ESG engagement survey – Creating a complete picture

Executive summary:

- Our 2023 Manager ESG survey reveals that while more investors are implementing engagement and proxy voting strategies, there is still room for improvement.

- The adoption of bespoke voting policies indicate that managers are taking active ownership seriously as an investment tool.

- However, there is still scope for more consistent record-keeping and engagement tracking practices.

Environmental, social and governance (ESG) considerations are here to stay. This was the key takeaway from our Manager ESG survey, which evidenced how investment managers from all major asset classes continue to incorporate ESG factors into their investment processes.

However, investment decision making is only half of the picture, with engagement playing a key role in achieving the full potential of investment objectives. Stewardship and the exercise of ownership rights are invaluable tools in holding issuers accountable to integrating ESG best practices and reporting the results.

For this reason, we dedicate a portion of our survey to active ownership and conduct a deep-dive review of the responses. This informs our industry views and our own practices, as well as our expectations for the investment managers we assess, recommend and hire.

Our research shows that while more investors are implementing engagement and proxy voting strategies, there is still room for improvement.

Engagement

Corporate engagement continues to emphasise environmental, social and governance issues

While our research and observations note rising efforts around active ownership generally and engagement specifically, ESG topics are frequently – but not always – on the agenda. Over 80% of the managers who responded to the survey stated that they hold regular meetings with management, and either occasionally or always cover ESG topics. Since 2021, the percentage of respondents noting that they do not engage or rarely engage on ESG issues has fallen from 9% to 4% in 2023.

