Q4 update: Real-time risk exposure report

As institutional investors, we most often represent risk as standard deviation or tracking error. But when we implement changes in our portfolios, the real-time risk happens much faster. Those standard deviations will impact portfolios not on an annual scale, but in hours or even minutes. What happens in those minutes can have lasting effects on performance.

Investors generally don't have visibility to the real-time implementation slippage that can occur without an intentional focus on real-time exposures. Very few investors have detailed real-time post-implementation reporting to verify that their exposures were managed appropriately throughout the course of implementation.

The cost of just one hour of misaligned exposure

How much can a market hour of misaligned portfolio exposure impact performance? The risk of a market hour, as represented in the chart below, demonstrates just how impactful it can be. In recent market experience with U.S. equities, U.S. Treasuries and international developed equities, just one market hour can have a standard deviation of +/-nearly 50 basis points.

Click image to enlarge

1 - Hourly tracking errors calculated based upon 60-day historical tracking errors between S&P 500 ETF (SPY), Long Treasury ETF (TLT), MSCI EAFE ETF (EFA) and cash through – 09/30/2022. Standard & Poor's Corporation is the owner of the trademarks, service marks, and copyrights related to its indexes. For illustrative purposes. Data is historical and not a guarantee of future results. Indexes are unmanaged and cannot be invested in directly.

How can investors better manage real-time implementation exposure risks?

- Use an overlay manager. An adept overlay manager can provide needed market exposures with derivatives, while providing the flexibility to quickly execute exposure trades to balance or offset physical trading activity or pooled fund redemptions and subscriptions.

- Use a transition manager for large changes to physical portfolios. Work with a skilled transition manager who is accountable for portfolio performance and is focused on managing real-time risk exposures. This is industry best practice for large portfolio changes.

- If possible, ensure the overlay manager and transition manager reside within the same organization. The ability of the transition manager to work with the overlay manager in real-time, on the same systems, with precisely synchronized execution of derivative and physical transactions provides the most seamless implementation of large asset allocation shifts. This harmonized implementation structure affords the investor confidence that exposures are intentional and aligned for success. Compare this synchronized TM/OS provider to the alternative of separate firms managing different portions of the implementation. You'll easily see that the disparate organizations trying to coordinate trading activity leaves the investor open to exposure gaps and more implementation slippage.

The bottom line

Investors should be aware of potential real-time market exposure risks when implementing large changes to their portfolios and they must be intentional in managing these risks. The risks are particularly large when making asset-class shifts and when international markets are involved with discontinuous market hours. Capabilities are key, but the strategy in which those capabilities are applied is even more critical to success. Many asset managers and brokers have derivatives and physical trading capabilities. That's the easy part. But effectively combining these capabilities to minimize market exposure risks, often across numerous mandates, in real-time, at a single provider, is a rare organizational structure.

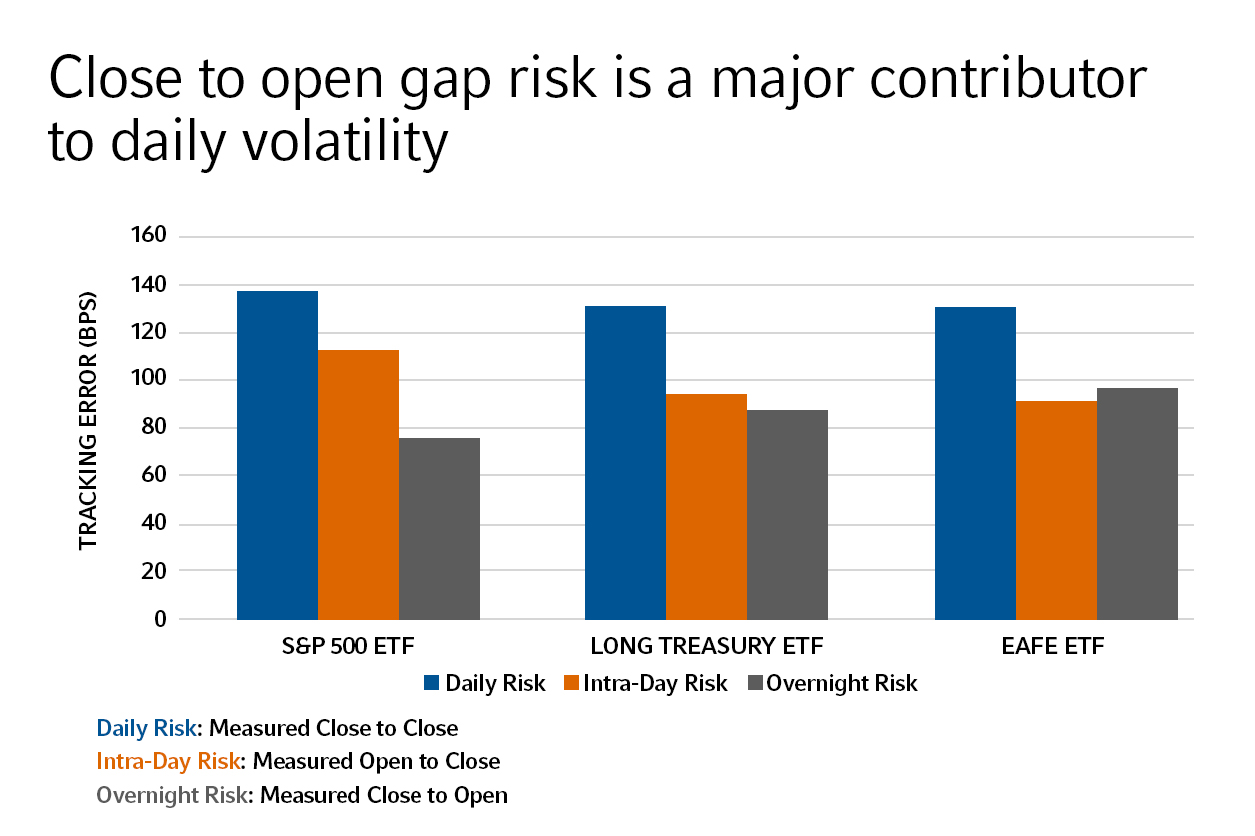

What happens while you sleep?

Overnight risk or gap risk is a common exposure risk that institutional investors can overlook without guidance from implementation experts.

This occurs when the exposure is lost at the close, perhaps coming out of a commingled fund, and the replacement exposure is gained the next morning on the open. From a market clock perspective, this is very sensible. After all, only being out of the market while the market is closed should be harmless, right?

The reality is that the price is received at the next day's open is often very different than that of the prior night's close. In the chart below you see that the tracking error of overnight exposures is significant relative to the day-to-day volatility of the market overall.

Using thoughtful approaches to manage exposures, including bridging exposures using derivative overlays, is one way to limit these unwanted risks that can materially impact outcomes unnecessarily.

Learn about transition management

To successfully manage large-scale portfolio changes, investors need to partner with a firm that has a core competency in coordinated trading in local-market physical securities and derivatives, with best-in-class currency execution facilities. This combination of capabilities doesn't come about by chance. Rather, it must be intentionally built, with the expertise and infrastructure to effectively manage large portfolios in flux.