How commodities can play an increasingly important role in portfolio diversification

Managing exposures in 2021

Anything that improves long-term expected return is a benefit in today's environment. But at the end of a long disinflationary cycle to historically low Treasury yields, it is quite possible Treasuries (and entire fixed income allocations) do not provide the full diversification benefit they have in the past. In that event, will an exposure to commodities prove to be the medicine your portfolio needs?

Just a spoonful of sugar¹...

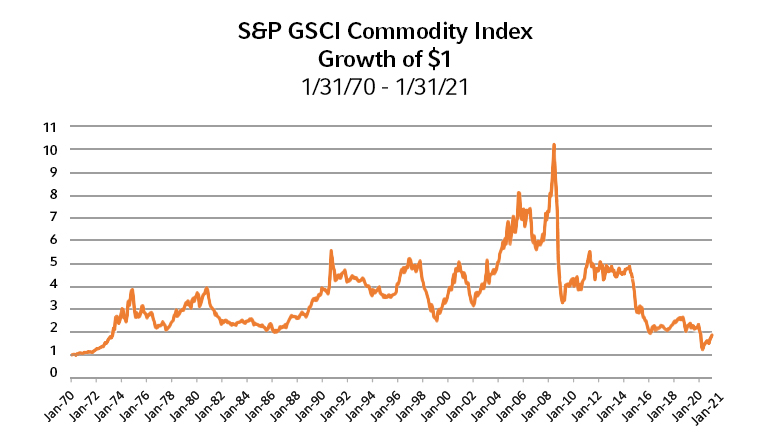

Anyone with a commitment to commodities over the past few decades of prominent disinflationary forces has endured considerable pain. No amount of figurative sugar could cover the bitter taste experienced by a commodity investor that bought and held this exposure since mid-2008. But there have been previous periods where commodities have had very attractive returns. S&P GSCI Index, the most established commodity index, is shown below over the longest period available.

|

Time period |

1/31/70-6/30/08 |

6/30/08-1/31/21 |

|

Years |

38.42 yrs |

12.5 yrs |

|

Annualised return |

6.24% |

-12.69% |

|

Annualised STDV |

18.82% |

23.92% |

Source: Russell Investments, Bloomberg.

In this blog, we attempt to make the case that something that lost over 12% a year on average for more than a decade could play an interesting role in an investor's portfolio.

Diversification concepts revisited

At business school, instructors teach that there is no free lunch. That said, diversification is about as close as you can get to a free lunch in the finance world. The reason it is not entirely free is subtle. In the case of diversifying assets, too much of a good thing stops being good at some point. If something were truly free, we would back up the truck and haul away as much as we could. Over longer periods, commodities tend to have a lower expected return and higher expected risk than equities. Overloading on commodities would be an even worse idea than overloading on equities, but too much of either leads to suboptimal diversification.

The connection between diversification and rebalancing

For most of us, diversification is already delivered by a modern policy portfolio that is meant to deliver better risk-adjusted returns than our primary return driving asset (equities) alone. While the recipes differ from shop to shop, investment consultants forecast asset class returns and the correlation between asset classes - and an efficient multi-asset policy can be created from those key inputs. We talk about diversification all the time, but rarely dive into why it works.

In the first multi-asset role of my career, a mentor of mine gave me an article that captures the magic of diversification and the math behind it well². I will do my best to capture the concepts while sparing you the equations. In short, diversification allows you to create a portfolio with returns greater than the sum of the parts - with the surplus dubbed the diversification return. The catch: This is not a buy-and-hold portfolio. Like your policy portfolio, its return is calculated by taking the monthly return of each asset in the policy times the target weight of each asset. The behaviour of this portfolio is such that it is rebalanced to target every month3, and this implicit rebalancing assumption is key to why the diversification return exists.

What makes an asset a good diversifier?

Volatile asset – This is one case where commodity volatility is good. Volatile price movements generate buy-low and sell-high via rebalancing.

