Five key ways advisors deliver value in the face of 2020’s adversities

We believe advisors have never been more valuable than they are right now, in the midst of these challenging times.

For the past five years, we’ve created an annual report that holistically analyzes the real value advisors deliver to their clients in their portfolios, in vital services advisors provide, and, right now in particular, in helping investors avoid behavioral mistakes.

This year, when a flock of black-swan events have flown overhead, the vital role advisors play should be more obviously valuable than ever. Volatility is back with a vengeance. Economic hardships are piling up. And fight-or-flight tendencies are causing some investors to follow the herd into costly mistakes.

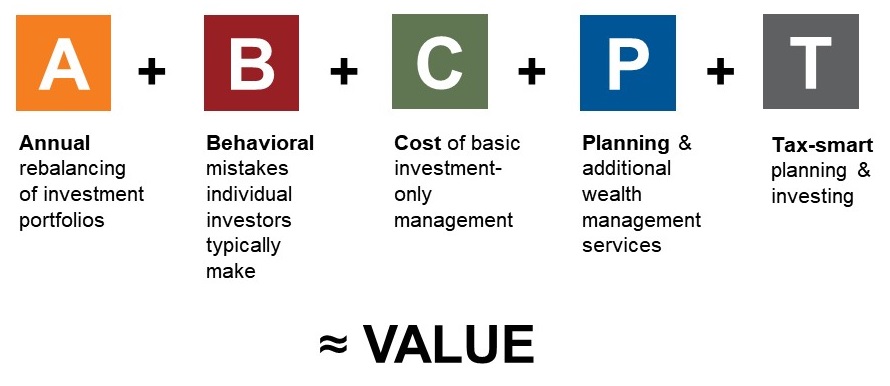

Dedicated advisors are not walking away from these challenges. Instead, we see many of them wading into the fray and working hard to keep their clients’ life savings intact. And as the volatility batters many investors’ savings, advisors may be challenged to articulate that the value they deliver goes over and beyond selecting and managing investments. That’s why it’s so important to provide a simple, easy-to-follow equation that shows the full value of an advisor’s services. It’s as easy as ABC, and then some:

Value of an Advisor = A + B + C + P + T

Click image to enlarge

A is for Annual rebalancing

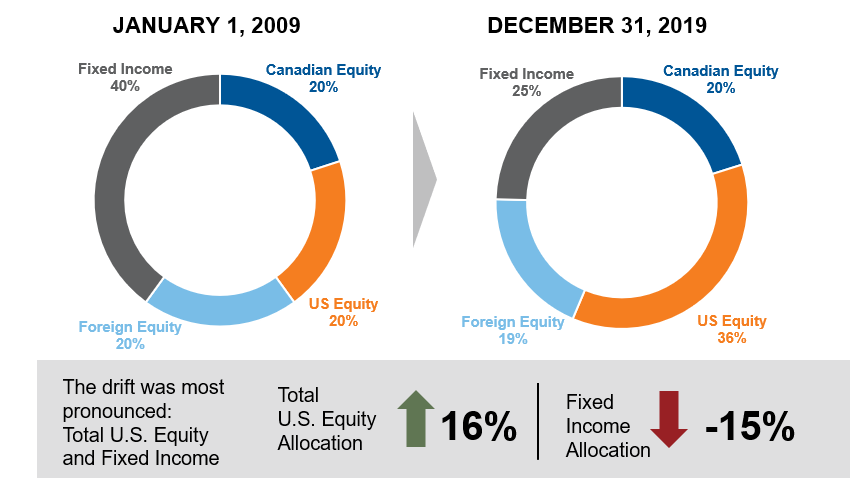

There have been few times in modern history when the topic of rebalancing has been hotter than it is right now. When markets are rising, it can be easy to underestimate the importance of disciplined rebalancing. But this year, in the face of rarely seen volatility, it’s obvious that rebalancing is vital because it is designed to help investors avoid unnecessary risk exposure. Imagine you have a hypothetical balanced index portfolio that has not been rebalanced. In certain market conditions, it could end up looking more like a growth portfolio and expose the investor to risk they didn’t agree to. The annual rebalancing an advisor provides can help keep that from happening.Historically, rebalancing to fixed weights causes one to sell equities and buy bonds. For this reason, a 2020 portfolio today has likely fallen less than had it not been rebalanced over the past 10 years.

