Equity Factor Report - Q3 2024: Value and low volatility strategies rally

Executive summary:

- In a stark reversal from the first two quarters of 2024, among Russell Investments Factor Portfolios, Global Large Cap Low Volatility, Size and Value outperformed the benchmark for the third quarter while Global Large Cap Quality, Momentum and Growth underperformed.

- During the third quarter, the rise in correlations between the Value factor and the Low Volatility factor in Russell Investments Factor Portfolios—which had been observed over the past year—leveled off.

- The choice of metric used within factor portfolios to manage carbon exposure risk typically has minimal impact in broad-based benchmarks, with the exception of some value portfolios.

Overview

In anticipation of interest rate cuts, investors buoyed Small Cap and Value stocks to kick off the third quarter, with the rally fading as the quarter progressed. Small Caps handily outperformed their Large Cap counterparts across the U.S. and Developed ex-U.S. regions. The Russell 2000 Index (+9.3%) outperformed the Russell 1000 Index (+6.1) and the MSCI ex-U.S. Small Cap Index (10.6%) outpaced the MSCI ex-U.S. Large Cap Index (7.8%). After a sluggish start to the quarter, the MSCI Emerging Markets index finished with a return of +8.9%, with most of that return coming in the month of September (+6.7%). The MSCI All Country World Index (ACWI) had a positive return for the quarter of +6.7%.

When considering Russell Investments’ global factor portfolios (RFPs), Global Large Cap Low Volatility, Size and Value outperformed the benchmark for the quarter with positive excess returns of +2.3%, +1.8% and +0.8%, respectively. Conversely, the Global Large Cap Quality, Momentum and Growth portfolios underperformed for the quarter with excess returns of -1.7%, 1.6% and -1.1%, respectively. The performance of the factor portfolios this quarter is a stark contrast to the prior two quarters where Momentum and Growth were the outperformers.

Exhibit 1: Cumulative excess returns for Global Russell Investments Portfolios vs. MSCI ACWI

Source: Russell Investments and MSCI; Data as of 07/01/2024-09/30/2024.

Factor performance

Global Russell Investments Factor Portfolios’ performance dynamics

The performance dispersion among Global Russell Factor Portfolios (RFPs) this quarter was larger than prior quarters, with dispersions between Value and Growth factors ranging almost +/-5% before coalescing at quarter-end. Growth and Momentum lagged the market for much of July before recovering slightly to finish the quarter off their lows.

Exhibit 2: 10-Day rolling excess returns for Global RFPs vs. MSCI ACWI

Source: Russell Investments and MSCI; Data as of 07/12/2024-09/30/2024.

Russell Investments Factor Portfolios’ performance across regions

In the third quarter of 2024, the performance of the factor portfolios was uniform in some regions and divergent in others. The Low Volatility factor outperformed strongly across all regions against their respective benchmarks, with excess returns ranging from +0.8% to +2.3%. Conversely, the Growth factor underperformed across all regions with excess returns ranging from -0.7% to -1.8%. Similarly, the Momentum factor underperformed their respective benchmarks across all regions with the exception of U.S. Small Cap, which had a positive excess return of +0.7%.

The divergence in performance in Size was along the cap tier spectrum with Large Caps in the U.S., Developed ex-U.S. and Emerging Markets outperforming with excess returns of +0.6%, +2.3% and +0.9%, respectively, while Small Caps underperformed with excess returns of -0.2% for both the U.S. and Developed ex-U.S. regions. The performance of the Quality factor was split between U.S. and ex-U.S. regions, with underperformance in the U.S. Large Cap (-1.9%) and Small Cap (-1.0%) regions and outperformance in both Large Cap and Small Cap Developed ex-U.S. regions (+0.1% and +0.2%, respectively) as well as in Emerging Markets, with excess returns of +0.5%. The performance of the Value factor was mixed, with positive excess returns in Emerging Markets (+0.9%), negative excess returns in U.S. Small Cap and Developed ex-U.S. Large Cap of -1.1% and -0.9%, respectively, and flat returns in U.S. Large Cap and Developed ex-U.S. Small Cap. The weakest performance among factors in all regions for the quarter was in Emerging Markets, where the Momentum factor underperformed (-3%).