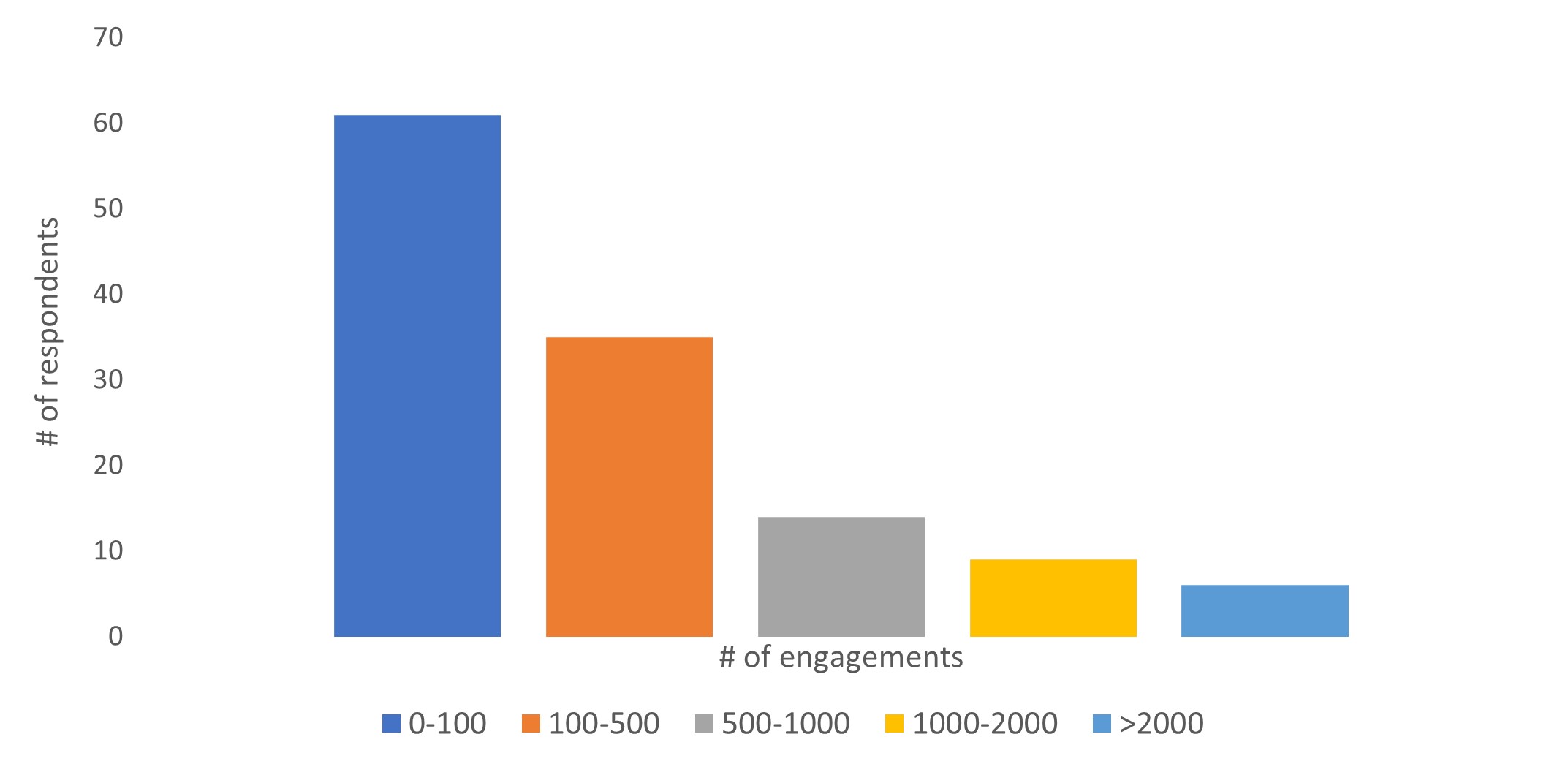

Still no consensus on what defines an “engagement”

In response to the question “How many engagement conversations did your company hold on ESG in the last year?”, respondents provided a wide range of responses, ranging from single digits all the way up to thousands, as shown below:

(Click image to enlarge)

Active ownership applies to all investments

For the first time, managers were asked to disclose the percentage of their firms’ holdings that were subject to active engagement, again defined for respondents as “Active dialogue between investors and companies on environmental, social and governance issues and practices.” Nearly 50% of respondents indicated that they were engaging across all or nearly all of their firm’s holdings. Roughly a quarter of managers who submitted survey responses did not answer this question, suggesting that record-keeping is a challenge.