Asset allocation drift of a hypothetical diversified portfolio

Click image to enlarge

Source: Russell Investments Canada Limited. Original Portfolio Asset Mix: 40% Fixed Income (FTSE Canada Universe Bond Index), 20% Canadian Equity (S&P/TSX Composite Index), 20% US Equity (S&P 500 Index), 20% Foreign Equity (MSCI EAFE Index). Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

For skilled investors and advisors, rebalancing may seem obviously vital, especially this year. But we believe there are two reasons that many investors don’t rebalance if left to their own devices:

- Because it’s an easy thing to forget to do. Investors know they’re supposed to do it. We also know we’re supposed to regularly change the batteries on our smoke alarms. But do we really do it?

- Because, in many cases, rebalancing may be the equivalent of buying more of what’s been hurting my portfolio and selling what’s been doing well. Right now, as I write this in the midst of a volatile market, it may seem counterintuitive to buy more equities. But, as a disciplined rebalancer, I know that, over long histories, stocks have the potential to outperform bonds, with some of the best returns on stocks following large market drawdown.

B is for Behavioral mistakes

Behavioral mistakes cost real money. We believe they are causing many investors to suffer significant long-term losses right now. This year in particular, we believe behavior coaching is one of the most vital parts of the advisor job description. And when it comes to delivering value, avoiding behavioral mistakes may be the most significant contributor to total value.

You've likely heard many comparisons between the current markets and the Global Financial Crisis in 2008/09, so keep this fact in mind: From September 2008 to December 2019, $100,000 that remained invested in a balanced portfolio of 60% equity and 40% fixed income would have doubled in value. Meanwhile, had that $100,000 been moved to cash in September 2008 and remained in cash, it would have only marginally risen to $101,846. Left to their own devices, many investors may pull out of the market at the wrong time. Helping them stick to their long-term plan is one way that advisors provide substantial value.

Benefits of staying invested through market turmoil

Click image to enlarge

Source: Russell Investments, Refinitiv DataStream. In CAD. Balanced 60/40 portfolio: 20% S&P/TSX Composite Index (Canadian equities), 20% S&P 500 Index (U.S. equities) 20% MSCI EAFE Index (international equities), 40% FTSE TMX Canada Universe Bond Index (Canadian fixed income); Cash: S&P Canada Treasury Bill Index. This hypothetical example is for illustration only and is not intended to reflect the return of any actual investment. The 60/40 Balanced portfolio does not reflect a deduction for expenses or fees, had it done so, returns would have been lower. Indexes are unmanaged and cannot be invested in directly. Past performance is not indicative of future results.

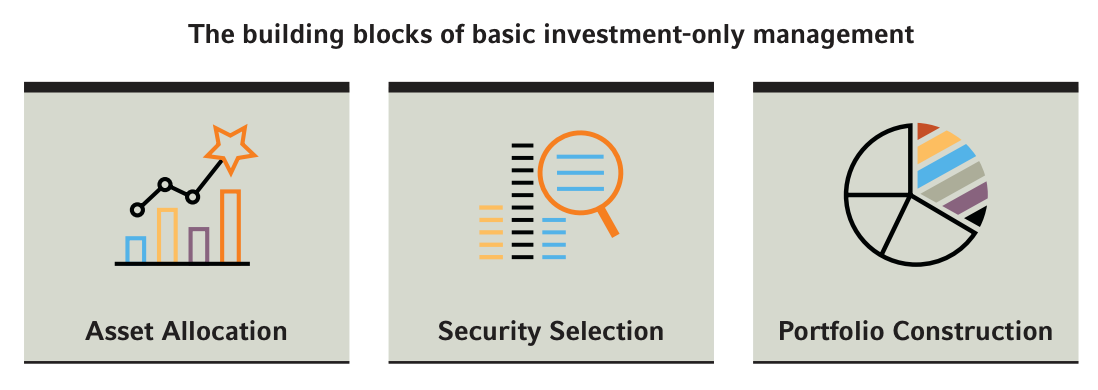

C is for Cost of investment-only management

What is a bare-minimum investment management worth? What would investment management cost if a robo-advisor did it? And what does a robo-advisor deliver?Click image to enlarge

Most robo-advisors that deliver investment-only management and no financial plan, no ongoing service, and no guidance, still charge something, even if it’s just for annual statements, online access, and a phone number to call in case of questions. Are you making sure your clients acknowledge that you provide investment management as only one small part of your offering?

