Confessions of a portfolio manager – # 3: Preparing for a market crash

Crashes exist precisely because they are unexpected. Today David confesses that trying to predict and time the precise future is somewhat futile. We know only one future will come to pass, but as we sit here today many are possible.

Only one future will come to pass, but many are possible

Prepare, don’t predict

Surprises happen when you least expect them to – and that means that I, like many other managers, won’t be able to take down risk assets the day before the next crash. What I do aim to do however, is prepare and protect my portfolios as the probabilities of surprises, or rather, ‘crashes’, rise.

I always get asked by journalists during an episode of weakness “what are you doing” and I tell them that if it was a known event, like the referendum or an election, then the real question should be – ‘what did you do ahead of the event?’. That’s because it is what a portfolio manager does ahead of a market changing event that will determine success. The ability to successfully react and take profitable action after the event becomes smaller and smaller as time passes.

I’m convinced I foresaw the dot com crash

Market declines are always obvious with hindsight. I’m sure we have all seen Michael Lewis’ The Big Short and sat their nodding sagely or screaming at the TV saying, ‘come on!’. Well – and I’m probably going to surprise you here with another confession – I genuinely believe that I saw the tech crash/dot com crash of 2000.

Pre-crash mania

I was only a number of years into my career at that stage, still a ‘text book’ analyst and very naive. I couldn’t understand why companies with no earnings were valued at crazy multiples and had risen by hundreds of percent. I also clearly remember the mania – everyone was taking stock tips from the contracts clerk who was mining tech tip sheets. Even dissenting senior portfolio managers were getting swept away for fear of missing out. However, calling the end and timing the end are two different things, and to be honest – I didn’t call time on the end, but I did think that things were crazy, I recognised something wasn’t right.

The trigger? Boo.com

To me, the end of the bull market happened when boo.com went bust. You may remember it was an internet retailer… Or rather, you probably won’t remember because at that time, only 20% of us had the internet and even fewer still had the speed necessary to be able to make the site function! When it went under with a cash burn of £70m a month, people woke up and the penny dropped. That’s when the selling started.

Despite our efforts, crashes keep happening

And they will continue to happen...

Crashes exist precisely because they are unexpected and cannot be forecasted in a very timely manner. At the crux of this debate is that every bear market is different. Soul searching, regulation and legislation is imposed after each episode, but crashes keep happening. Models are developed to perfectly spot (with hindsight) the last crash, but often the focus point is then not actually correct for the next crisis. The global system is complex and dynamic and so I’m confident that the next crash will result from a separate set of vulnerabilities. That said, the lessons of history are not to be dismissed out of hand. We look at valuations and economics to help us prepare.

Consider valuations – they always mean something

Despite changes in the global system, expensive valuations should still be considered as a warning sign. Today, Schiller’s cyclically adjusted price-to-earnings ratio (CAPE) remains to be the highest its been in over 15 years at 32.43%.1 This indicates the U.S. equity market is currently highly overvalued. It begs the question – is this the end of the bull market? How much further can the U.S. equity market go? Whilst CAPE is not a short-term timing tool (according to Professor Schiller’s own admission), it does help us to shape our expectations for the future. It narrows the funnel of doubt.

Consider economics - vulnerability and resilience depends on the health of the economy

Does studying the economy really work when it comes to preparing for a crash? Well yes and no. Correctly guessing the economic data itself plays a smaller role than some may think, but its study is not wasted as the vulnerability of markets to a shock does depend on the health of the economy. So, monitoring debt levels, leverage, and consumption rates amongst other metrics can prove to be useful.

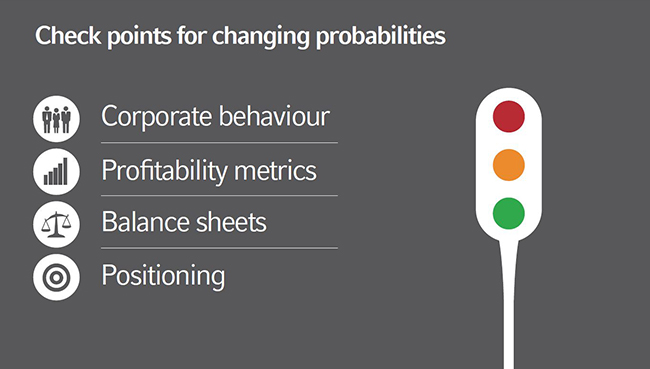

The key? Use check points for changing probabilities

Four main indicators

- Corporate behaviour – Mergers and acquisitions, initial public offerings and buy-backs are always good to keep an eye on.

- Profitability metrics – We run analysis to help us consider whether the corporate profit peaks have been reached, or are close.

- Balance sheet and credit metrics – High debt levels are rarely a good thing!

- Positioning – Knowing where you are in the crowd is a very useful thing. We survey how other managers are positioned to ascertain what the herd is saying.

All these things provide what I like to call the ‘kindling or the fuel’ for a bear market. But, the list isn’t exhaustive. Something is missing, i.e. the spark to ignite the fire is needed – and it is this that is most difficult to predict – like Boo.com or Lehman’s going bust.

My final confession today: There is no perfect answer

Having an awareness of the lessons history can teach us is instrumental in helping to prepare for the next bear market. They help us give an indication towards what needs to be monitored. Stress testing portfolios regularly at the points of most fuel, and leaning away from expensive assets while being mindful of the dangers, can significantly mitigate the losses when they arrive unexpectedly.

It’s likely that we won’t spot the turning point, and this is a fact that should be accepted. But, a good process should have you leaning out of risk assets as returns come down and risks rise.