Exhibit 3: Excess returns of RFPs vs. corresponding benchmarks

Source: Russell Investments; FTSE Russell; MSCI

Performance of subfactors in the global universe

Exhibit 4 illustrates the performance of various subfactors in the MSCI ACWI universe for the last quarter, represented by top minus bottom quintile portfolios.1 All Value subfactors had a positive return in Q3, reversing a trend from the prior two quarters. The largest positive return for the quarter came from the Free Cash Flow to Price subfactor, with a return of +6.7%. In addition, all Low Volatility subfactors had a positive return as well, with 3-Month Daily Volatility having one of the largest positive returns of the quarter at +5.2%. The performance of all Growth subfactors was strongly negative, with 3-Year EPS Growth Forecast (-8.4%) and 3-Year Book-to-Price Growth (-8.6%) having some of the largest negative returns for the quarter. Similarly, all momentum factors had negative returns, with the largest negative return for the quarter belonging to the 12-month Momentum factor, which had a return of -8.7%. Quality subfactors were also negative across the board, with all factors having a negative return. Among these, Accruals had the smallest negative return at -0.7%.

Source: Russell Investments; MSCI; Refinitiv

Ex-ante correlations and active risk of Global Russell Investments Factor Portfolios

In the third quarter, the rise in correlations between the Value factor and Low Volatility observed over the past year flattened, as illustrated in Exhibit 5. The trend between Size and Low Volatility continued to increase in the prior quarter and is now close to matching a near term high last reached in 2022. Momentum continues to become more uncorrelated to Low Volatility and is now as uncorrelated as Growth and Quality. Ex-ante active risk levels—predictive measures of the active risk associated with factor portfolios in Exhibit 6—displayed a slight trend up over the prior quarter in Value, Low Volatility and Growth portfolios. Even with the recent uptrend, the active riskiness of the factor portfolios is still within a normal level.

Exhibit 5: Ex-ante correlations with Global LC Low Volatility RFP

Source: Russell Investments; Axioma; MSCI; Data as of 01/2016-09/2024.

Exhibit 6: Ex-ante tracking errors of Global RFPs

Source: Russell Investments; Axioma; MSCI; Data as of 01/2016-09/2024.

Spotlight on: Choosing a carbon metric for factor portfolios

Metrics for measuring carbon emissions in investment portfolios, often referred to as portfolio carbon footprinting metrics, play a central role in regulations, net-zero commitments, and building sustainable portfolios. While these metrics face justified criticism, the importance of tracking emissions remains critical, ensuring some version of them is here to stay. Two commonly used metrics, weighted average carbon intensity (WACI) and financed emissions (using EVIC), are often contrasted, though many other options exist. These metrics are increasingly used in a portfolio construction framework, especially when attempting to minimise exposure to carbon risk.

We define and contrast two commonly used measures, WACI and carbon footprint using EVIC, and the different aggregation methods at a portfolio level. Finally, we compare the impact of each approach for the Russell Factor Portfolios.

Comparing WACI and Carbon Footprint

An individual company emits greenhouse gases (GHGs), often measured in terms of Scope 1 and 2 emissions. These "absolute" emissions are raw figures without standardisation. Larger companies, especially within the same industry, typically have higher emissions. Therefore, a carbon intensity metric can offer more insight: for each unit of output, how much does the company emit?

Standardisation brings its own challenges. Ideal sector-specific intensity measures, such as emissions per liter of beverage for Coca-Cola or per ton of steel for ArcelorMittal, work well within sectors but are difficult to aggregate across a portfolio that include companies that are diversified. A more generic standardisation method, like emissions per unit of revenue, becomes useful in this scenario.

