3 guidelines to keep in mind in volatile markets

We are faced with headlines every day that force us to consider bailing on investments when markets get jittery. Whether it’s a global pandemic, trade war talks or a looming election, the news can be very distracting.

It’s important to remember to stick to your long-term financial plan and avoid emotional, headline-driven decisions. To help ease some of the angst, consider these three guidelines to help you keep things in perspective, and stay calm and invested.

On days where headlines are alarming and investors like you are wondering what’s happening to your savings, it’s more crucial than ever to focus on the bigger picture and your long-term goals. At Russell Investments, we believe that investors can avoid missteps that can lead to bigger shortfalls than they are already facing. Recent events have served as a reminder of this. Investing can be uncomfortable for a lot of people, but does it have to be?

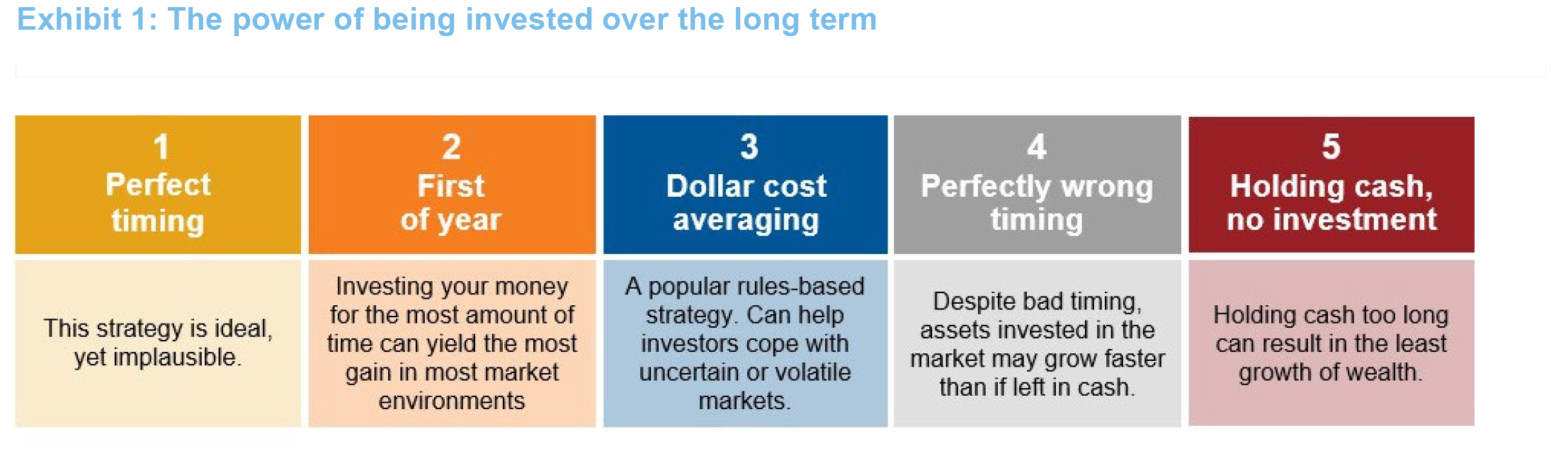

1. No one can really time the market

Even the most sophisticated investors will tell you that it is virtually impossible to consistently and accurately predict the market’s short-term moves. In fact, mistiming can be disastrous to investment returns. In a low growth/low return environment, what does this mean for investors saving for retirement? In today’s reality, where investors are more likely than ever to face retirement income gaps, they can’t afford to miss out on returns.

