Amid funding concerns, do non-profits need to re-evaluate their investment strategies?

Key takeaways:

- With many U.S. funding policies under review, non-profits are facing budget uncertainties

- As a result, some organisations should consider making changes to their investment strategies

- In some circumstances, an increased allocation to private markets may make sense, and in others it may need to be decreased

- In other instances, organisations may want to consider creating a shorter-term investment portfolio to fund near-term outflows

The outlook for non-profits is murky. But does this mean a change in investment strategy is worth considering?

During times of uncertainty, we generally believe investors should stick to their strategic policy allocation and delegate any short-term adjustments in positioning to an investment manager. Doing so helps ensure that any tactical adjustments align with an investor’s goals—and not their emotions.

But for some non-profit organisations right now, concerns around market uncertainty are being compounded by concerns around budget uncertainty. Why? The federal government has historically been a key source of funding for many non-profits, and with many U.S. funding policies under review, there’s concern that access to federal dollars may change.

Does this mean a change in investment strategy is warranted? Our answer: It depends. If an organisation’s finances are affected by budget cuts, this will likely impact the magnitude of their portfolio net outflows. Correspondingly, the amount of risk they’re willing to take or the amount of return needed from their investments may change. For these organisations, a holistic review of their investment strategy is likely warranted.

There are many factors to consider when re-evaluating an investment strategy—and they will vary by organisation. To help guide non-profit investors, we’ve come up with broad considerations for three different sets of potential circumstances:

- Permanent, but manageable, increase in portfolio outflows

- Permanent, and significant, increase in portfolio outflows

- Transitory budget changes

Permanent, but manageable, increase in outflows

We believe organisations looking to maintain the value of their investments amid a permanent—but manageable—increase in outflow expectations should focus on finding additional sources of return and diversification. This can allow them to continue meeting their funding goals without a notable uptick in portfolio volatility. The exact considerations for change in investment strategy will vary depending on the makeup of their current portfolio.

The first thing to consider is the allocation to alternative assets. Private equity can play a key role in boosting returns, while private credit, private real assets and hedge funds can serve as key diversifiers and also offer potentially enhanced returns. For investors with a higher tolerance for illiquidity, we think an introduction or increase in alternative investments is worth considering. For those that already have large allocations to private markets, we think they should stress-test their liquidity to ensure this allocation is still appropriate given their new liquidity needs.

For some organisations, it might be prudent to increase the overall allocation to growth assets, rather than just leaning into alternatives.

All organisations looking to enhance returns will need to consider how to manage total-portfolio volatility. Given recent changes in the stock-bond correlation—in 2022, stock and bond prices started moving in tandem—fixed income can’t solely be relied on to manage against the downside in all equity market pullbacks. This is why we think it makes sense to explore alternative sources of portfolio diversification, such as active long volatility and trend strategies. These strategies can help manage downside risk in the event of equity losses without relying on a negative stock-bond correlation.

Permanent, and significant, increase in outflows

Unfortunately, if the increase in required outflows is large enough, a required change in policy may be necessary for non-profits. At a certain point, it is difficult to expect investment returns to be able to keep up with outflows. It is typically considered extremely difficult to target maintaining purchasing power in perpetuity once annual outflows exceed 6% of the investment pool.

