The 2022 List Issue, Part 2: 10 steps for DC plan sponsors to consider this year

Editor's note: This is part 2 in a four-part series on 2022 investment insights. Part 1 can be viewed here.

***

Defined contribution (DC) plans in the U.S. are facing unprecedented challenges. According to an article from Groom Law Group, 2020 was a record-setting year for litigation under the Employee Retirement Income Security Act of 1974 (ERISA), with more than 200 new class actions filed, which is an 80% increase over 2019 and more than double the number filed in 2018. Although the activity in 2021 was off slightly from the pace set in 2020, there continues to be many suits filed for issues such as excessive fees, cybersecurity and imprudent investments.

All of this is occurring at a time in which plan sponsors are coming to the realisation that they must adapt their governance practices to meet the challenge of preparing their participants for retirement. The consequence of inaction is delayed retirement for many, which has a measurable financial impact as a direct result of workforce management complications. Amid this backdrop, many committees are asking what steps they can take in this difficult environment to put plan participants on a path to creating a fully funded retirement income stream.

This blog post reviews key strategies to navigating the onerous legal and regulatory issues faced by plan fiduciaries today, which will understandably take precedent over any other plan consideration. The post also examines tactics to better fund future liabilities - including increasing savings and creating more efficient investment strategies for both active participants and retirees - with an overall objective of increasing the likelihood that employees will have successful retirement outcomes.

Navigating legal and regulatory Issues

1. Review and update plan governance to meet the new challenges

Eliminating all litigation risk and fiduciary responsibility is not possible for a sponsor once it has signed the plan’s original document. There are steps that can be taken to mitigate risk, such as regular fee benchmarking, operating in compliance with the plan document and investment policy statement, and ongoing monitoring of plan investment options. However, such processes will only be successful with a sound foundation. In the oversight of any institutional investment portfolio, like a DC plan, such a foundation is a strong governance process.

An important initial step in the process of improving governance is to establish formal investment beliefs and objectives for the plan. They are considered a core factor in global best-practice models, fundamental to improved governance, and are now utilised by many of the largest plans in the world. Establishing beliefs saves time and allows committees to focus more on managing fiduciary risks, along with strategies to improve retirement outcomes for participants.

2. Improve governance through delegation of investment decision-making

The passage of the SECURE Act in 2019 included reforms intended to broaden plan coverage for employees of smaller companies by allowing them to band together to participate in a single plan, known as either a Pooled Employer Plan (PEP) or Multiple Employer Plan (MEP).

However, MEPs and PEPs are not the panacea that some might suggest for avoiding fiduciary and litigation risks. In these arrangements, employers still maintain fiduciary responsibility for the careful selection and ongoing oversight of the MEP and PEP providers. Further, there is limited flexibility in plan design and in choosing investment options that together may inhibit the sponsor’s ability to make the changes necessary to help their participants. Russell Investments is supportive of committees delegating their investment decisions, but we believe that an internal subcommittee for those with sufficient resources, or an outsourced chief investment officer (OCIO) arrangement, is more appropriate for mid and large sized plans. Similar to a MEP or PEP, the sponsor has responsibility for the selection and monitoring of the provider, but it maintains the flexibility of managing the plan as its own.

3. Cybersecurity

For fiduciary committees, the responsibility to mitigate cybersecurity risks is critical in their efforts to reduce potential litigation. If recent history has shown us anything, it is that when there is an issue with a provider, the plan sponsor will most often be the lead defendant in the class action. To help plan sponsors manage this risk, the DOL included a list of tips for hiring service providers with cybersecurity responsibilities.

However, it isn’t sufficient to simply ask the right questions or gather information from the plan’s service providers. We recommend that fiduciary committees review the responses with their internal IT team, or with a trusted external vendor, to ensure that the provider’s processes are reasonable and considered best-in-class.

4. Environmental, social and governance (ESG)

The recent proposal by the DOL, issued on Oct. 13, 2021, is intended to make it easier for plan fiduciaries to incorporate ESG into their DC plans, including the QDIA, and will likely amend ERISA’s prudence and loyalty standards to make it more difficult for future administrations to change. However, committees are still prohibited from assuming more risk or sacrificing return simply to support collateral objectives.