Two commonly used methods, WACI and carbon footprint using EVIC, use different metrics to standardise GHGs of each individual security. WACI, widely recommended by the Task Force on Climate-related Financial Disclosures (TCFD), utilises revenue of the security, while the newer "enterprise value including cash" (EVIC) metric, recommended by the Partnership for Carbon Accounting Financials (PCAF), is more often used with carbon footprint because it can be applied for both equity and fixed-income portfolios.

Another difference between the two metrics is the approach used to aggregate emissions across a portfolio. WACI calculates portfolio exposures using portfolio weights and typically relies on a carbon intensity measure at the security level. Alternatively, carbon footprint is measured using absolute emissions and typically aggregates emissions using an ownership share approach before normalising it by the portfolio’s AUM. This method assigns a portion of a company's emissions to the investor based on their ownership or financing share (see below). The main choice here is how to calculate ownership share—historically, market cap was used, but this poses problems for fixed-income portfolios.

Implications for factor portfolios

Despite the differences between WACI and carbon footprint using EVIC, by making one assumption2, we can align the two different data sets for comparison. The difference can be reduced to their choice of denominator—revenue or EVIC.

Exhibit 7 compares the two metrics for companies in the MSCI ACWI universe. The correlation between security-level emissions per revenue and emissions per EVIC is 0.75. This suggests that for a well-diversified portfolio, the choice of metric has minimal impact.

Exhibit 7: Security-level emissions scaled by revenue vs EVIC

Source: Axioma, MSCI, Russell Investments; Data as of 9/30/2024.

We next explore managing carbon exposure risk within factor portfolios to understand the differences that can arise by the choice of metric used. To examine this, we apply a commonly used approach in the industry by constructing a decarbonised version for each of the Russell Factor Portfolios (RFPs) that targets a 50% reduction in exposure while minimising the deviation to the respective factor portfolio using both EVIC and revenue-based measures. We construct two versions of each portfolio, one where sector weights are not constrained in the portfolio and another where sector weights are constrained to a maximum of 5% of active weight versus the benchmark. We test both versions due to the concentration of carbon emissions within sectors such as Energy that can drive a large portion of carbon exposure.

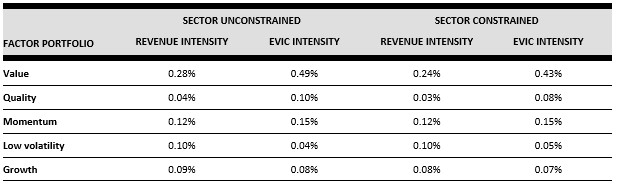

Exhibit 8 shows the ex-ante tracking errors of decarbonised RFPs that target a 50% reduction in carbon exposure when measured against the benchmark. All RFPs except for Value have similar active risk measures regardless of the metric chosen. The Value portfolio, however, has more thana 75% increase in active risk when using EVIC vs. revenue intensity. This increase persists even with sectors constrained.

Exhibit 8: Comparison of quarterly Ex-ante tracking errors of MSCI ACWI Russell Factor Portfolios with decarbonisation constraints versus the benchmark

Source: Axioma, MSCI, Russell Investments; Data as of 09/30/2022 to 09/30/2024.

When applying carbon risk reduction strategies to factor portfolios, the measure used can cause differences in active risk. In broad based benchmarks, the choice of carbon metric is likely to have little impact, except perhaps in value portfolios, which could have a slightly higher active risk when a EVIC intensity measure is used. In addition, since value portfolios tend to have higher carbon footprints, the choice of metric may be more impactful because larger deviations might be required to achieve carbon reduction targets.

1 Top minus bottom cap-weighted quintile portfolios are not investible and are used to proxy the performance of the subfactors used in the construction of RFPs. RFPs are long only portfolios.

2 Note however that to make this simplification we’ve ignored the potentially significant issue of aligning the timing of each of data item. For e.g. in order to divide emissions by revenues in WACI, we align these data items to be pulled from the same financial year, e.g. both taken from FY2021 reporting statements. Similarly, presumably to divide our position by EVIC, these also should have been harmonised to the same date (e.g. fiscal year end). But to do that, we no longer have the equivalence to portfolio weight, which will vary through the year.