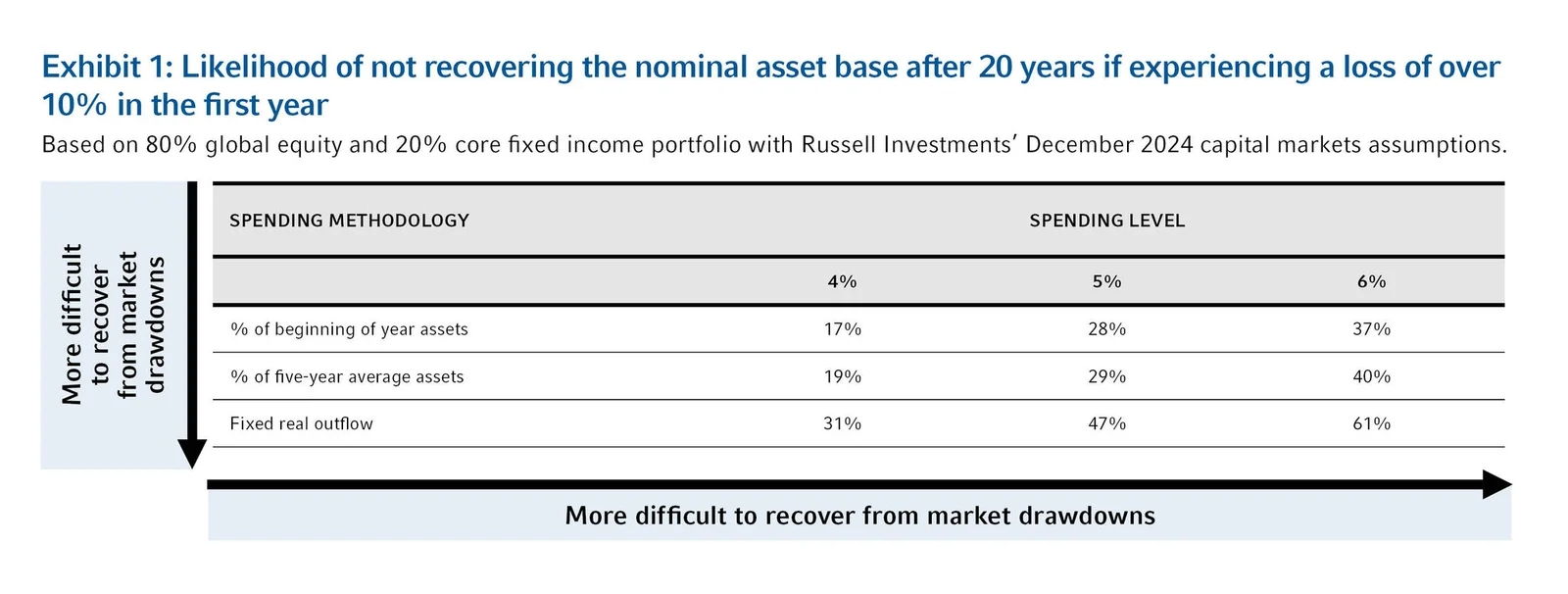

In addition, investors often reach a point where the magnitude of the outflows is high enough that concerns on crystallising near-term losses become more important than the desire to generate returns. This can lead to further de-risking. If expected outflows go beyond this, the ability to tolerate investment losses will be further impacted by spending controls—specifically, the organisation’s ability to reduce spending after market losses. The harder it is to make adjustments to spending levels, the less investment volatility can be tolerated, as shown in the following exhibit.

Organisations in this category likely face the most difficult questions, as there will not be a one-sized-fits-all answer. For some organisations there may be a desire to reconsider long-term objectives and lower risk to reduce the potential shortfall. Others might maintain a high-risk posture to maximise the possibility of maintaining the value of their investments. In all instances, organisations with an allocation to private investments should stress-test their portfolio’s liquidity to ensure the size of their privates allocation is still appropriate.

Transitory budget changes

In the event of a transitory—but material—increase in outflow expectations, it could be prudent to create an additional investment portfolio specifically designed to fund the near-term outflows. Assuming that the primary investment portfolio is growth-oriented, it’s likely taking on levels of risk that are prudent based on original outflow expectations. Significantly higher outflows lead to the possibility of greater crystallisation of losses in a market downturn, which could make such a level of risk inappropriate.

In order to prevent this, we think it’s a good idea to maintain the strategy of the initial investment pool as is and create a shorter-term investment portfolio specifically to fund these outflows. This aligns the risk profile of the shorter-term investment portfolio with the expected timing of the outflows. Although the strategy of the initial investment pool is left unaltered, if it holds illiquid investments, the outflow to fund the short-term pool will likely leave it overweight illiquid investments. This means an implementation plan will be necessary to bring the portfolio back in line with its strategic asset allocation.

Depending on the organisation’s tolerance for risk, if there is a transitory but manageable increase in expected net outflows, it could lead to no changes in investment strategy, the creation of a small short-term pool or the holding of additional short duration bonds.

Implementation considerations

Once a new strategy has been decided, implementation is next. We typically think using a dollar-cost-averaging schedule is best, in order to minimise market risks. If the new strategy is leading to a moderate de-risking or an increase in growth risk, there are a wide variety of implementation times that could be appropriate. However, if there is a need to de-risk significantly, it is typically more appropriate to expedite the changes.

It's also worth noting that any increase or decrease in the desired level of private markets exposure will take time. Until the private markets allocation is at its target weight, adjustments to the liquid portion of the portfolio should be carefully weighed. When building the private markets portfolio, the additional liquid assets could be focused on growth to attempt to try to replicate returns with public markets. Or, they could be invested in a more balanced approach to target the expect risk level of the future portfolio.

If the allocation to illiquid investments needs to be reduced, we believe there should be discussions to determine preferences. For example, is the organisation’s preference to keep the overall allocations in line with broad level investment targets? Or is there a need to de-risk the liquid portfolio to ensure higher levels of liquidity?

In all circumstances it is important to remember that illiquid investments come in many structures. Due to the flexibility introduced by different structures, this should be a factor in determining the appropriate allocation to less liquid investments. Not all private investments are the same, and a need to increase liquidity should not necessarily lead to equal reductions in all private investment targets.

The bottom line

With rumors of potential funding cuts swirling in the headlines, we believe now is a good opportunity for non-profits to review their objectives and ensure their investment strategy is optimised to the future needs of the organisation.

An increase in required outflows from the investment pool may only require slight adjustments in investment strategy, or it could require a complete re-thinking of objectives and the purpose of the investment pool. But no matter the situation, no potential tool or strategy should be overlooked.