We believe the most appropriate way for plan fiduciaries to incorporate ESG - while minimising their legal and regulatory risk - is by leveraging ESG integration, which considers factors that have a clear financial benefit. In other words, any ESG consideration should improve the expected risk and return profile of the portfolio. This can be achieved by focusing on investment managers that include ESG integration as part of their process in the same way they may consider valuation, potential growth, credit quality, etc. In addition, as with everything else, plan fiduciaries should ensure they make decisions utilising a well-considered process while documenting everything carefully.

Improving participant outcomes

5. Funding policies for the DC plans

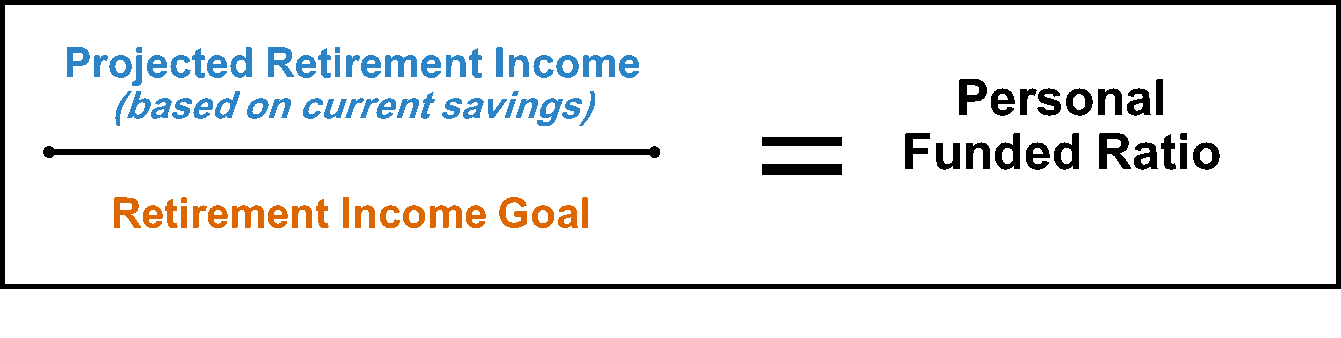

Personal Funded Ratio is a Russell Investments-coined phrase and patented process1 for determining an individual DC participant’s personal retirement readiness based on the asset-liability funded ratio approach used by institutional investors.

Because participants look to their employers to tell them what to do through plan design, sponsors should be using participant inertia to their advantage. Optimising the use of automatic features is among the strategies that likely have the biggest impact in improving personal funded ratios. Much like how organizations periodically review the funding policies for their pension plans, it is critical that employers understand the impact that their decisions (e.g., initial auto enrollment levels and what cap to use for auto escalation) have on funding DC liabilities. Periodic re-enrollment should also be discussed to get non-contributing employees to begin saving and default current participants into a more appropriate asset allocation.

We recommend triennial retirement readiness studies to evaluate progress and determine which levers will have the biggest impact. It is difficult to accurately determine what changes are necessary, or to measure the impact of prior decisions, without establishing the baseline and making periodic assessments.

6. Consider the use of private securities in white label and custom target date fund (TDF) portfolios

The Russell 1000 Index experienced significant drawdowns during both the Global Financial Crisis of 2008-2009 and the COVID-19 pandemic, with peak to trough declines of 53% and 20% respectively. These were painful periods for well-resourced DB sponsors that may have been forced to make additional contributions to improve their plan’s funded status. However, the impact was more significant for DC participants, particularly for those at the end of their glidepath - many of whom were forced to delay retirement.

DB plan fiduciaries have long understood that creating portfolios with the appropriate balance between return seeking and hedging strategies most often leads to success. Since both DB and DC plans are solving for the same solution - fully funding a liability - it seems logical to create portfolios that have the same or a similar asset allocation. DC plans that offer white label portfolios or custom TDFs should consider incorporating similar strategies to help improve the efficiency of their plan’s investment options. Although not suitable as a standalone option, Russell Investments believes a competently managed exposure in a custom TDF or white label fund to illiquid assets has the potential to improve the risk-and-return profile versus comparable liquid assets in many market environments. In order to mitigate legal risks, particularly in light of the DOL’s Dec. 21, 2021 supplement to the 2020 information letter, sponsors considering such an option will want to review these issues with counsel.

