Four potential outcomes for Brexit: Probabilities and market impact

Brexit update: Summary

Where are we now?

- On the 29th of January, the House of Commons rejected two cross-party amendments (Cooper-Boles and Grieve) that would have given it the legislative authority to effectively block a no-deal Brexit

- Additionally, the Commons accepted a Conservative amendment (Brady) that obliges the government to renegotiate a new deal without a backstop

- As the EU has already rejected the idea of a deal without a backstop, this sets the UK government on a collision course with their European interlocutors

- Taken together, the rejection of the Cooper-Boles and Grieve amendments, and the acceptance of the Brady amendment, materially increase our subjective likelihood of a no-deal Brexit from 20% to 30%

- As a result, the path to get to a positive Brexit outcome has materially narrowed in our view

Bottom line: With no-deal Brexit risks increasing and sterling having already experienced a strong year-to-date rally, we are now expecting to see sterling fall against the dollar and euro.

Brexit update: Deep dive

The political background

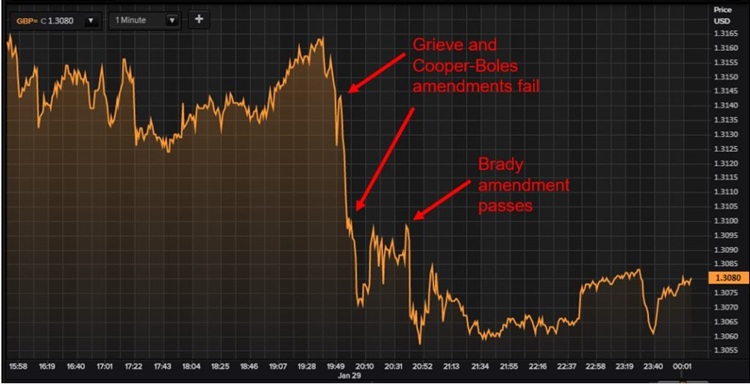

On the 29th of January, Parliament voted on seven amendments to the deal Prime Minister (PM) Theresa May has spent the last two years negotiating with the European Union (EU). Three of these, namely the Brady, Cooper-Boles and Grieve amendments, had the potential to be market-moving. The Grieve and Cooper-Boles amendments, which would have given Parliament the legislative tools to stop a no-deal Brexit and come up with an alternative, both failed to gain majorities.

In contrast, the Brady amendment won the backing of the House of Commons. This amendment forces the government to renegotiate the currently agreed deal in order to remove the Irish Backstop and replace it with unspecified alternative arrangements. Arguably, it sets PM May on a collision course with EU officials who have already rejected the idea of a deal without a backstop. Collectively, these votes explain Sterling’s 1% peak-to-trough fall with the U.S. dollar on the day, as can be seen in Figure 1.

Figure 1: GBP-USD intra-day moves on the 29th January

Source: Refinitiv (formerly Thomson Reuters) as at 29 January 2019.

Brexit scenarios: Implications for sterling, equities and gilts

We agree with the market view that the parliamentary outcomes from Tuesday 29th January are indeed negative results for the UK and UK-based assets. However, we are surprised that the downward move wasn’t bigger. In our view, the failure of Cooper-Boles and Grieve, and the success of the Brady amendment, materially increase the probability of a no-deal Brexit from 20% to 30%. Additionally, they also reduce the likelihood of the UK remaining in the EU or negotiating a closer relationship with the EU along the lines of a Norway+ agreement.

We do believe that the currently negotiated Brexit deal will eventually pass (this remains our central scenario, with a probability of 50% — up from 45% previously). However, the path to this scenario is looking ever more fraught with downside risks. The general asset class implications of these various scenarios are outlined below.1

Scenario one: ‘Remain’

Down from 15% to 10% probability

- Sterling: Significantly up (15-20%) as the UK’s (currently favourable) terms of trade with its biggest trading partner are secured for the future

- Large cap UK equities: Significantly down (10-15%) as the negative correlation with sterling weighs on the rest of the index

- Domestically-focused UK listed equities: Significantly up (15-20%) as the domestic UK economic outlook materially brightens

- 10-year gilts: Meaningfully down as yields rise (40-50 basis points) to accommodate a higher expected short-rate path and a higher neutral rate

Scenario two: ‘Single market and customs union’ Brexit

Down from 20% to 10% probability

- Sterling: Up (10-15%) as the UK’s links with its main trading partner aren’t materially damaged

- Large cap UK equities: Down (5-10%) as the negative correlation with sterling weighs on the rest of the index

- Domestically-focussed UK listed equities: Up (10-15%) as the domestic UK economic outlook brightens

- 10-year gilts: Down as yields rise (30-40 basis points) to accommodate a higher than expected short-rate path

Scenario three: ‘Current agreement’ Brexit

Up from 45% to 50% probability

- Sterling: Up (5-10%) on relief that a Brexit deal which includes a 2-year transition has been reached. However, the gains are tempered by the fact that another cliff-edge still exists down the road

- Large cap UK equities: Down (0-5%) as the negative correlation with sterling weighs on the rest of the index

- Domestically-focussed UK listed equities: Up (5-10%) as the UK’s economic outlook brightens somewhat

- 10-year gilts: Down as yields rise (20-30 basis points) as some negative risk premia is removed from the curve

Scenario four: ‘No-Deal’ Brexit

Up from 20% to 30% probability

- Sterling: Significantly down (15-20%) as UK is economically locked out of all of its main trading partners as it falls back to World Trade Organisation (WTO) terms

- Large cap UK equities: Up (10-15%) as sterling falling to new lows, materially enhancing international sterling-denominated profits

- Domestically-focused UK listed equities: Significantly down (15-20%) as the domestic UK economic outlook materially darkens

- 10-year gilts: Significantly up as yields fall (40-50 basis points) to new lows on safe haven demand and much reduced short-rate expectations

In Figure 2 below, we map these four Brexit scenarios discussed above to levels in GBP / EUR (sterling to euro) – the markets’ main proxy for Brexit risk sentiment. As we can see, whilst the potential upside is substantial if we do get a softer form of Brexit than the one implied by PM May’s deal, the recent run up in sterling against both the dollar and the euro, as well as our own shifting Brexit scenario probabilities, mean we see limited short-term upside for sterling. Indeed, we expect sterling to fall from here as the political process to get May’s deal through Parliament runs up against the clock, souring investor sentiment again.

Figure 2: Brexit risk premia

The bottom line

As with all market calls based on binary political outcomes, one must be particularly cautious about acting on them. However, given that the balance of risks have so materially shifted, we feel it may be appropriate to consider scaling back risk taking in sterling. On a longer-term horizon, however, given our base case still remains that some sort of deal will transpire, a short-term correction in sterling could provide long-term investors with an attractive entry point.

1 The asset moves have been calibrated using closing prices from the 21st January 2019. Direction and magnitude of expected market reaction is based on experience from the post-referendum (after 23 June 2016) period. The anticipated market reactions will not necessarily occur on the exit date (March 2019). They may occur suddenly in the run-up to the exit, if unexpected but clear political outcomes materialise. Alternatively, market moves may play out gradually over an extended period of time, if the political process evolves towards the outcome slowly.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.