporate fundamentals, where almost 50% of managers expressed confidence in the performance of both companies and the overall economy. Click image to enlarge

- 42% of managers consider U.S. high yield bonds to offer the most compelling opportunities in the corporate space — the highest since Q1 2018.

- In the global investment–grade credit space, managers seem to be more comfortable with the current level of credit spreads vs. risks of deteriorating credit fundamentals.

- In the last survey, there was a modest bullish tone when it came to securitized assets, with managers adding a bit more risk. In this survey, managers seem to be maintaining current positions — while just 22% of them are adding risk.

Source: Russell Investments. IG=Investment Grade

Risk across the globe

Europe and UK

- In contrast to the last survey, managers moderately increased their optimism on Europe, whille decreasing it for the U.S. — levelling out sentiment for both regions in the investment–grade credit space.

- G30 FX (foreign exchange) managers also indicated that the U.S. dollar will not outperform in 2020. Consequently, 40% of managers now believe that the euro will see a modest appreciation versus the greenback in the next 12 months.

- With lower uncertainty around Brexit, managers seem more comfortable with the pound being in the £1.26-1.30 range. 30% of managers believe that the pound should appreciate against the U.S. dollar in the approximate £1.31–1.35 range.

Emerging markets

- Local currency emerging–market debt (EMD) is preferred over hard currency EMD in both short–term and long–term horizons. Almost 40% of managers still consider local rates to be cheap — with many believing them to be fair value. This is in spite of record low yields in the asset class. There is a neutral view on inflation with only 24% of managers seeing inflation going higher.

- The Russian rouble, Brazilian real and Mexican peso were the most favoured currencies from a local perspective. The Thai baht remains the least preferred currency, followed by the South African rand. There was, however, a warming sentiment toward the Turkish lira.

- Most managers now expect a range–bound performance of hard currency EMD spreads during 2020. In Q3 2019, most managers were expecting a modest tightening.

- From the survey we discovered that the preferred allocations (for hard currency EMD) were overweights to Ukraine, Brazil, Argentina and Mexico. The main underweight positions were the Philippines and China.

- Changes in U.S. Treasuries and a slowdown in the Chinese economy are the two main risks for managers.

Conclusion

Amid trade and economic growth concerns, the Fed gave the markets the rate cuts it desired. Interest rate managers reacted positively and broadly do not expect any significant movement from the Fed this year. Additionally, as optimism increases around the performance of the economy, managers seem to be more confident in the outlook for the BBB space. Managers also consider U.S. high yield bonds to offer considerable opportunities. This appetite for risk would clearly indicate that the markets are singing the tune of steady as she goes — as broadly engendered by Fed actions.

However, are managers too reliant on the Fed to provide meaningful tailwinds? In this survey, we also discovered that managers (for the first time since 2Q 2018) are concerned about geopolitical risks which show no signs of abating. More managers also indicated concerns about a global slowdown. When markets stop singing, managers have looked to the Fed for support.

Can the Fed react by going lower on rates? Is it willing to consider zero bound? 202 thus far has already given us enough to mull over — notwithstanding the looming U.S. elections — and the headwinds don't look to be fading anytime soon.