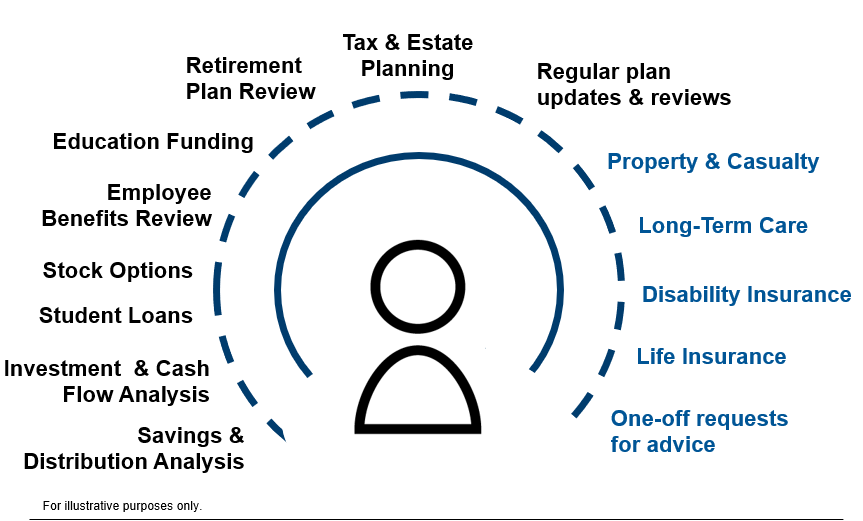

P is for Planning costs and ancillary services

By this point in 2020’s volatile markets, you’ve probably seen commentary on how important it is to stick to a long-term investment strategy. The sound financial planning that advisors provide is designed for times just like this. And we believe it has never been more valuable.

As obvious as this sounds, it’s worth stating that financial advisors add value by doing the hard work of shepherding a strategy from origination to outcome—through all kinds of market events—even global pandemics. Per a recent financial planning study conducted by Kitces, the average standalone planning fee for a comprehensive plan was around $2,0801. Are your clients aware of that value? They should be.

And what about the ancillary services you and your team offer? We believe advisors and their staff consistently underestimate the value of the ancillary services—insurance needs, custom requests and questions—they may provide their clients. These additional services can quickly consume 20, 50, or 100 hours each year. Make sure your clients consider what those professional hours are worth.

Planning and ancillary services advisors may provide

Click image to enlarge

1The Kitces Report Volume 2, 2018 and the “How much does a comprehensive financial plan actually cost?” April 8, 2019 article from kitces.com

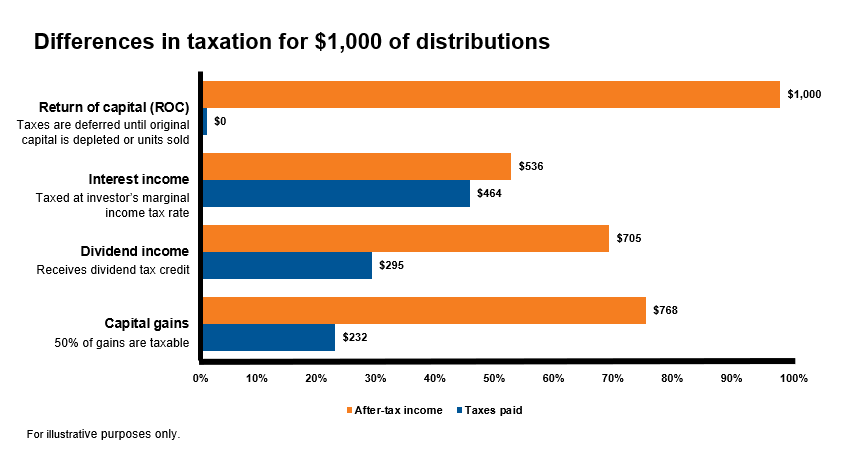

T is for tax-efficient investing

Believe it or not, taxes have the ability to seriously erode returns—even in a down year. While downward fee pressure can mean downward value trends in other areas, advisors who focus on tax-efficient investing can distinguish themselves and demonstrate differentiating value. Because it’s not what you earn. It’s what you get to keep.

Tax-efficient advisors can help add value by helping build and implement a personalized, comprehensive and tax-efficient portfolio. Reducing the impact of taxes on investment returns may help achieve better outcomes. Deferring taxes into the future has the potential to significantly compound returns over time.

An advisor who considers the impact of taxes can help structure a portfolio to minimize the tax payable on distributions or defer taxes into the future.

Click image to enlarge

All examples shown are based on the following 2020 Ontario marginal tax rates for calculating the tax liabilities: interest income = 46.4%, Canadian eligible dividends = 29.5% and capital gains = 23.2%

The bottom line

Market volatility, economic downturns and uncertainty make today’s investing environment one of the most challenging of our lifetimes. At Russell Investments, we believe the role advisors play has never been more vital. When else have investors had a greater need of a counselor and guide to help them navigate these issues? This annual Value of an Advisor study quantifies that dedication and the resulting benefit.

Advisors, we believe in your value. We see the advantages you create for your clients. We know the commitment you bring to your relationships. So stand tall. You’ve never mattered more.