Uncorrelated returns to current holdings - Relative performance deviation between holdings generates the need for a rebalancing trade. Correlation of monthly returns to a portfolio of 60% S&P 500 and 40% Bloomberg Capital Treasury index (60/40) are as follows. This is over a shorter time-period of 31/12/90 to 31/1/21, to allow for comparison of the shorter-lived Bloomberg Commodity Index (BCOM) to Goldman Sachs Commodity Index (GSCI).

Correlation between 60/40 and GSCI was 0.20, whereas 60/40 and BCOM was 0.25. This difference is most likely due to a lower weighting to the volatile energy sector in BCOM. These correlation levels are not dissimilar from Russell Investments' modelled correlation values for global commodities over the next 10 years.

Positive expected return – This allows the position to survive oversight risk as it fulfils its role in the portfolio. Russell Investments' strategic return assumptions⁴ over a 10-year horizon are 3.8% per annum over current T-Bill levels.

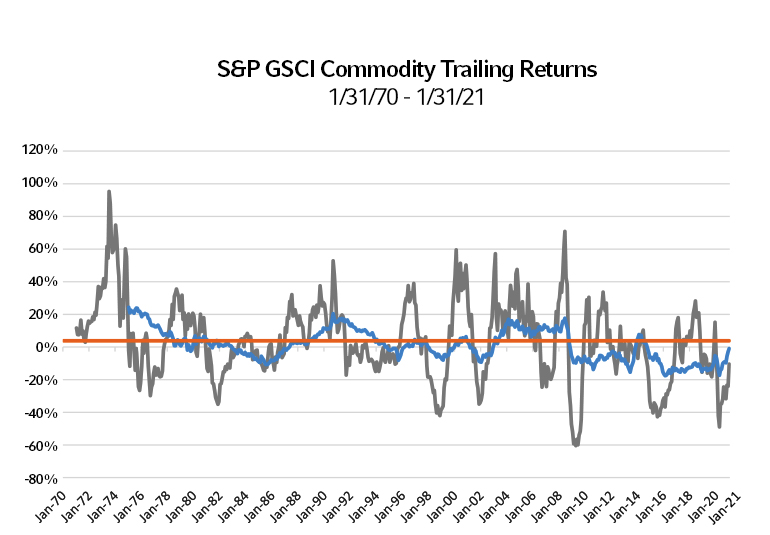

Commodity returns run in cycles, perhaps deeper and longer than equity return cycles. Especially in capital-intensive industries, a weak price environment can linger for years until reductions in capital investment ultimately reduce the supply of the commodity. Particularly depressed are the resource sectors that have declined notably as a share of the overall equity market. Average returns over time are less relevant than the power of being in the cycle when it is in your favour. For this purpose, it is better to look at annualised five-year rolling returns. GSCI is highlighted due to longer history that captures the presence of inflation in the 1970s to better illustrate the environment where commodities could thrive again.

Source: Russell Investments, Bloomberg.

The commodity bear cycle since the Global Financial Crisis has been very deep from a historical perspective. The five-year trailing return (blue line) appears to be moving toward positive levels after a very long time in the negative territory. If this momentum continues, returns to commodities could be much sweeter in the earlier initial years of a rally than for the full 10-year forecast horizon. (orange line).

How do you access such an exposure?

An overlay allows for the addition of unfunded diversifying exposures, in effect by shorting cash exposure (since futures deliver the risk premium to an asset in excess of the financing rate, but not the cash return component). An alternative to using an overlay would involve fully funding commodity exposures. In that case this new diversifier must displace another asset and its expected return contribution portfolio return.

Below is a list of the more actively traded commodities:

- WTI Crude Oil

- Brent Crude Oil

- Natural Gas

- Soybeans

- Corn

- Gold⁵

- Copper

- Silver

Source: Futures Industry Association.

