The unintentional biases of ESG portfolios

Clients are increasingly asking how they should integrate ESG (environmental, social and governance) considerations into their investment plans. Money managers are responding to that interest with a growing array of ESG products, a range of approaches and increasingly sophisticated messaging.

ESG data can be a valuable input, but our experience and research show that data without context can lead to unintended selection and construction outcomes. We analysed 450 products to highlight the relationship between ESG risk metrics and portfolio exposures. Today, we are presenting the results of our analysis and how Russell Investments accounts for these relationships by evaluating ESG impact and insight through a multi-dimensional perspective.

A growing array of ESG products

Morningstar recently reported that, in 2019, estimated net flows into open-end and exchange-traded sustainable funds that are available to U.S. investors totaled $20.6 billion, a nearly four-fold increase from the prior year 1. Money managers are responding to that interest with a growing array of ESG products and a range of approaches. Many ESG or responsible investing products offer a truly integrated and well-defined investment process. Others simply offer exclusions. Still others claim they’ve “been doing ESG all along” and apply minimal resources and discipline to the exercise.

But, in all cases, we have seen that managers are offering increasingly sophisticated messaging around their capabilities. Without a deep understanding and comprehensive view of the ESG product universe, it is difficult for clients to determine which products will actually deliver the exposures and performance their portfolios require.

What does the data tell us?

Asset managers and investors are increasingly using third-party ESG data as a measure of successful ESG integration when identifying or validating products, but our research and experience shows that ESG data must be handled with care. Russell Investments has been conducting research on ESG data and portfolio tilts since 2013, and while we use third-party data as an input to our manager research and portfolio management processes, we have also developed and incorporated proprietary ESG scores in our solutions. We have found that some measures of ESG risk tend to correlate with other drivers of returns, including size, style and region. As a result, some investment philosophies and products are more easily positioned as ESG simply because of their existing exposures—but whether this represents higher levels of ESG integration is a separate question.

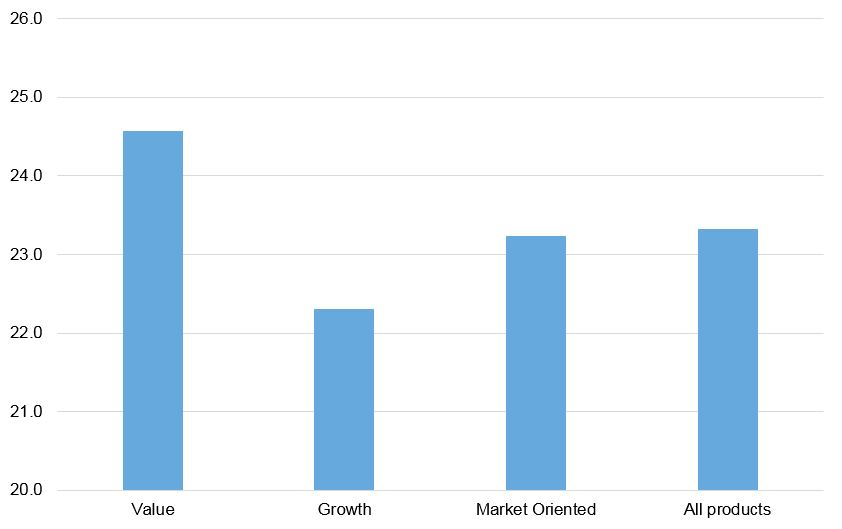

For example, we analysed the average portfolio ESG risk ratings for 449 products in the global and ex-U.S. universes, sorted by style (value, core and growth). We found a statistically significant difference in the assignment of ESG risk ratings according to style, summarised in chart 1 below. Specifically, value strategies have ratings suggesting higher ESG risks than growth strategies.

Chart 1: Average ESG Risk Rating by Product Style

Source: Sustainalytics and Russell Investments

This pattern in the data is at least partly attributable to the types of companies these managers will buy. Value managers are more likely to invest in cyclical industries such as energy and materials, and when grouped by sector, these have the first and third-highest risk ratings. Meanwhile, growth investors are more likely to be overweight technology and consumer discretionary stocks, which have among the lowest risk ratings.

We also conducted research at the security level, ranking the stocks in the MSCI All Country World Index according to their growth factor score minus their value factor score, and found a clear difference between the top and bottom quintiles. Stocks categorised as value stocks using this definition had higher ESG risk than growth stocks.

This means, in a naïve construct, growth strategies will more easily pass as ESG-compliant, and an investor assembling an ESG-friendly portfolio could inadvertently tilt toward growth and away from stocks with a revaluation opportunity.

