T is for tax-efficient planning. And the time is now.

For your tax–sensitive clients, taxes may be the largest fee they don’t know they’re paying when it comes to their investment portfolios. At Russell Investments, we call unnecessary taxes the government expense ratio.

How big is that fee? According to Morningstar, as a whole, Canadian equity funds (active, passive, Exchange Traded Funds) gave up on average 1.5% of returns to taxes every year in the three years ending November 2020.1 That means a mutual fund with a 10% pre–tax, three–year annualized return actually would have had an annualized return of only 8.5% on an after–tax basis. This tax impact of 1.5% is larger than the total fee most advisors charge. If you think of it in terms of the power of compounding—or rather, the foregone opportunity of the power of compounding—you realize that smaller percentage numbers add up to be real money for real people living real lives.

So, taxes matter.

This is the fifth and last blog in our 2020 series, discussing why Russell Investments believes in the value of advisors, based on this easy–to–remember formula:

Click image to enlarge

In this section, we’re talking about T, which stands for tax–efficient planning and investing. Because it’s not about what the investors make. It’s about what they keep.

How much could tax management save your investors?

Taxes have the ability to seriously erode returns. While downward fee pressure can mean downward value trends in other areas, advisors who focus on

tax–efficient investing can distinguish themselves and demonstrate differentiating value.

Just how much return can be added when the impact of taxes on an investment is taken into consideration? You can find out right now. We’ve created a Tax Illustration tool which allows you to compare investment solutions on a

tax–adjusted basis and quickly assess the tax implication between products on a forwarding looking basis. Ask your Russell Investments sales representative for access to our secure advisor site to use this tool. Just select a corporate class mutual fund and a comparable trust mutual fund. You can also check out the table below, which gives a quick overview of the different rates of taxation on different types of distributions. Corporate Class funds can provide their monthly distributions in the form of Return of Capital, which can make them a more tax-friendly choice for investors who have non-registered investments.

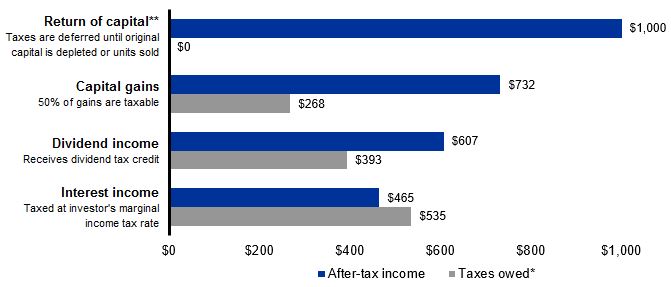

Differences in taxation for $1,000 of distributions

Click image to enlarge

For illustrative purposes only.

All examples shown are based on the following 2020 Ontario marginal tax rates for calculating the tax liabilities: interest income = 46.4%, Canadian eligible dividends = 29.5% and capital gains = 23.2%

Are you a tax–efficient advisor?

Many advisors already think they have taxes handled, so we encourage them to answer these five questions:

- Do you KNOW each client’s marginal tax rate?

- Do you PROVIDE intentionally different investment solutions for taxable and

non–taxable assets? - Do you EXPLAIN to clients the benefits of managing taxes?

- Do you PARTNER with local CPAs2 to minimize tax drag?

- Do you REVIEW your client’s T–3 (and/or T–5)?

If you can answer yes to all five of these questions, then congratulations, you’re already a tax–efficient advisor. If you answered no, then we’re here to help.