As you can see, the energy complex is at the top of the most-liquid list, but grains and metals also have sizeable markets. Underlying commodity futures contracts can be accessed for more targeted trading, but the simplest way to get exposure is via one of the two most common collateralised commodity futures indexes (weights shown below). While the S&P GSCI index has a longer history, we see a slight preference for the Bloomberg Commodity (BCOM) index from our clients (since it is more diverse and less dominated by energy).

|

Commodity Sector |

S&P GSCI (wgt in %) |

BCOM (wgt in %) |

|

Energy |

53.9 |

30.0 |

|

Grains and softs |

19.3 |

29.9 |

|

Industrial metals |

11.9 |

15.6 |

|

Precious metals |

6.9 |

19.0 |

|

Livestock |

8.0 |

5.6 |

Source: Futures Industry Association.

Either of these can be accessed via total return swap (assuming ISDA documentation in place). S&P GSCI listed futures contracts can be used for smaller exposures or when clients do not have OTC documentation in place, since capacity in this market is much smaller and faces additional risk to maintain exposure (via rolling quarterly futures). Financing levels vary over time, but as of mid-February 2021, long exposure can be accessed at social size of $250 million on either index for 3-month T-Bill rate plus 8-9 basis points. More targeted exposure can be attained at the sector level of each index with social size of $50 million.

Both indexes are calculated based on holding collateralised commodity futures contracts, so return pickup or drag relative to spot commodity prices exists over time. Supply/demand characteristics in each underlying futures market determines whether a given contract has a positive roll yield or a negative carry cost in relation to the underlying spot market in each case.

How much should you hold?

A diversifying asset has diminishing marginal benefit as you add more of it. Clearly, each portfolio has a different starting mix of assets. Given the rate environment and the potential for reflation, a larger fixed income allocation can be offset by more commodity exposure. As a general rule, 2% to 5 % is enough to make a difference. Above that, it requires considerably more strategic commitment to the asset class.

With unfunded exposure (allowing for marginal leverage), an average return pickup would be on the order of 19 basis points on the total portfolio (3.8% return x 5% allocation). In addition, diversification benefit improves with very little incremental expected risk at the total portfolio level. If done funded (without easing the leverage constraint), the expected return pickup would probably come at the expense of diversifying fixed income (Treasuries).

Conclusion

Anything that improves long-term expected return, with little incremental risk, is a benefit in today's environment. Commodities had a challenging bear market up until recently, but they will certainly prove useful if inflation concerns are present due to monetary and fiscal policy stimulus. While commodities seemed to have bottomed for now, stronger deflationary outcomes or default crises typical of a new recession are risks that could delay commodities' upward rebound. In that case, long term Treasury bonds would outperform commodities in the near term, until reflation regains traction. However, at the end of a long disinflationary cycle to historically low Treasury yields, it is quite possible that Treasuries (and entire fixed income allocations) do not provide the full diversification benefit they have in the past. In that event, commodity exposure should prove particularly useful, whether in passive form or with an active alpha-seeking strategy.

Ultimately, your portfolios may be exposed to more risks than ever before. How do you mitigate these risks? Who do you turn to? We have the experience and deep capability set to help you manage your exposures and to help you navigate the challenging road ahead. Let us know how we can help.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

¹ In a 1964 musical movie, Mary Poppins, Julie Andrews sings how a spoonful of sugar helps the medicine go down. Disclaimer: While sugar is an available commodity futures contract, this is not specifically making a case for sugar as an investment, nor stating sugar's superiority amongst the much broader list of sweeteners now available 66 years after the film was released.

² "Diversification Returns and Asset Contributions", by David G. Booth and Eugene F. Fama, Financial Analysts Journal, May-June 1992 edition.

³ Key reason we stress a disciplined rebalancing framework, the policy portfolio gets the benefit of free rebalancing. Mimicking this behaviour in a portfolio attempts to keep up with the policy in capturing this rebalancing return, as well as reducing relative risk to the policy.

⁴ Strategic return expectation not a guarantee of return, actual annual returns will be more volatile around this forecast value.

⁵ Recent Strategy Spotlight (Sahlin, January 2021) highlights how to access exposure to gold.