Private credit: Why we believe ‘now’ is the time to invest

Private markets and market timing are two phrases that typically do not belong together. Private market vehicles can generate premium returns over publicly traded markets with lower volatility1 in large part because they take away the investors’ ability to precisely time when the money comes in and out. That said, any investor is going to ask why now? when making a new investment. This is good governance and merits a serious response. So, let’s dive into some of the reasons why we believe investors should put their money into private markets, specifically private debt, now.

Reasons to consider investing in private credit now

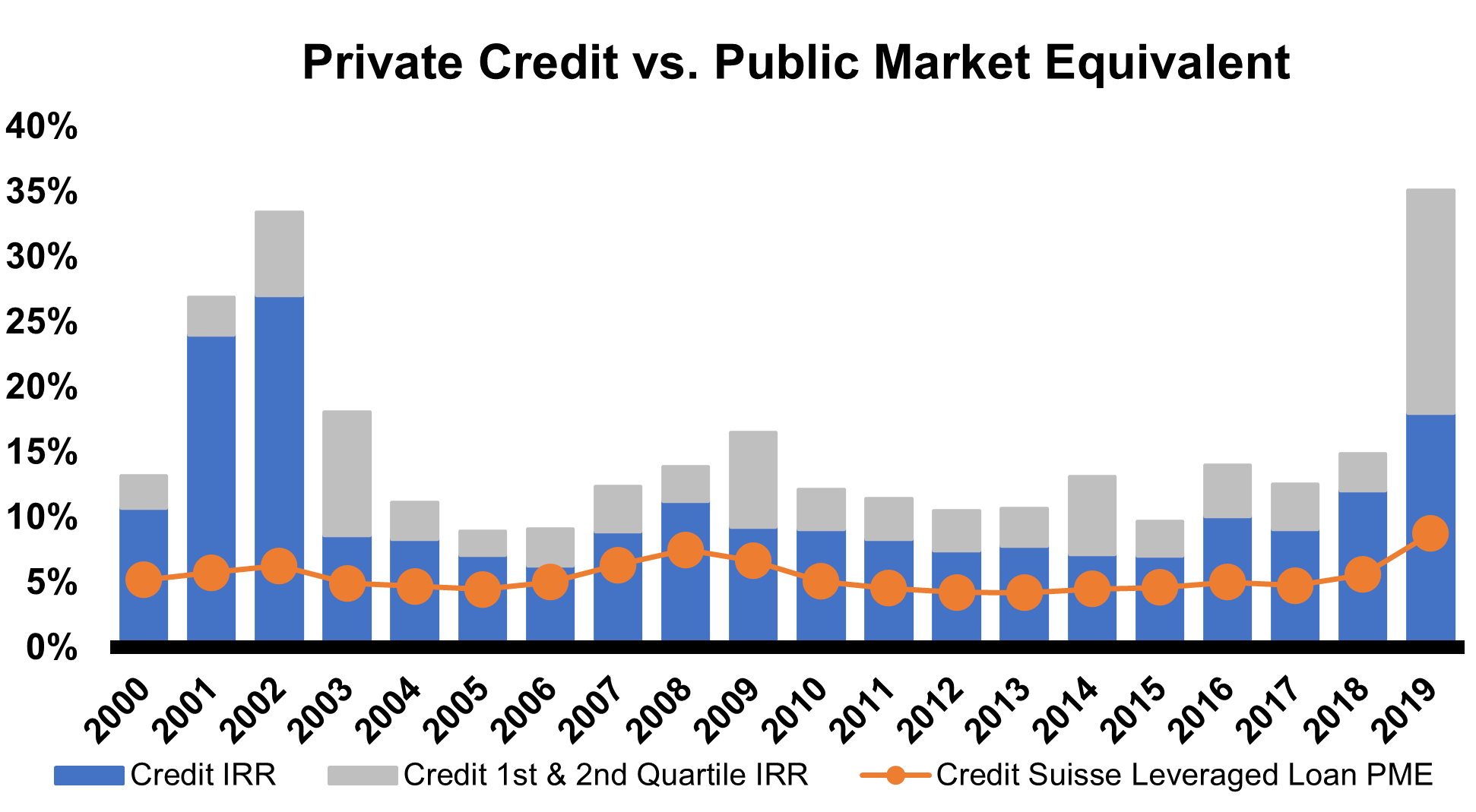

Well, firstly when it comes to private credit, the numbers don’t lie. When we compare credit vintage by vintage against the public market equivalent in the syndicated bank loan market, the private debt market has produced a higher internal rate of return (IRR) every single vintage.2

To be fair, an IRR is a total outcome, which is arguably the most important way to assess investment success, but many investors are accustomed to viewing performance and feeling risk through the lens of time-weighted returns. That is month-over-month or year-over-year return assuming a constant amount of money invested. On this front, the public market does only a little better. Over the last 15 years, the Cliffwater Direct Lending Index, a representative benchmark for private credit, has outperformed the Credit Suisse Leveraged Loan Index 8.71% to 3.95%3. And, of the last 15 calendar years, the private credit market has outperformed in all but one4. To us, this shows that rare is the time NOT to invest in private credit relative to public credit markets.

Private credit funds have greater market coverage

Another advantage private investment vehicles have is their ability to pivot on strategy, which is particularly relevant today. While we commonly refer to this distinction between private vs. public credit funds, the real distinction is not so much in the nature of their holdings as it is in the terms of their liquidity. Sure, private funds tend to emphasize directly originated credit (where the manager holds most or all the loan) whereas public credit funds buy broadly syndicated loans or bonds and only own a small fraction of the total loan. But there is nothing to stop private credit funds from crossing over into more liquid markets when one of those rare opportunities presents itself to generate compelling returns by buying syndicated credit. Arguably, now is one of those times, with the high yield bond market actually offering a cash yield competitive with private market spreads.5

