T is for being a tax-smart advisor throughout the investment process

Taxes matter. Imagine your paycheck if income taxes weren’t deducted. Imagine how the price of a car or major appliances or a nice shirt would change if the invoice didn’t include sales or excise taxes.

Many investors don’t realize that the same applies to an investment portfolio.

Taxes are a cost when it comes to investments. They are a drag on a portfolio’s returns. In essence, taxes are like a government fee being applied to investment portfolios.

We believe advisors who take taxes into consideration when constructing an investment portfolio can play a significant role in helping minimize the impact of taxes on their clients. And we believe that has significant value.

This is the fifth and last blog in this year’s Value of an Advisor series, each of them taking a deeper dive into our easy-to-remember formula:

Click image to enlarge

In this blog, we are going to look at the value an advisor can provide when they consider taxes throughout the investment process. We’re not just talking about tax-loss harvesting or deferring capital gains taxes. We’re talking about using tax-loss harvesting as a way to offset the tax impact of realized capital gains. We are talking about minimizing the tax cost of dividends as well as interest payments; carefully timing and managing portfolio turnover and trading activity and maximizing the use of tax-lot level accounting, among other strategies. Even asset location within a portfolio holds the potential to affect after-tax success.

Managing the impact of taxes on a portfolio could take on even greater importance in the next few years as the cost of the support programs related to COVID-19 will eventually need to be paid for.

Advisors who work closely with their clients and clearly understand their goals, preferences and circumstances will have a better idea of which registered plan – a Registered Retirement Savings Plan (RRSP) or a Tax-Free Savings Account (TFSA) -- would best meet their future needs. An advisor can provide their clients with information about the contribution and withdrawal rules that govern a Registered Education Savings Plan (RESP) or how to access RRSP funds under the Home Buyers Plan. Advisors can also discuss how a client can convert an RRSP to a Registered Retirement Income Fund (RRIF) the year they turn 71. Or, if they are being laid off, how best to take their pension benefits – lump sum or deferred?

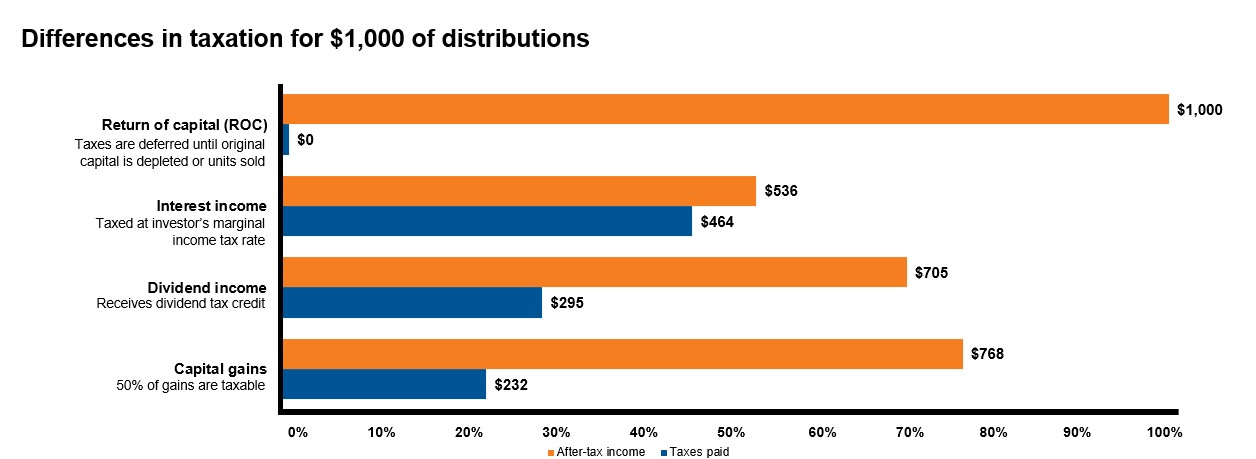

Given the different types of tax rates on different types of distributions from an investment, advisors can help clients minimize the tax bite by channeling different investments into the right structure.