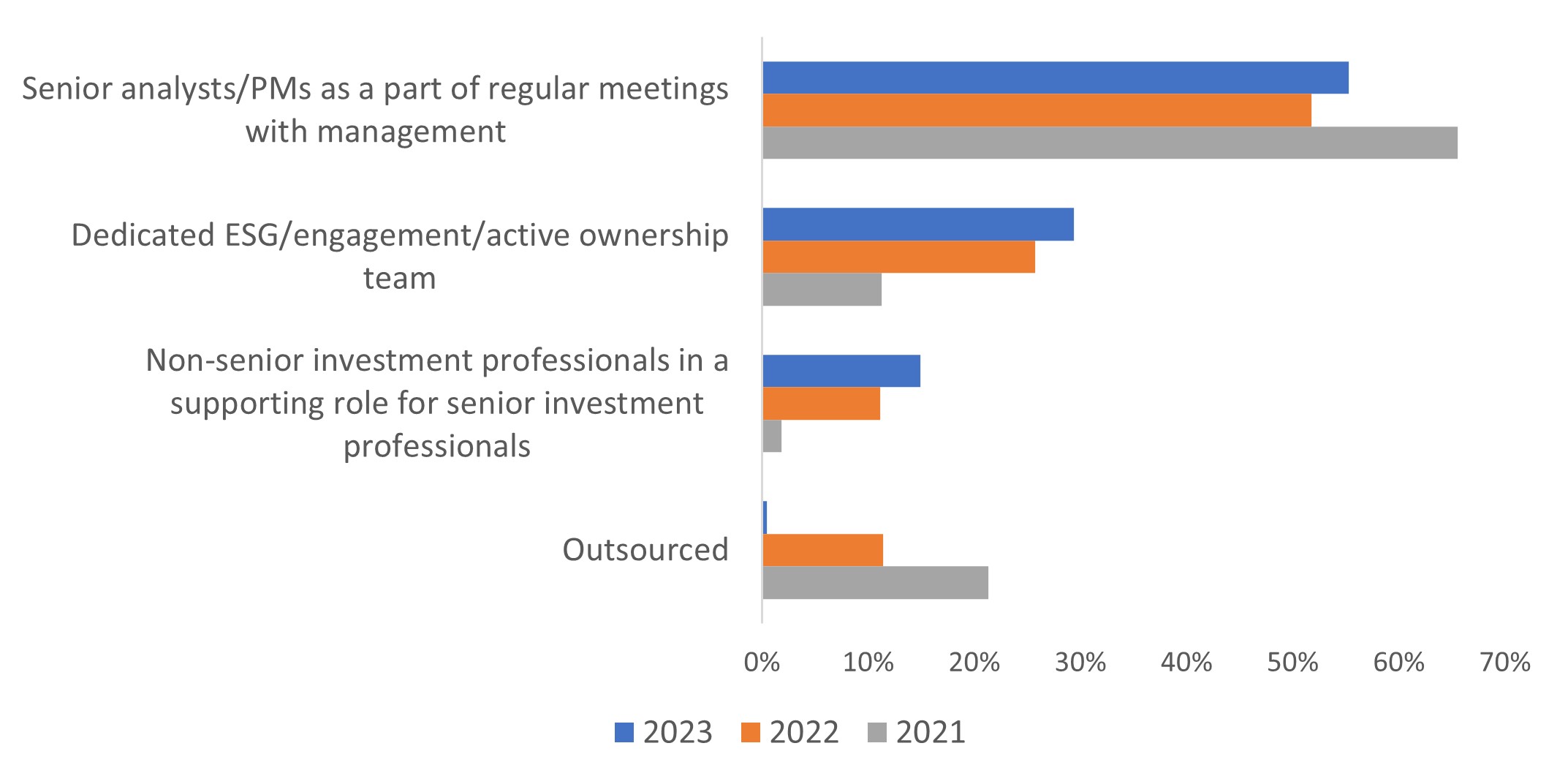

Engagement activity is kept in-house

Over half of the respondents include portfolio managers when conducting engagements activities, with another 15% relying on non-senior investment professionals who support senior professionals to take on engagement activity. Outsourcing of engagement activity has declined significantly, as headcount toward a dedicated ESG and/or stewardship team has risen.

(Click image to enlarge)

The vast majority of the investors who participated in the survey have partaken in collaborative engagement with other investors. However, this year’s respondents indicated lower Involvement with collaborative engagement programs, except for membership to Climate Action 100+, which was 4% higher at 31%. 39% of respondents were involved in the UN PRI (Principles for Responsible Investment) in 2023, 7% lower than the 2022 survey results. We find these data points interesting but not necessarily indicative of a trend. Additionally, 12% of firms engaged with IIGCC. 52% of respondents cited working with “Other” third party initiatives, among which Ceres and IGCC (Investor Group on Climate Change) were frequently specified.

In terms of engagement tracking processes, 70% indicated that they document and monitor ESG-related engagements. 65% also document unsuccessful engagements and next steps (escalation). The proportion of firms documenting unsuccessful engagements and divesting was largely unchanged year-over-year.

Voting

A mainstream tool in investment practice, and a shareholder right

In 2023, surveyed entities indicated higher adoption of bespoke (customised) policies, 77% versus 71% in 2022, while only 23% reported using standard policies from proxy advisors. We believe the trend toward custom voting policies remains intact, even as large firms and proxy advisors tout a greater variety of “off-the-shelf” or thematic voting templates for managers and their clients. Pass-through or client-directed voting solutions are becoming more accessible, yet our survey suggests their uptake continues to be limited.