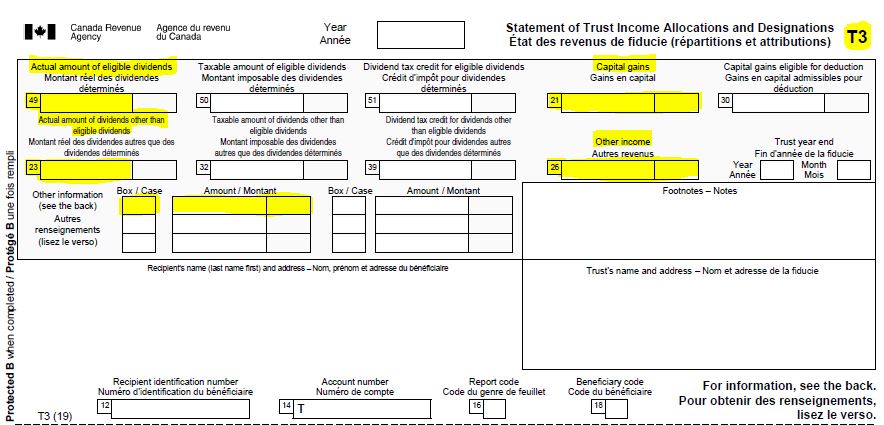

A forensic review of theT–3 form

While it’s important to always keep taxes in mind when investing, there are two key dates in the year that advisors should focus on to assess a client’s tax situation:

December 31 and April 30. If all you look at is the total portfolio growth that happened at that year–end date, without thinking about the April 30 tax bill due date, then you may be missing a serious opportunity.

A forensic review of the T–3 can be really eye–opening. Looking at the T–3 connects the dots between what a client makes and what a client actually keeps. The tax process sometimes buries that: Clients don’t necessarily connect what they are paying with what they are investing, because of the complex forms required by the Canada Revenue Agency (CRA).

This is an opportunity for advisors to shine. Simply walking through the T–3 and discussing insights, implications, and income impact for clients can be truly beneficial. On their own, clients are unlikely to connect the dots between dividend distributions and the impact on their total wealth return. You, the advisor, can reveal what they may be sacrificing to taxes. And better yet, you can do something about it.

Forensic review of the CRA Form T–3

Connecting the dots between what a client makes and actually keeps

Click image to enlarge

Box 49: Total amount of eligible dividends

Box 23: Total amount of non-eligible dividends

Look for: Difference between 49 and 23. Too many non-eligible dividends? Does the client need dividend income?

Box 21: Capital gain distributions. Understand amount as percentage of total investments. Are gains out of line with investment size?

Box 25 (optional box) and 26: Other income includes interest income, foreign dividends and foreign income. Know client’s tax and tax-equivalent yield.

Now is the time to start managing taxes

In this year of historic government stimulus packages, the question we should all be asking is, “ How are we going to pay for all this?” The Canadian government has so far committed $325 billion, or 14% of the country's gross domestic product in direct support to individuals and businesses to offset the impact of COVID-19.3 I don’t have a crystal ball, but it seems unlikely that taxes are going down.

So don’t wait to consider tax efficiency in your discussions with clients. Why? Because every year—even in down years—many mutual funds are hit by big capital gains distributions. At the same time, some investments may pay close to zero percent in taxes—a significant savings.

Communicate your value

This is the final installment of our 2020 Value of an Advisor series. But all this proven value that we’ve discussed in this blog post, in the series, and in the full report, can go unnoticed by your clients without one vital action on your part: communication.

Advisors need to communicate the value they provide to their clients. Communication, as an academic discipline, is deceptive because everybody thinks they’re good at it. But for most advisors, we have found that the quality of their communication would benefit from greater effort and greater intentionality. After all, your value is only as good as the client experience that you are reliably delivering, clearly communicating, and constantly elevating.

So then, what are you going to do to elevate your value? A tax–efficient approach might be your best place to start. We are ready for you. Are you?

1 Source: Morningstar. Canadian equity funds: mutual funds and ETFs in Morningstar categories: Canadian Dividend & Income Equity, Canadian Equity, Canadian Focused Equity, Canadian Focused Small/Mid Cap Equity, Canadian Small/Mid Cap Equity, including all share classes.

2 CPA refers to Chartered Professional Accountant

3 Source: https://www.canada.ca/en/department-finance/economic-response-plan/fiscal-summary.html