'Click image to enlarge

For illustrative purposes only. All examples shown are based on the following 2021 Ontario marginal tax rates for calculating the tax liabilities: interest income = 46.4%, Canadian eligible dividends = 29.5% and capital gains = 23.2%

Corporate class funds can be especially beneficial to high net-worth individuals, small business owners, retirees who want to draw down a regular income without impacting their Old Age Security (OAS), and parents or grandparents setting up in-trust accounts for minor children or grandchildren. Advisors who are knowledgeable about the corporate class structure and its ability to provide distributions in the form of Return of Capital can help their clients reduce their tax burden in certain situations.

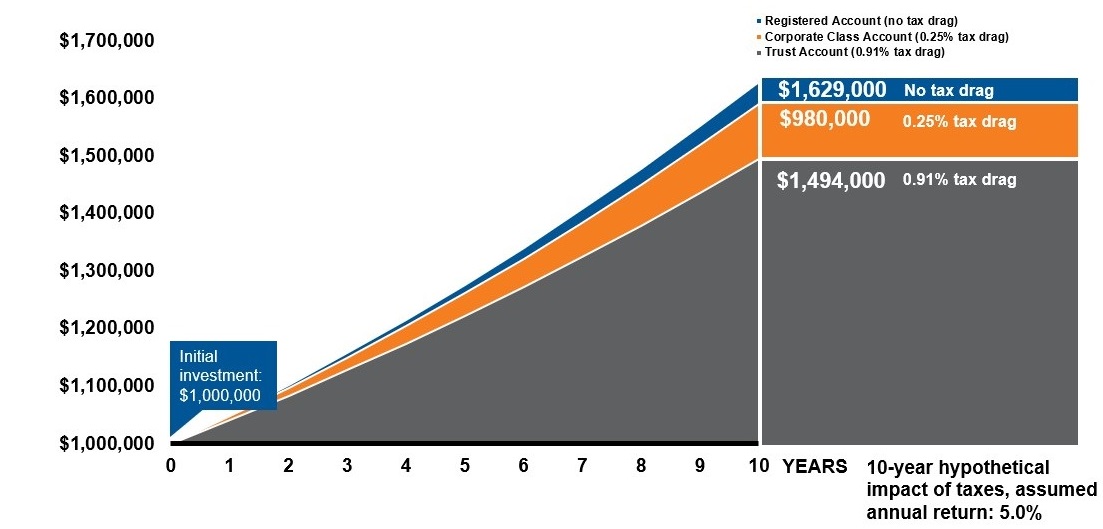

There is a possible long-term advantage of being smart about taxes on investments. As you can see from the chart below, removing the tax drag through registered investments or corporate class funds can substantially impact a portfolio’s return. We believe that advisors who help their clients maximize their after-tax returns can potentially add meaningful value.

Click image to enlarge

Source: Russell Investments

Assumptions: C$1 million investible amount. 5% rate of return for "Registered Account", 4.75% rate of return for "Corporate Class Account*, 4.09% rate of return for '"Trust Account". After-tax distributions are re-invested. Tax "drag" is the difference between the returns on the "Registered Account" versus "Corporate Class Account" or "Trust Account". For illustrative purposes only. Not intended to reflect any actual portfolio or Russell Investments Canada Limited product. Percentages represent the difference in the gross return and after-tax return for trust and corporate-class mutual funds.

For advisors who wonder if they are helping their clients minimize their tax bill, we encourage them to answer these five questions:

- Do you KNOW each client’s marginal tax rate?

- Do you PROVIDE intentionally different investment solutions for taxable and non-taxable assets?

- Do you EXPLAIN to clients the benefits of managing taxes?

- Do you PARTNER with local CPAs to provide the most appropriate tax structure to your clients?

- Do you REVIEW your client’s tax statement?

We all know the historic government stimulus packages that got us through the COVID-19 pandemic will have to be paid for someday. That means it’s likely that taxes are going to go up in the future. Helping your clients structure their investments in the most tax-efficient manner possible can have significant value.

Communicate your value

This is the final installment of our 2021 Value of an Advisor series. Unless advisors communicate the value they provide, their clients may not be fully aware of all the benefits they receive by working with an advisor. After all, your value is only as good as the client experience that you are reliably delivering, clearly communicating, and constantly elevating.

So then, what are you going to do to elevate your value? Considering taxes through every phase of the investment process might be your best place to start.

To learn more about the 2021 Value of an Advisor Study, click here