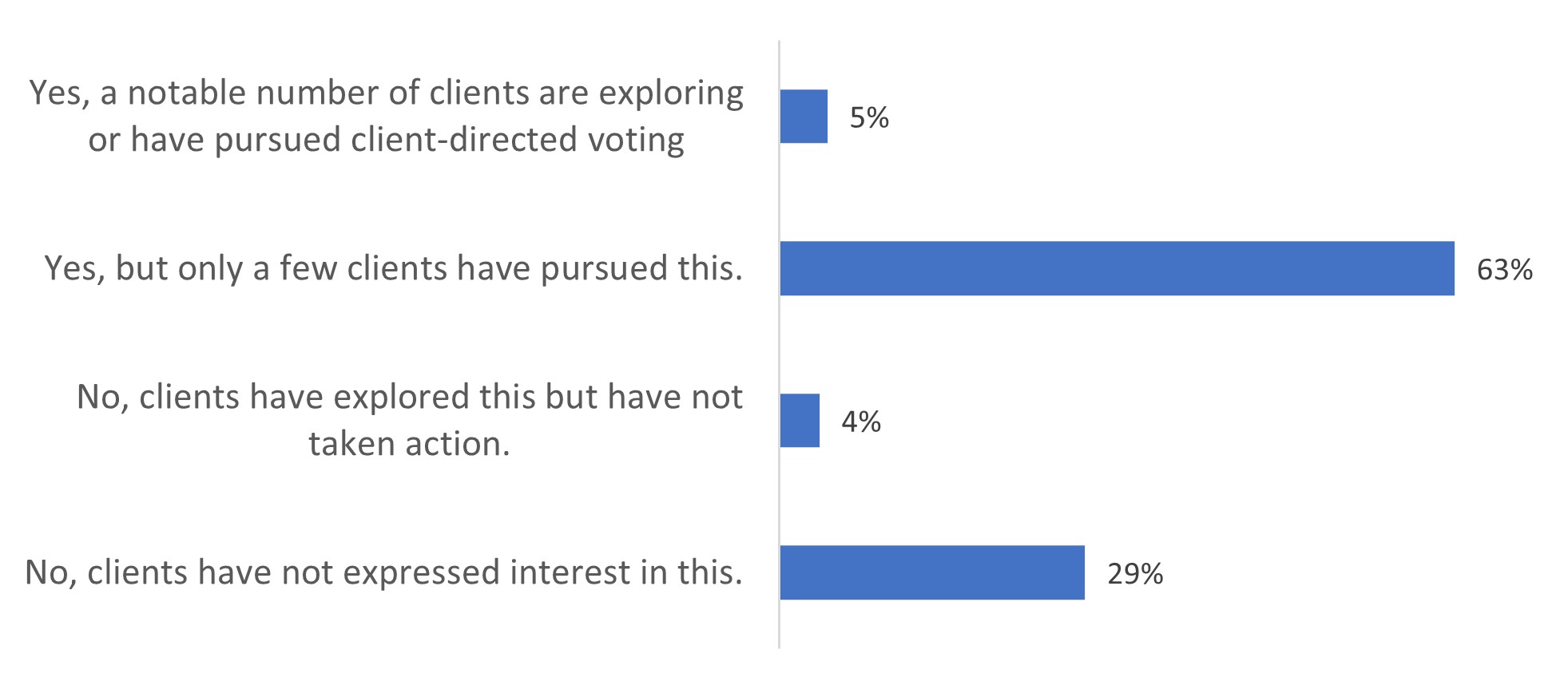

Client-directed voting gains attention, but not traction

For the first time, managers were asked to report whether clients are pursuing client-directed or pass-through voting, but despite media attention to the topic, this seems to still be a niche issue.

(Click image to enlarge)

The bottom line

Our survey and investment work tell us that investors are increasing their focus on ESG matters and are thinking about how to implement this into their engagement and proxy voting activities. Outsourcing of engagement activity has declined significantly, as headcount toward a dedicated ESG and/or stewardship team has risen. Meanwhile, the proportion of managers who are not engaging either on ESG or at all continues to dwindle, falling below 5% of respondents.

Increased adoption of bespoke voting policies is a heartening indication that managers are taking active ownership seriously as an investment tool. However, despite media focus on client-driven voting solutions like pass-through voting, this has not gone mainstream.

On the engagement front, there is still scope for improvement in terms of record keeping and engagement tracking practices. For firms actively engaging with most or all of their holdings, this granularity is particularly important to supporting their investment outcomes. In addition, without standardisation of the terms “engagement” and even “ESG”, it is difficult to make industry-wide conclusions.

However, in spite of these challenges, we believe that the trend of increased resourcing and attention to ESG and Active Ownership practices will persist. While there is still room for progress, indicators show that investor engagement is clearly moving in a positive direction.