7. Rethink core menu design and portfolio structure

Investment committees that still view DC plans as supplemental often emphasize choice over the quality or clarity of investments. However, as fewer employees are covered by a pension benefit, it becomes even more important to have a clear and well-designed core menu to improve the likelihood of successful retirement outcomes. Including both an active and a passive investing tier in a DC plan, in an effort to accommodate the needs of a majority of employees, is a reasonable approach. However, the distinction between the tiers must be communicated to avoid overwhelming participants with too many highly correlated investment choices.

For committees seeking to engage participants and help them achieve better retirement outcomes, we believe that using a multi-manager, white-label structure to consolidate and simplify the plan menu is an appropriate step. Multi-manager, multi-style investing is not a new idea. It’s the way institutional investors, such as DB plans, have been investing for decades. DB plans would never invest all their assets with one underlying investment manager – especially across asset classes, but not even within asset classes. Thus, multi-manager, multi-style investing helps to institutionalise a DC plan.

8. Revisit the Qualified Default Investment Alternative (QDIA)

A vast majority of U.S. defined contribution plans have chosen to use off-the-shelf target date funds as their plan’s QDIA. Target date funds provide a one-stop shop experience by creating diversified portfolios with varying combinations of return seeking and fixed income investments. While they allow participants to avoid making investment decisions from initial enrollment through retirement, it’s important that committees don’t avoid their obligation to periodically evaluate their manager beyond a quarterly review of benchmark relative performance. To assist committees in the selection and ongoing evaluation of their target date fund manager, the DOL issued a series of tips in 2013.

Off-the-shelf TDFs are based on an average U.S citizen, rather than specific investor characteristics. While they have clear advantages over earlier best-in-class solutions, such as risk-based funds, they are only attempting to simplify investment decisions, rather than providing advice on both funding and investing strategies. On the other hand, managed accounts, which are frequently offered in a DC plan, recommend the savings level and investment allocation designed to put the participant on the path to fully fund their retirement. These solutions have also been specifically structured to function as the plan’s QDIA. Just like funding and investing policies for pension plans are unique to each sponsor, DC participants would likely benefit from more comprehensive and personalised advice for more successful outcomes.

An alternative that is starting to garner interest, along with some limited implementation, is a hybrid approach where participants are initially defaulted into a TDF but are then automatically moved, through a secondary default, to the managed account as retirement nears. This approach could be a solution for those committees concerned about the managed account fees for a full-career employee.

9. Provide retirement income solutions for participants in or approaching retirement

The primary focus for DC plan sponsors and committees has historically been on helping participants accumulate assets during their working years, with little support provided in retirement.

However, a flashpoint may be on the horizon. The SECURE Act provides a new fiduciary safe harbor for selecting an insurance provider as a distribution option. Combined with greater product availability, the act appears to be a catalyst, with more committees now expressing interest in evaluating retirement income solutions for their DC plans.

In our view, initial efforts should be focused on participants that appear to be asking for assistance during accumulation. To us, that means committees should first focus on strategies that incorporate automatic or default distribution options in the plan’s QDIA and the managed account option if available.

10. Managed efficient Implementation

Implementation is broadly defined as trading strategies executed by a third-party to mitigate the costs and unintended risk exposures when a committee elects to make a manager change and move among investment mandates. Any asset movement in a DC plan can have serious implications if risk and costs are not carefully managed with thoughtful implementation. In DC plans, implementation comes in many forms, including transitioning assets from one investment manager to another, centralised investment implementation of multi-manager portfolios (i.e. portfolio emulation) or an implementation account within a custom target date fund to improve the trading efficiency of rebalance and roll-down.

We believe that plans should engage with implementation specialists because it is a natural extension of the current focus on fees. The pitfalls of relying on managers to transition assets among mandates are becoming more apparent as DC plans move away from mutual funds to more institutional structures. Efficient investment implementation reduces turnover and trading costs, keeps participants fully invested in the capital markets and avoids blackout dates and performance holidays commonly associated with transitions in DC plans today.

The bottom line

Today’s DC committees face significant challenges in preparing their participants for retirement, which are further complicated by a myriad of legal and regulatory concerns. However, committees must avoid being paralyzed by fear of litigation if they hope to improve participant outcomes. For DC plans to succeed as a vehicle that can help participants reach their personal funded status goals, it is important that committees consider the savings and investment strategies discussed in this blog and prioritise those that will be most impactful.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 U.S. Patent No. 10,223,749 entitled "Retirement Planning Method."