Investors going into private credit vehicles aren’t giving up on this opportunity. Many private credit funds will pivot to buying a hung bank loan syndication and even buying from forced sellers (often public funds) at knock-down prices. Conversely, public credit funds simply can’t go the other way in any meaningful amount due to demands of the liquidity they offer investors.

Capturing the opportunity from the scarcity of fresh capital in today’s market

Importantly, when public markets sell off like this, capital in private markets tends to dry up too. This typically leads to opportunities to be a provider of scarce capital at higher rates of return to investors. Indeed, that is what we have been seeing in 2022 as origination spreads on new loans have begun to widen back out after years of creeping tighter and tighter.

Private Credit New Issue Spreads by Vintage6

While median spreads have not moved meaningfully higher in this data, private markets data is notoriously lagged and anecdotal conversations with managers suggest those average spreads have been moving wider in recent months. Regardless, the breadth of the distribution has widened and that is good news for private credit strategies that are looking to differentiate from the pack.

The bottom line

So, when clients ask why private credit, we believe there are some very compelling reasons why now, more than ever, investors should be considering an allocation to private credit. Today’s environment is especially enticing for specialist investment strategies where there is less competition that can take advantage of wider spreads to lock in higher yields. In our opinion, that should lead to better returns and more income for investors now and into the future.

1 Refer to chart 1

2 Source: Hamilton Lane, Bloomberg, July 2021. Performance based on 539 funds in the universe of managers. Funds selected by Hamilton Lane for this exhibit include all funds in which Hamilton Lane clients invest, and which have been subject to Hamilton Lane’s due diligence process. Performance shown is net off fees and expenses. Past performance is not indicative of future results.

3 Bloomberg data as of 9/30/2022

4 Bloomberg data as of 12/31/2022. That one year was 2009 as liquid markets rallied off the extreme market bottom.

5 Bloomberg data as of 9/30/2022

6 PitchBook Data from 1/1/2010 to 9/30/2022