Private Assets: The next frontier for retail investors

Institutional investors, including the world’s largest pension plans, endowments and foundations, have been incorporating alternative investments in their portfolios since the 1980s.¹

Many credit the popularization of incorporating alternative assets in portfolios to the late David Swensen, Chief Investment Officer at Yale University from 1985 to 2021. Swensen and his team looked for investments that would offer higher return and diversification, resulting in large allocations to private assets and hedge funds. In 2019, about 60% of Yale’s portfolio was allocated to alternative investments including private equity, venture capital and hedge funds.²

Universities with large endowments were early adopters of alternative investments, given their aggressive return targets and perpetual time horizons.3 This approach of substantial allocations to alternative investments has been called the "endowment model."

In this blog, we will focus on private assets and cover what they are, the reasons to allocate to them, and challenges to investing in them.

What are private assets?

Private assets are investments that are not available through public markets such as stock exchanges. Private markets include private debt, private equity, venture capital, and private real assets (infrastructure, real estate and natural resources).

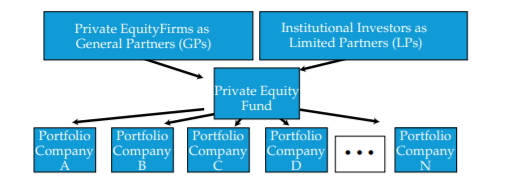

How investors gain exposure

Investors typically get exposure to these type of assets by investing in a fund. If we use a private equity fund as an example, investors (known as limited partners) provide capital for the private equity fund. The private equity firm that manages the fund is known as the general partner. Limited partners commit capital before any investments are made, which the general partner then “calls” over time as investments are made. Capital is then returned to limited partners over time when the gains on the underlying investments are partially or fully realized. The investment period typically lasts one to four years, and the distribution period typically occurs over six to 10 years. Once all capital is returned to investors, the fund is wound down.

Click image to enlarge

Source: CFA Institute: Alternative Investments: A Primer for Investment Professionals

Reasons to allocate to private assets

Similar to what David Swensen and his team at Yale were looking for when evaluating alternative assets, the vast majority of institutional investors look to private assets for diversification and the opportunity to generate higher returns. According to Shroeders Institutional Investor Study 20214, 80% of respondents listed diversification and 75% listed higher return potential for reasons to invest in private assets. Additionally, 90% of respondents were looking to increase their allocation to one or more private assets over the next 12 months.

The Pension Investment Association of Canada (PIAC), which is comprised of more than 130 pension plans overseeing close to $2.5 trillion in assets, publishes asset mix reports annually. For the year ending 2020, average exposure to alternatives ranged between 10% to 30%, with private equity, private debt, real assets and hedge fund strategies making up the bulk of the allocation5. Using a more specific example, CPP Investments, a global investment management organization that invests the assets of the Canada Pension Plan, had a 26.7% allocation to Private Equities, as per their 2021 Annual Report6.

Potential to generate higher returns

Both private equity and private credit have outperformed their public market equivalent over the last 20 years (as at 2019 year-end)7. More specifically, buyout equity has outperformed the MSCI World Index in 19 of the last 20 vintage years by an average of 6.62%. Similarly, private credit has outperformed its public counterpart in 20 of the last 20 vintage years by an average of 5.48%8.

Diversification

Many investors might be surprised to learn that 87% of U.S. companies with more than US$100 million in revenue are private9. To further put this into perspective, there are more than 17,000 private companies in the U.S. with annual revenues above US$100 million versus approximately 2,600 public companies with revenues above US$100 million.10 These figures demonstrate the large opportunity set in the private markets space that savvy investors can seek to capitalize on. As equity indices become ever more concentrated, an allocation to private assets can help diversify a portfolio.

Another fact that might surprise investors is that private equity (specifically, developed market buyout equity) and private credit have proven to be quite resilient during market downturns. Both developed market buyout equity (+2.4%) and private credit (+5.4%) posted positive returns during the worst five-year rolling period for their public market equivalents, MSCI World Index (-5.7%) and Bank of America Merryll Lynch High-Yield Index (-0.9%), respectively.11 Thus, the addition of these types of private assets to a traditional 60% equity/40% fixed income portfolio can provide downside protection during times of market turbulence. With that said, not all areas of private markets show this type of resilience during market downturns, with venture capital typically experiencing worse drawdowns as compared to public markets, so understanding the risk/return dynamics of various private markets strategies is crucial. In addition, it must be noted that returns for private assets funds are disclosed monthly or quarterly, which can smooth out the volatility profile compared to public market investments, where the returns are disclosed daily.

Challenges to investing in private markets

Investments in private assets have been dominated by institutional investors. Traditionally, it has been challenging for retail investors to access private assets and there are several reasons why. Firstly, these types of funds typically require high minimum investment amounts in the six- or seven-figure range. Secondly, private assets funds can have lengthy lock-up periods, typically seven to 10 years for private equity funds. Finally, management fees tend to be higher than traditional mutual funds and Exchange-Traded Funds (ETFs), and performance fees are standard practice12.Given the high minimums, illiquidity, and higher fee structure, it is no surprise the average retail investor has very little to no exposure to private assets.

The bottom line

The key drivers for investing in private assets are diversification and the potential for higher returns. Thus, the inclusion of private assets to a traditional portfolio of stocks and bonds has the potential to generate superior risk-adjusted returns. In a low yield environment and after an extended bull run in public equities, retail investors would be well advised to consider an allocation to private assets.

1Source: CFA Institute: Alternative Investments: A Primer for Investment Professionals

3Source: Chartered Alternative Investment Analyst Association (CAIA Association).

4Shroeders Institutional Investor Study 2021 https://www.schroders.com/en/uk/pensions/insights/institutional-investor-study-2021/

5Source: https://piacweb.org/site/publications/asset-mix-report

6Source: https://www.cppinvestments.com/the-fund/our-performance/financial-results/f2021-annual-results

7Source: Hamilton Lane, Bloomberg, as of July 2021. Private equity performance based on 1142 funds in the universe of managers. Funds selected by Hamilton Lane for this exhibit include all funds in which Hamilton Lane clients invest. Private credit performance based on 539 funds in the universe of managers which include all funds in which Hamilton Lane clients invest. Performance is net of fees and expenses.

8Source: Hamilton Lane, Bloomberg, as of July 2021.

9Source: Hamilton Lane, Capital IQ as of February 2021

10Source: Hamilton Lane, Capital IQ as of February 2021

11Source: Hamilton Lane via Cobalt, Bloomberg, as of September 2020.

12Performance fees are payments made to an investment manager for generating positive returns above a certain threshold. They are intended to ensure that the managers’ and investors’ interests are aligned.