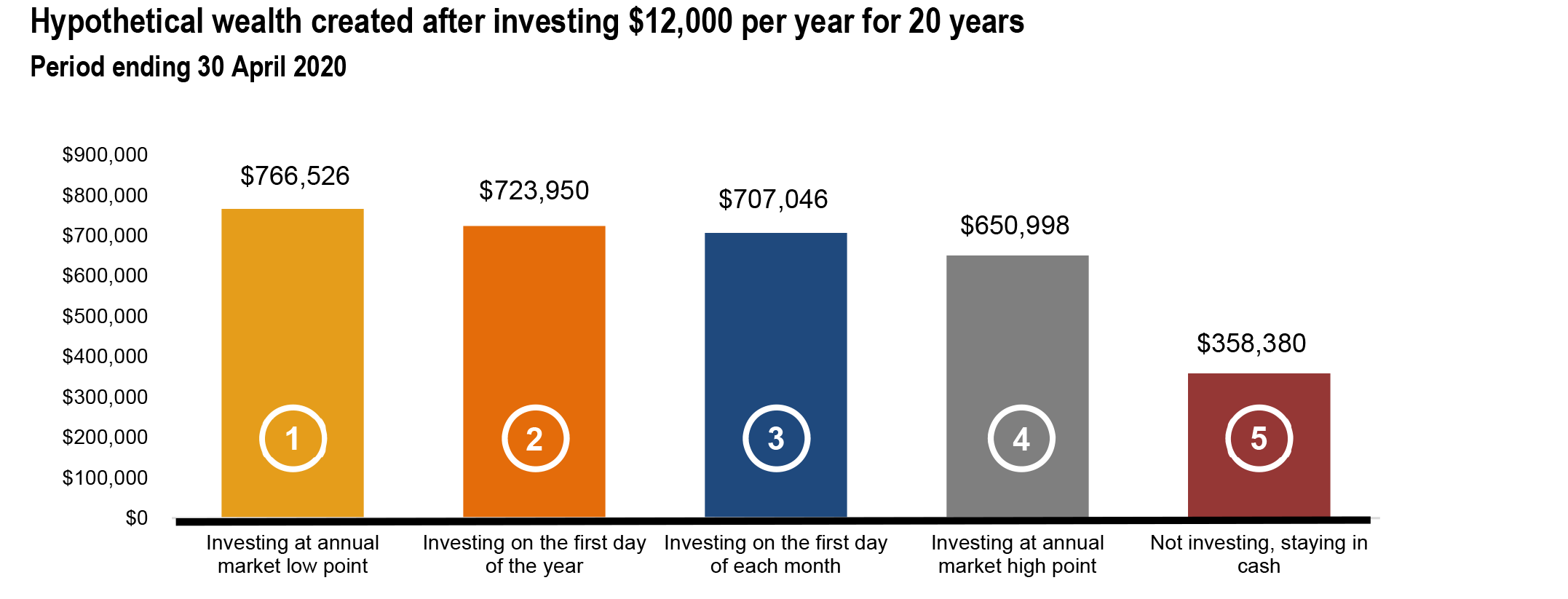

We believe in the power of being invested over the long-term. Not being invested and leaving money in cash (strategy #5 in Exhibit 1), yields by far the worst ending wealth of any investment option. Even investing your money on the worst days of the market (strategy #4 in Exhibit 1) is still more favorable than not investing at all.

2. Nothing, especially volatility, lasts forever

Throughout history, there have been many times where markets have declined—but these relatively short periods are most often followed by the most favorable returns. Unfortunately, due to loss aversion1—one of the principles of behavioral economics—people tend to remember the bad twice as much as the good2. This means that despite having experienced the longest bull run in history3, even a few bad days in the markets can cause investors to rethink their long-term investment strategy.

Since 1963, NZ stocks have more often finished the calendar year in positive rather than in negative territory—in fact, 70 percent of the time, as evidenced in Exhibit 2.4 It’s extremely challenging to predict whether a calendar year will be positive or negative.

Note that one year represents a 12-month period ending the last day of April each year.

Assumes a one-time investment of $12,000 per year into the S&P/NZX 50 Index (representing New Zealand equities) with no withdrawals between April 30, 2000 and April 30, 2020. Cash return based on return of $12,000 invested each year in the NZX 90-day bank bill index (representing New Zealand cash) without any withdrawals between April 30, 2000 and April 30, 2020. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Source: Russell Investments. Hypothetical analysis provided for illustrative purposes only.

3. Diversification matters

The very point of diversification is to limit downside losses in difficult markets. If a market correction happens and you’re properly diversified, you’ll be less likely to lose a substantial amount and less likely to sell at the bottom. Working with your financial adviser or financial professional and having a robust strategic asset allocation with regular rebalancing, can potentially enhance returns, but more importantly, help manage volatility. Put simply, investors diversify because the future is uncertain, and no one can predict with certainty which asset class will win or lose over the upcoming market cycles.

Represented by the NZSE40 from 1963-2002 and S&P/NZX 50 from 2003-2019 (total: 1963-2019). Source: Russell Investments.

Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

The bottom line

While navigating uncertainty and extreme market volatility is difficult, it’s important to keep the big picture in mind and stay focused on your long-term goals. Volatility is inevitable even in positive markets, and diversification is a tool every investor can rely upon to help withstand market corrections. Rather than reacting to volatility and trying to time short-term market gyrations, Russell Investments believes that investments should be based on personal long-term goals, time horizon, financial circumstances and risk tolerance, not on what markets are doing at a given moment. Economic uncertainty will always be a cause for anxiety, so it’s important to remember these guidelines and either speak with your financial advisor or seek professional financial advice, especially when the markets get choppy.

1 Loss aversion is people's tendency to prefer avoiding losses to acquiring equivalent gains.

2 Source: Seeking Alpha: The Persistence of Aversion: Why Investor Pains Hurts Twice. https://seekingalpha.com/article/4240745-persistence-of-aversion-why-investor-pain-hurts-twice

3 Bull markets are markets where the cumulative return exceeded 20%.

4 Represented by the NZSE40 from 1963-2002 and S&P/NZX 50 from 2003-2019 (total: 1963-2019). Source: Russell Investments

5 John Templeton learned to put his eggs in different baskets, by Sushruth Sunder. https://www.financialexpress.com/market/how-legendary-investor-john-templeton-learned-to-put-his-eggs-in-different-baskets/847894/