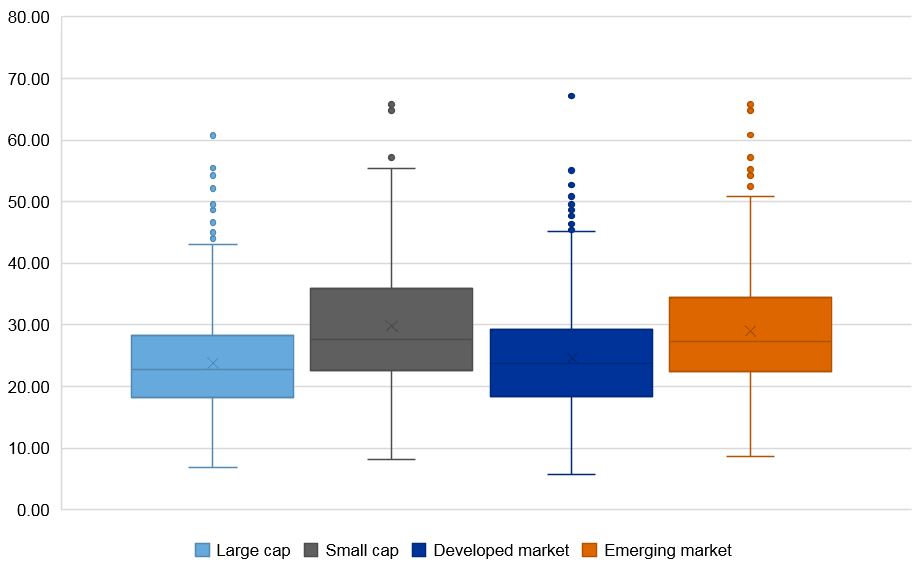

Similarly, our analysis finds that small-cap companies and those domiciled in emerging markets have higher ESG risk scores than large-cap and developed-market companies (chart 2).

Chart 2: ESG risk ratings by size and region

Source: Sustainalytics and Russell Investments

Be wary of a simplistic approach to building an ESG portfolio

It follows that a simplistic approach to ESG positioning that is focused on minimizing ESG risk scores could create a portfolio with unintended biases—toward growth, developed markets and large cap companies.To avoid this, investors looking for an ESG product or portfolio should not rely on product messaging or even messaging in combination with data. What’s needed is a comprehensive view of the ESG product universe and an ability to compare like-for-like managers. In other words, value managers should be evaluated for their ability to identify ESG risks and opportunities among value stocks and against value peers. Our investment professionals are well aware of these biases, and to overcome them, we leverage a multi-dimensional approach to assessing and selecting managers to identify managers that successfully integrate ESG within each region and style.

Multi-dimensional perspective: How Russell Investments assesses ESG integration

At Russell Investments, we evaluate ESG integration from both top-down and bottom-up perspectives to gain a multi-dimensional view of ESG insight and impact.

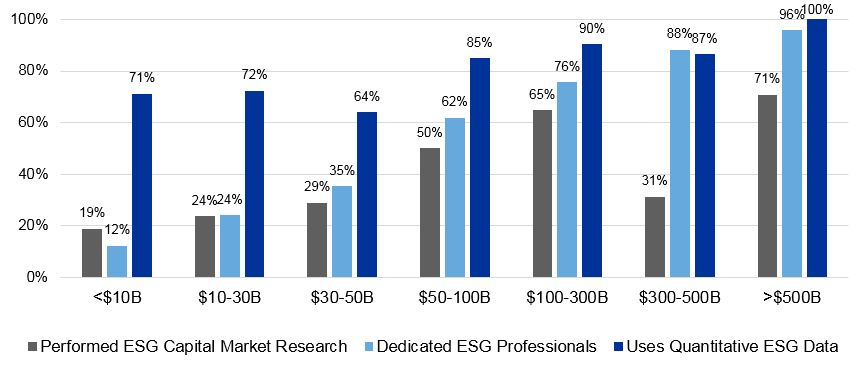

Our annual ESG survey provides us with firm-level information regarding ESG resourcing as it relates to data providers and personnel. As you can see in chart 3, survey results suggest smaller firms, as measured by AUM, are less likely to have dedicated ESG professionals, use quantitative ESG data providers or perform research on the efficacy of ESG integration.

Chart 3: Firms with ESG-Specific Resources

However, to determine an accurate assessment of insight and impact, Russell Investments goes deeper than metrics and messaging. Through product-specific due diligence meetings, we differentiate between firms with true ESG integration and those that are greenwashing2. Our proprietary research reveals some firms that have invested in impressive ESG resources at the firm level do not demonstrate adequate integration at the product level.

Since adding ESG considerations to the manager research framework in 2014, Russell Investments has assigned proprietary ESG scores to nearly 2,000 products across equity, fixed income and alternative products. The depth of our accumulated knowledge allows us to identify a broad set of managers who have effectively integrated ESG considerations into their investment process. In turn, our clients are better positioned to benefit from ESG insight and impact in pursuit of their investment goals.

1 Source: https://www.morningstar.com/articles/961765/sustainable-fund-flows-in-2019-smash-previous-records

2 Merriam Webster: “Making expressions of environmentalist concerns especially as a cover for product, policies, or activities.”